WASHINGTON — Lindsey Johnson, President of U.S. Mortgage Insurers (USMI), today released the following statement on the organization’s comment letter submitted in response to the Consumer Financial Protection Bureau’s (“the Bureau”) Advance Notice of Proposed Rulemaking on the “Qualified Mortgage (QM) Definition under the Truth in Lending Act (Regulation Z).”

“As takers of first-loss mortgage credit risk with more than six decades of expertise and experience underwriting and actively managing that risk, USMI members understand the need to balance prudent underwriting with a clear and transparent standard that maintains access to affordable and sustainable mortgage finance credit for home-ready borrowers. The upcoming expiration of the temporary QM category, often referred to as the ‘GSE Patch,’ provides an important opportunity for the Bureau to assess what has developed within the marketplace since the enactment of the QM Rule. Notably, mortgage lending has been done with far greater diligence by market participants to ensure consumers have a reasonable ability-to-repay (ATR) and has resulted in a much stronger housing finance system. Further, the GSE Patch has played a critical role in maintaining credit availability. In our comments to the Bureau, we offer specific recommendations for replacing the current GSE Patch to establish a single transparent and consistent QM definition in a way to balance access to mortgage finance credit and proper underwriting guardrails to ensure consumers’ ATR. USMI’s recommendations include:

Maintaining the ATR and product restrictions as part of any updates to the QM definition to ensure discipline in the lending community and to protect consumers;

Retaining specific underwriting guardrails such as the current debt-to-income (DTI) component of the QM definition, but modifying the specific threshold to better serve consumers; and

Developing a single set of transparent compensating factors for loans with DTIs above 45 and up to 50 percent for defining QM across all markets, similar to how the GSEs, FHA, and VA use compensating factors in their respective markets today.

“Retaining specific thresholds in measuring a consumer’s income, assets, and financial obligations better serves consumers and ensures that the statutory and regulatory intent of measuring a consumer’s ATR is met. Further, adjusting the current DTI limit from 43 percent to 45 percent for all loans, and up to 50 percent for loans with accompanying compensating factors creates a more transparent and level playing field that provides greater certainty for borrowers and lenders and reduces the impact of the expiration of the GSE Patch. USMI believes that the development of a single transparent industry standard will facilitate greater consistency across all lending channels and ensure there is not market arbitrage to achieve QM status.

“USMI applauds the Bureau for undertaking the necessary process for updating this critical rule that is aimed at enhancing lending standards and consumer protection. We look forward to working with the Bureau as it seeks to implement any changes to this important rule.”

Following the release of the Bureau’s ANPR in July, USMI published a blog with observations and recommendations for replacing the GSE Patch.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

Luisa De Gaetano Polverosi Associate Managing Director Moody’s Investor Service 7 World Trade Center 250 Greenwich Street New York, NY 10007

Dear Ms. De Gaetano Polverosi:

U.S. Mortgage Insurers (USMI) welcomes the opportunity to provide comments on the “Proposed Update to Moody’s Approach to Rating US Prime RMBS”. Our members are supportive of the proposed update to Moody’s methodology, and view this update as a necessary step toward examining and updating various models, and also as a step toward prudently revitalizing the private securitization market for Residential Mortgage-Backed Securities (RMBS). We applaud the recognition that the value of private mortgage insurance (MI) extends beyond the government-sponsored enterprise (GSE) segment of the housing finance system and we believe that RMBS investors can greatly benefit from the loss severity reduction resulting from MI.

Of particular interest to our members is the proposed update to the evaluation of private MI. Lenders originating mortgages with loan-to-value (LTV) ratios above 80% typically obtain MI to maintain maximum flexibility for secondary market execution. Currently, however, the lack of credit for MI in the rating determination provides little incentive for these mortgages to be included in RMBS structures and transactions. The proposed changes to the methodology address this issue and lenders will no longer be disincentivized to direct mortgages with LTVs above 80% to the RMBS market, thus increasing access to liquidity in support of homeownership and offering investors more choices with regard to taking credit risk in this vital segment of the mortgage market.

Our members appreciate that the proposed update to Moody’s methodology has been the result of an investment of considerable time and effort in data analysis, as well as careful attention to the development of the mortgage lending landscape. While the proposal as published is an improvement, in the spirit of mutually beneficial ongoing dialogue, we would like to offer some commentary on the proposed methodology. Generally speaking, we feel that additional transparency, particularly more details around the benefits of MI, the proposed changes to rejection rates, and Moody’s methodology of determining maximum insurance payout and allocation based on the insurer’s rating, would be highly beneficial to market participants and enable more detailed analysis of the proposal, in addition to some minor recommended adjustments.

