On July 24, USMI submitted a comment letter in response to the U.S. Federal Housing (FHFA) Notice of Proposed Rulemaking (NPR) on “Enterprise Duty to Serve Underserved Markets.” USMI supports FHFA’s consideration of advances in manufactured housing and the opportunity to better serve homebuyers who purchase it. Additionally, USMI recommends that FHFA incorporate private MI and primary first-loss credit enhancement into the safety and soundness evaluation for any new product or activity to ensure that homebuyers are affordably and sustainably served, while private capital absorbs credit losses. Click here to read the full letter.

Category: Uncategorized

Homeownership: The Heart of the American Dream

USMI Statement on Introduction of the Sustainable Homeownership Act (H.R. 9460)

WASHINGTON — Seth Appleton, President of U.S. Mortgage Insurers (USMI), today released the following statement regarding the introduction of H.R. 9460, the “Sustainable Homeownership Act,” by Rep. Scott Fitzgerald (WI-05):

“We applaud Rep. Fitzgerald’s thoughtful approach and are pleased to support H.R. 9460, which includes important policies to advance access to affordable home financing for creditworthy borrowers nationwide, while promoting safety and soundness in the housing finance system.

“Among its key provisions, H.R. 9460 would ensure that private capital continues to meaningfully reduce the loss severity of low down payment loans that default, absorbing risk ahead of lenders, the government-sponsored enterprises, and taxpayers; foster transparency around new products, activities, and pilots; and prohibit piggyback mortgages, which allow borrowers to take out multiple loans for the same home purchase and performed poorly during the Great Financial Crisis.

“For nearly 70 years, the private MI industry has served first-time and working-class homebuyers throughout the country who don’t have the resources for 20% down payments and USMI’s members help hardworking Americans buy homes sooner throughout all housing market cycles. We commend Rep. Fitzgerald for his efforts to make homeownership more attainable and sustainable, while ensuring that private capital – not the taxpayer – continues to bear a greater share of mortgage credit risk.”

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

USMI Submits Comment Letter to Banking Regulators on Proposed Bank Capital Rules

Recognizing private mortgage insurance in bank capital regulations could increase access to mortgage credit and make homeownership more affordable for first-time and working-class borrowers

WASHINGTON — U.S. Mortgage Insurers (USMI), the association representing the nation’s leading private mortgage insurance (MI) companies, recently submitted a comment letter to the Federal Reserve System (Federal Reserve), the Federal Deposit Insurance Corporation (FDIC), and the Office of the Comptroller of the Currency (OCC) (collectively the Agencies) in response to two Notices of Proposed Rulemaking (NPRs) on Regulatory Capital Rules that would modernize bank capital requirements for assets held on balance sheet, including residential mortgages.

“USMI strongly supports the Agencies’ efforts to create a more risk-sensitive framework that reflects the true credit risk of residential mortgages, and recognition of private mortgage insurance in mortgage exposure risk weights supports that goal,” said Seth Appleton, President of USMI. “Aligning capital treatment to acknowledge the role that private MI plays in mitigating risk in the housing finance system would allow banks to more efficiently serve first-time homebuyers and working families pursuing the American Dream.”

In its comment letter, USMI urged the Agencies to make the following targeted changes in the final rule:

- Recognize private MI coverage in the calculation of a mortgage’s loan-to-value (LTV) ratio for the purposes of assigning risk weights, with capital relief calibrated to the depth of MI coverage. Third-party actuarial analysis from Milliman of more than 90 million loans over a 25-year period found that private MI reduces net loss severity on insured high-LTV loans to below the gross loss severity observed on loans with LTVs between 60% and 80%. Crisis-vintage loans (2005-2009) with LTVs above 90% and private MI coverage had net loss severity of just 29%, compared to 52% gross loss severity for the 60-80% LTV benchmark.

- Apply a counterparty haircut to private MI coverage that does not exceed 14.2%. This is aligned with the Federal Housing Finance Agency’s (FHFA) Enterprise Regulatory Capital Framework (ERCF) – the most comprehensive U.S. capital framework for mortgage credit risk, supporting consistency across federal regulatory frameworks.

- Clarify the “Eligible Guarantor” definition to permit highly rated, well-capitalized private MI companies to participate in bank credit risk transfer (CRT) transactions, bringing additional private capital into the U.S. banking system and reducing reliance on government-backed alternatives.

“The private MI industry exists precisely to absorb losses on high-LTV loans so that lenders, the government-sponsored enterprises (GSEs), and taxpayers are protected from risk,” added Appleton. “The Agencies’ final rule should reflect the same safety and soundness benefits of private MI that the Agencies have already recognized in prudent underwriting standards when calculating and assigning capital requirements for residential mortgage exposures.”

In February, USMI joined a coalition of housing in banking industry stakeholders in sending a letter to banking regulators in support of efforts to modernize bank capital standards to strengthen financial stability and housing affordability. The groups wrote that a revised Basel III Endgame rule should support the critical role that private mortgage insurance (MI) plays in reducing risk for taxpayers while preserving and enhancing mortgage finance options for homebuyers. This includes providing loan-level capital relief commensurate with the level of private MI coverage and adjusting the Eligible Guarantor definition to include private mortgage insurers.

For nearly 70 years, the private MI industry has served lenders, the GSEs, the U.S. government, and taxpayers as an effective and resilient form of private capital, standing as the first layer of protection against credit risk and mortgage defaults, while enabling access to mortgage credit for borrowers without large down payments. In 2025 alone, more than 800,000 borrowers purchased a home or refinanced a loan with private MI, accounting for more than $311 billion in originations. Collectively, private MI saved American homebuyers more than $35.3 billion in down payment costs in 2025 by using private MI rather than waiting to accumulate a 20% down payment.

To read USMI’s full comment letter, click here.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

USMI Names MGIC CEO Tim Mattke as Chair of the Board

WASHINGTON, DC — U.S. Mortgage Insurers (USMI), the association representing the nation’s leading private mortgage insurance (MI) companies, today announced that Tim Mattke will serve as the association’s new Chairman of the Board of Directors. Mr. Mattke is CEO of MGIC and its parent company, MGIC Investment Corporation (NYSE: MTG). He succeeds Rohit Gupta, President, CEO, and Director of Enact Holdings, Inc. (Nasdaq: ACT), as Chairman of the Board of Directors.

“Private MI plays a critical role in the housing finance system, serving low down payment borrowers and allowing them to begin accumulating generational wealth associated with homeownership years sooner, while at the same time protecting lenders, investors, and taxpayers from undue mortgage credit risk,” said Tim Mattke, incoming Chairman of the USMI Board of Directors. “It is an honor to be elected as Chairman of USMI as we celebrate 70 years of private MI supporting homeownership for more than 41 million households.”

Prior to his current role, Mr. Mattke held positions in accounting and finance at MGIC and in audit with PricewaterhouseCoopers LLP.

“Tim’s extensive career in mortgage finance, along with his years of work with USMI to expand access to homeownership for first-time buyers and working families, positions him well to serve as Chairman,” said outgoing USMI Chairman Rohit Gupta. “I’ve had the opportunity to work alongside Tim through our shared work with USMI, and I’m confident his leadership will build on the strong progress we’ve made. In the last few years alone, private MI has helped homebuyers save more than $250 billion in cash at closing, and I look forward to continuing that momentum with Tim and the broader USMI community to support affordable, sustainable homeownership.”

USMI President Seth Appleton added, “In contrast to other costs associated with homeownership, private MI premium rates have declined 25% since 2017 and private MI premiums are once again tax deductible for working-class homeowners. On behalf of USMI, we thank Rohit for his exemplary service as Chair over the past two years. Tim’s leadership at MGIC has demonstrated his commitment to helping first-time homebuyers achieve the American Dream and I am confident that the association is well-positioned to be an effective voice for all those who count on private MI to buy a home without a large cash down payment.”

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

Private Mortgage Insurers Helped More than 800,000 Borrowers in 2025

WASHINGTON — U.S. Mortgage Insurers (USMI), the association representing the nation’s leading private mortgage insurance (MI) companies, released annual volume data showing that the private MI industry helped more than 800,000 borrowers secure mortgage financing in 2025. Approximately 92% of these mortgages were new purchases.

“Homeownership has long been a bedrock of the American Dream and, for generations, private MI has served as a tool for millions of American families to affordably and sustainably achieve this milestone,” said Seth Appleton, President of USMI. “This latest data further demonstrates the foundational role private MI plays in making homeownership attainable for first-time homebuyers and working families across the country.”