Rejection Rate Assumptions

Looking at the proposed rejection rates, a more detailed representation of the slope and/or shape of the line between the Baseline Assumption and Aaa Assumption would be useful, as well as more details surrounding the Aaa Assumption’s rejection rate range of 5-15% in the absence of a GSE backstop. In additional, the variability of the Aaa Assumption should include disclosures of all the factors that can drive a final determination.

We would also encourage the rejection rate assumptions to reflect MIs’ updated Master Policies which increased clarity on terms and streamlined the payment of claims to ensure that MI coverage results in timely, consistent, and accurate policy and claim administration. The proposed update’s rejection rate assumptions should account for the imbedded Rescission Relief (contractual circumstances under which an MI waives it rights to rescind coverage on a mortgage) applicable to the loans in a specific transaction. Mortgages that are already subject to Rescission Relief should have lower assumed rejection rates, and the various milestones regarding Rescission Relief should also be considered in the overall lifetime projections. Our member companies are more than willing to provide detailed information on Rescission Relief to Moody’s to assist with the refinement of implementation of the rejection rate assumptions.

Further, the proposed update to the rating methodology should reflect overall improvements in mortgage originators’ underwriting standards, as well as the MI industry’s new capital framework that is driven by the GSEs’ Private Mortgage Insurer Eligibility Requirements (PMIERs). All MI companies comply with PMIERs’ stringent capital and operational requirements and the industry has nearly doubled its pre-crisis capital, an indication of the industry’s strength and that MI on loans included in securitizations should improve credit enhancement levels in rated RMBS transactions.

The rejection rate haircut should also reflect the Representations & Warranties of a particular transaction and encourage stronger language by providing a benefit to RMBS issuers that provide investors with an extra layer of protection. There have been significant improvements to lenders’ underwriting practices, including the use of independent validation sources, over the last several years that would serve to reduce the overall rejection rates and improve credit enhancement levels, and should therefore be considered for loans that will be repurchased due to loan manufacturing defects or where the trust will be made whole due to servicing defects. Lastly, with regards to the differential treatment of the GSE backstop, USMI encourages Moody’s to consider broadening that category to create a level playing field by including additional types of credit enhancement backstops from a variety of counterparties that would supplement private MI’s credit risk protection.

Maximum Insurance Payout and Allocation

The proposed update includes analysis of expected losses but currently lacks visibility into the benefit of MI as it relates to the Moody’s Individual Loan Analysis credit enhancement (MILAN CE) framework. We would like to request that Moody’s disclose detailed methodology regarding treatment of MI in the MILAN framework. In practice, it is critical that a RMBS issuer be able to quantify the benefit of MI with a certain insurer rating in each of the rating scenarios. Therefore, we believe the RMBS market will greatly benefit from Moody’s publishing the Idealized Expected Loss Table which demonstrates the conversion from non-rejected insured losses to idealized losses in correspondence to the insurance rating of MI in each loss scenario. Without seeing the Idealized Expected Loss Table, it is difficult to comment on this specific component of the proposed methodology update, but there are a couple of general comments related to this element of the rating methodology we would like to offer.

The first is that since the rating of private MIs depends on many factors beyond their capital adequacy, it is possible that purely using an overall company rating may be overly conservative. For examples, ratings of private MIs may not fully reflect the benefit of credit risk transfer programs the MI industry executes with global capital markets and reinsurers, which have transformed the MI business model from “buy-and-hold” to “buy-manage-distribute” and significantly strengthen MIs’ capital positions and claims paying ability during stress periods. While the insurer rating may be reflective as an overall measure of counterparty risk, the incorporation of non-claims payment factors means that items not related to the ability to pay all claims are taken into consideration. It would be very helpful to have access to MI rating sensitivity analysis, as well as loss scenarios that inform the proposed methodology updates.

The second comment is that we would like to understand how the maximum insurance payout (MIP) plateaus and how the state-based insurance regulatory framework has been reflected. Of the private MI companies that ceased writing new business during the financial crisis approximately a decade ago, their cash payouts currently range from approximately 75% to 100%, with the remainder being deferred payment obligations (DPO) – facts that support very high MIP assumptions.

Conclusion

Thank you again for the opportunity to comment on the “Proposed Update to Moody’s Approach to Rating US Prime RMBS.” Our members appreciate the data-driven analysis and proposed update, and look forward to continuing a mutually beneficial dialogue, including on the topic of recognition of the value of private MI. This important shift can help promote new interest in private label RMBS, as lenders will have increased secondary market execution flexibility when it comes to their insured mortgage production. By providing an avenue for mortgages with private MI to contribute to the supply of collateral for RMBS, we will see improved liquidity for lenders and an expansion of mortgage credit investment opportunities for private capital investors.

Questions or requests for additional information may be directed to Lindsey Johnson, President of USMI, at ljohnson@usmi.org or 202-280-1820.

Sincerely,

Lindsey D. Johnson President U.S. Mortgage Insurers

Alfred M. Pollard General Counsel Federal Housing Finance Agency Eighth Floor 400 Seventh Street, SW Washington, D.C. 20219

RE: Comments/RIN 2590-AA95

Dear Mr. Pollard:

This letter is submitted by U.S. Mortgage Insurers (USMI), a trade association comprised of the leading private mortgage insurance (MI) companies in the United States.0F1 Together, the private mortgage insurance industry has helped nearly 30 million homeowners over the past 60 years, including more than 1 million in the past year alone.

USMI is dedicated to a housing finance system backed by private capital that enables access to housing finance for all creditworthy borrowers while protecting taxpayers. USMI supports meaningful and appropriate capital requirements for Fannie Mae and Freddie Mac (the “Enterprises”) and appreciates the Federal Housing Finance Agency (FHFA) for initiating this rulemaking process, and for affording us an opportunity to submit comments.

Currently, the Enterprises use a FHFA-developed Conservatorship Capital Framework (CCF) to align business and pricing decisions (e.g. G-Fees) with economic risk. The notice of proposed rulemaking (NPR) states that during conservatorship, FHFA expects the Enterprises to “use assumptions about capital described in the rule’s risk-based capital requirements in making pricing and other business decisions,” even though the new standards will not be used to determine capital compliance until after the conservatorship ends.1F2 Therefore, the final regulation could have an immediate real-world impact on the Enterprises’ activities and the cost and availability of mortgage credit. As a result, this rulemaking is very significant for our members, other participants in housing finance, and the American public.

USMI joined nearly 60 other organizations in supporting a full Senate vote on the nomination of Pam Patenaude as HUD Deputy Secretary. Click below to read the full coalition letter. Click here to download the letter as a PDF.

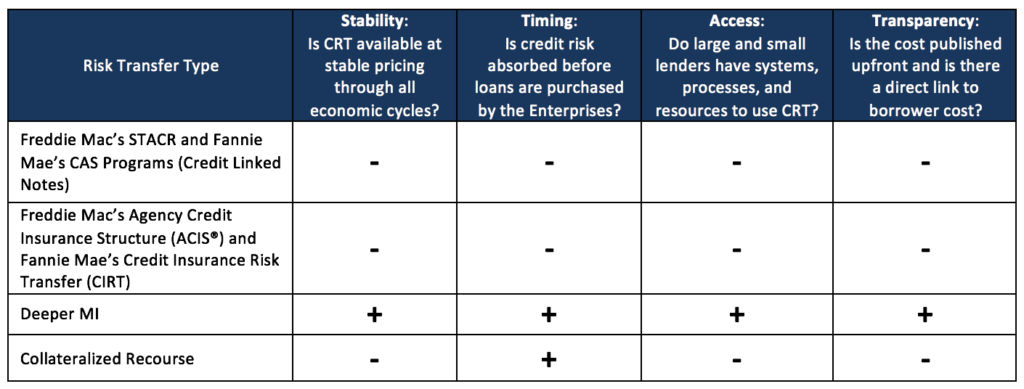

USMI Submits Comments on FHFA’s Single-Family Credit Risk Transfer Request for Input Mortgage insurers outline industry’s role in shifting greater risk away from taxpayers in an equitable way for all lenders while expanding access to homeownership

WASHINGTON — U.S. Mortgage Insurers (USMI) submitted comments to the Federal Housing Finance Agency (FHFA) today regarding its Single-Family Credit Risk Transfer (CRT) Request for Input (RFI) and steps to further shield the government sponsored enterprises (GSEs), Fannie Mae and Freddie Mac, as well as American taxpayers, from losses from mortgage-related risks. In its comments, USMI highlights the distinct advantages of front-end CRT done through expanded use of mortgage insurance (MI) that can address existing shortcomings in the GSEs’ credit risk transfer transactions and that can offer substantial benefits for taxpayers, lenders of all sizes, and borrowers.

USMI notes in its comments that “increasing the proportion of front-end CRT in the Enterprises’ CRT strategy will advance four key objectives of a well-functioning housing finance system by ensuring that: (1) a substantial of private capital loss protection is available in bad times as well as good; (2) such private capital absorbs and deepens protection against first losses before the government and taxpayer; (3) all sizes and types of financial institutions have equitable access to CRT; and (4) CRT costs are transparent, thereby enhancing borrower access to affordable mortgage credit.”