Over the past nearly 70 years, the private MI industry has enabled nearly 41 million people to access affordable and sustainable low down payment mortgages. In 2025, nearly 65% of those who used private MI to purchase a home without a large cash down payment were first-time homebuyers. The average loan amount for mortgages backed by private MI was roughly $375,000, according to data from Fannie Mae and Freddie Mac (the GSEs).

A USMI report found that, on average, it could take 26 years for a household earning the national median income to save a 20% down payment plus closing costs at the median national sales price. Rather than waiting a quarter century to achieve homeownership, private MI allows homebuyers to get off the sidelines with as little as a 3% down payment and begin building generational wealth and equity years, or even decades, sooner. By using private MI and accessing homeownership with smaller down payments, American homebuyers collectively saved more than $250 billion in down payment costs since 2020, including more than $35.3 billion in 2025 alone.

Importantly, private MI premium rates, as measured by publicly available in-force portfolio yield data, have declined in recent years due to the 2017 Trump tax cuts and enhanced risk-based pricing, in stark contrast to other costs associated with homeownership such as homeowners insurance premium rates and household utility rates. And, thanks to the Working Families Tax Cuts signed into law by President Trump last summer, qualified homeowners will once again be able to deduct premiums paid to private MI companies and government agencies on their federal income taxes and receive targeted tax relief.

“The deduction was claimed more than 44 million times between 2007 and 2021, when qualified American families were able to deduct MI premiums from their federal taxes. For 2021, the average deduction was more than $2,300,” said Appleton. “Beginning next tax season, millions of hard-working American homeowners will once again receive meaningful relief as federal tax policy promotes sustainable homeownership across the country.”

By design, private MI serves as the first layer of private capital protecting the housing finance system against default risk, protecting more than $1.6 trillion in mortgages and shielding the GSEs, lenders, and taxpayers from mortgage credit risk. The private MI industry’s strength and resiliency has been reinforced by safeguards and enhancements, including updated Private Mortgage Insurer Eligibility Requirements (PMIERs), which set robust, granular requirements for insuring loans acquired by the GSEs.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to affordable and sustainable housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

Private Mortgage Insurance: The Tool Helping Millions of Americans Buy Homes Sooner

As Financial Literacy Month concludes, it is the perfect time to shine a light on some of the unsung tools that can help homebuyers save money in the current economic environment. A 2024 survey by U.S. Mortgage Insurers found that only one-third of Americans are aware that it is possible to qualify for financing with only three percent down. By using private mortgage insurance (MI), Americans can own a home years or even decades sooner than they could with a 20% down payment.

And now, new data shows that private MI helped American homebuyers collectively save more than $258 billion dollars in cash due at the closing table between 2020 and 2024 alone. With America’s 250th birthday around the corner, that means more than $250 billion in down payment funds were saved by American homebuyers, putting a cornerstone of the American Dream within reach for hundreds of thousands of households per year.

According to a USMI report, on average, it could take 26 years for a household earning the national median income in 2024 to save for 20% down plus closing costs at the median national sales price. That is a quarter century of renting, saving, and not recognizing the generational wealth building potential of homeownership. However, that same household could become homeowners 65% faster by only putting down 5% with the help of private MI, making homeownership attainable for first-time homebuyers much sooner.

For nearly 70 years, the private MI industry has helped Americans to realize affordable homeownership without large down payments, allowing them to come to the closing table with tens of thousands of dollars less in cash and access homeownership years earlier than previously possible. Thanks to the Working Families Tax Cuts Act signed by President Trump last summer, private MI is also once again tax deductible for qualifying homeowners for the first time since tax year 2021. During the period in which private MI was tax deductible, from 2007 to 2021, qualifying American homeowners benefited from an average deduction of $1,454 a year or $64.7 billion total over the 15 years it was available. Starting with tax year 2026 – the taxes borrowers will file in spring 2027 – qualifying homeowners once again can take advantage of this benefit.