“By design, and as evidenced by the more than $50 billion in claims our industry paid during and since the financial crisis, mortgage insurance provides significant first-loss risk protection for the government and taxpayers against losses on low-down payment loans,” said Lindsey Johnson, President and Executive Director of USMI. “As the government explores ways to further reduce mortgage-related risk while also ensuring that Americans continue to have access to affordable home financing, experience shows that mortgage insurance is the answer, particularly when you consider mortgage insurance protection is at work before the risk even reaches the GSEs’ balance sheets.”

While USMI commends FHFA in its comment letter for establishing principles and risks to evaluate front-end CRT structures, which will enable the GSEs and other market participants to analyze the virtues and shortcomings of each form of CRT using an analytical framework, it urges that “the RFI principles should apply to both existing and proposed CRT activities.”

Among other questions, the RFI inquired about benefits of front-end CRT for small lenders. USMI explains in its letter that “small lenders derive optimal benefits from CRT programs that are familiar, have minimal implementation costs, and are based on lender selection among several market participants. Accordingly, MI works very well for small lenders (and deeper-cover MI similarly would work very well for small lenders) because it is already part of their current credit origination processes, is available with transparent pricing, and is available to lenders of all sizes. On the other hand, small lenders have no access to and derive no direct benefits from back-end forms of CRT.”

“In addition to the specific goal of shifting more risk from Fannie Mae and Freddie Mac, and unlike back-end CRT, mortgage insurance plays a direct role in helping families who have good credit but can’t afford large down payments to qualify for a mortgage. For nearly sixty years, mortgage insurers have been leaders in helping millions of Americans, particularly first-time homebuyers, purchase homes in an affordable way,” Johnson said.

Johnson added, “MI is one of the best forms of time-tested credit risk protection for our nation’s mortgage finance system. Mortgage insurers have taken steps to enhance both their claims paying ability—by increased capital and operational standards—and their claims paying process through updated Master Policy Agreements. MI is private capital directly tied to housing. Unlike some other forms of CRT structures, MI is dedicated to a housing finance system in good and bad economic times. By using more MI to provide deeper front-end risk sharing on loans the GSEs guaranty, the GSEs and taxpayers will be at a much more remote risk of losses. Promoting greater front-end risk sharing with MI is a way to help build a strong, stable housing finance system, provide prudent access to affordable mortgage credit, protect taxpayers, and help facilitate the homeownership aspirations for Americans for years to come. ”

USMI’s full comments to FHFA can be found here. A fact sheet on USMI’s comments can be found here.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

USMI delivered the following letter to members of the Senate Banking Committee last night:

May 20, 2015

The Honorable Richard Shelby

Chairman

U.S. Senate Committee on Banking, Housing, and Urban Affairs

534 Dirksen Senate Office Building

Washington, DC 20510

Dear Chairman Shelby:

U.S. Mortgage Insurers (“USMI”) welcomes the effort to make progress on increasing the reliance on private capital in housing finance as part of consideration by the Senate Banking Committee of the Financial Regulatory Improvement Act of 2015.

Specifically, USMI supports Section 706, which calls on the Government Sponsored Enterprises (“GSEs”) to engage in front-end risk sharing transactions. This directive would make greater use of private capital to “de-risk” the GSEs, lower the exposure and costs for the enterprises and taxpayers and should lower costs to borrowers. USMI supports this effort, and will continue to work with the Committee during the legislative process on clarifications to ensure the legislation has the intended effect of being “transaction neutral” to permit a variety of methods of up front risk sharing, with all risk sharing counterparties held to equivalent standards.

Promotion of greater up front risk sharing will help build a strong, stable housing finance system that provides access to sustainable and affordable mortgage credit while protecting taxpayers. We look forward to favorable action on this important effort.

USMI Supports Affordable Housing Principles and Calls for Transparency in FHFA Duty to Serve Plans

USMI submitted comments on the Federal Housing Finance Agency’s (FHFA’s) proposal for how the government sponsored housing enterprises Fannie Mae and Freddie Mac should serve underserved markets. USMI supports both principles of facilitating the financing of affordable housing for low-to-moderate income families consistent with the Enterprises’ overall public purposes while maintaining a strong financial condition and reasonable economic return. To that end, among other things USMI calls for full transparency into the economics of the Plans to ensure policy aims are met in the most efficient way available. USMI looks forward to working with MI customers, FHFA, the Enterprises, and other market stakeholders to help the Enterprises meet their “Duty to Serve” obligations. The text of the USMI comment letter can be found here.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

In letters to House and Senate Budget Committee leadership, USMI joined a broad group of more than a dozen housing organizations urging Congress to use GSE G-fees for their intended purpose, to support homeownership stability.

“By preventing g-fees to be used as a funding offset, this budget point of order gives lawmakers a vital tool to prevent homeowners from footing the bill for unrelated spending,” the letters said. “We urge you to once again include it in this year’s Budget Resolution.”

Click here for the full text of the House and Senate letters.

USMI Statement on Moore – Stivers Letter to FHFA Director Watt

“Yesterday’s bipartisan letter from Representatives Gwen Moore (D-WI) and Steve Stivers (R-OH) to Federal Housing Finance Agency (FHFA) Director Watt is further evidence of the growing bipartisan support for de-risking the Government Sponsored Enterprises (GSEs) with additional risk sharing transactions to reduce taxpayer exposure to losses from another housing downturn. USMI commends Representatives Moore and Stivers for urging FHFA to take additional steps to incorporate front end risk sharing, including with MI.

The letter expresses concern ‘about the lack of balance between ‘front-end’ and ‘back-end’ risk sharing. With FHFA having affirmed the importance of using private capital whenever practicable and equitable in credit-risk sharing transactions, we wanted to urge additional exploration and refinement of credit-risk sharing techniques that are consistent with other federal housing goals.’

Front-end risk share transactions transfer the risk of loans before they ever reach the GSE’s balance sheets. The letter by Reps. Moore and Stivers joins a bipartisan letter in the U.S. Senate by Sens. Mark Warner (D-VA), Bob Corker (R-TN), Heidi Heitkamp (D-ND), Mike Crapo (R-ID), Jon Tester (D-MT) and Dean Heller (R-NV) which also encourages FHFA to expand and better define the development of credit risk transfer programs.”

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

USMI Statement on Luetkemeyer – McHenry Letter to FHFA Director Watt

Statement by Lindsey Johnson, President and Executive Director of USMI

“Today, Representatives Blaine Luetkemeyer and Patrick McHenry sent a letter to Federal Housing Finance Agency Director Watt ‘regarding the transactions that Fannie Mae and Freddie Mac (the Enterprises) enter in order to share mortgage credit risk with private market participants.’ According to the letter, ‘[w]hile we strongly support these transactions as a mechanism for mitigating credit risk to the Enterprises and U.S. taxpayers, we are concerned that the focus for these transactions has been too heavily concentrated on back-end credit risk sharing. Accordingly, in order to expand the scope of risk sharing and to avoid favoring one approach to risk sharing over another, we believe that the Federal Housing Finance Agency (FHFA) should require the Enterprises to also explore and engage in diverse forms of front-end credit risk sharing.’

USMI members applaud Representatives Luetkemeyer and McHenry, Chair of the House Financial Services Committee’s Housing and Insurance Subcommittee and House Financial Services Committee Vice Chairman, respectively, for their leadership and advocacy on this important issue.

In advance of the upcoming release of FHFA’s 2016 Scorecard, taxpayers still face significant exposure to losses from another housing downturn. Front-end risk share transactions transfer the risk of loans before they ever reach the GSE’s balance sheets. As outlined in the letter, the benefits of front end risk sharing are clear. USMI agrees that there should be a greater balance between front and back end credit risk transfers. Of the several ways that the GSEs can conduct front-end risk share transactions, using MI on the front end is one of the easiest, most readily available forms that would be accessible to a vast majority of lenders today.

Momentum is growing to expand front end risk sharing with MI, and USMI members are ready to do more to de-risk the housing finance system while enhancing homeowners’ ability to borrow in an affordable way.”

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

(November 10, 2015) In a letter to conferees on the pending highway bill, USMI joined a broad coalition of 27 housing organizations in urging conferees to draw funds from the Federal Reserve’s surplus, rather than using GSE G-fees, to pay for the extension of the Highway Trust Fund.

(September 17, 2015) This week, in a joint letter to the bipartisan Congressional leadership, USMI and a diverse coalition of thirty-two housing organizations reiterated their opposition to using the mortgage credit risk guarantee fees (g-fees) charged by the housing finance enterprises, Fannie Mae and Freddie Mac, as a source to finance extension of federal highway programs. The letter states: “increasing g-fees for other purposes… imposes an unjustified burden on the housing finance system.” “Adding an additional fee to mortgages for unrelated expenses would only increase the hurdles these families already face in achieving the American dream of homeownership”, it continues.