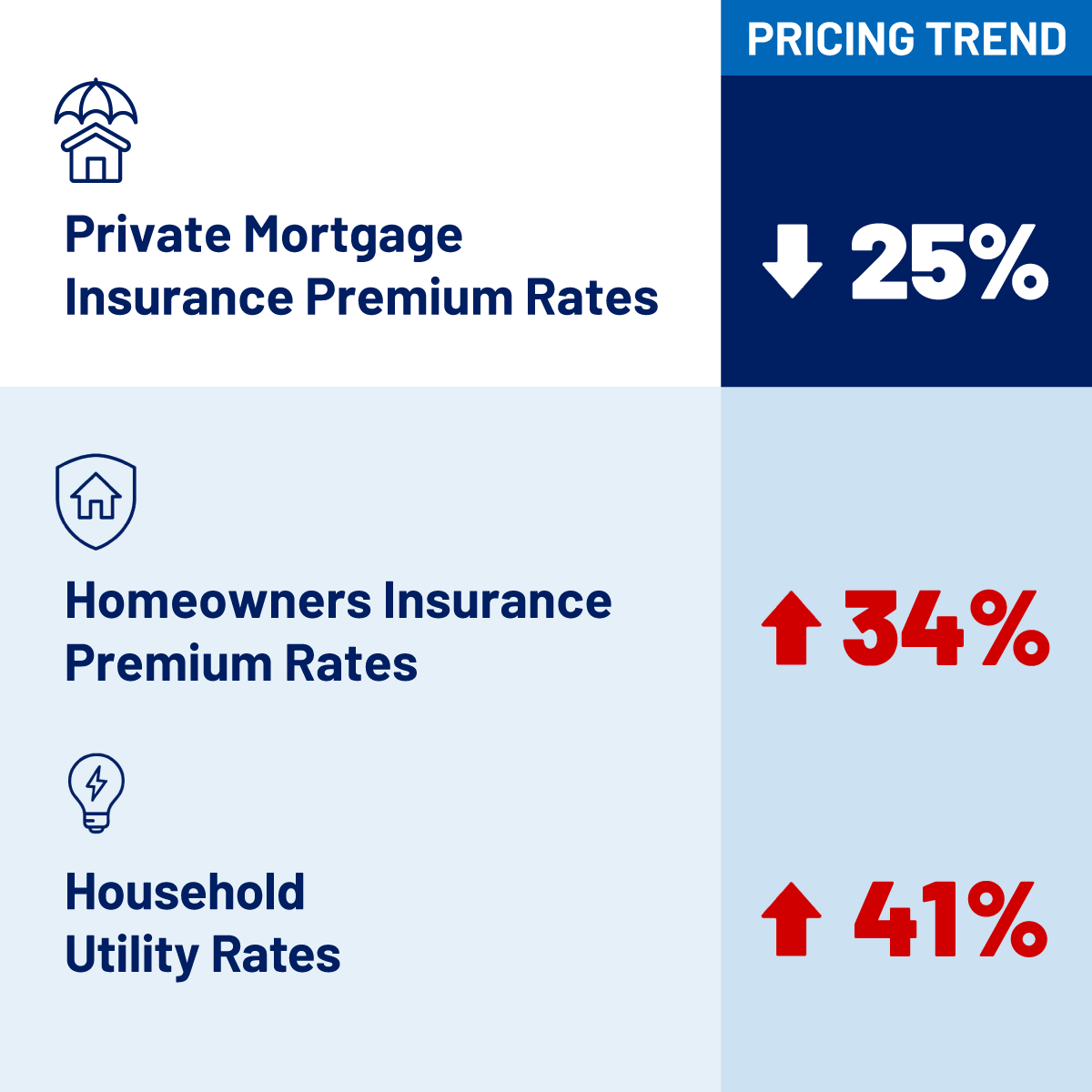

Beyond the potential tax savings, it is important to note that private MI is one of the few costs associated with homeownership that has declined in recent years. Based on publicly released data, private MI premiums have decreased by 25% since 2017, driven by the increased use of risk-based pricing and savings passed to borrowers from the 2017 Tax Cuts and Jobs Act. Private MI premiums trending down are in stark comparison to other prices associated with homeownership. For example, homeowners insurance premium rates and household utility rates have increased 34% and 41%, respectively, in recent years.

As an added benefit, private MI not only helps homebuyers qualify for mortgage financing, but, in most cases, the cost is temporary. Unlike MI premiums paid on vast majority of loans insured by government-backed agencies that cannot be canceled, private MI paid monthly by borrowers can be canceled once the buyer has established a certain amount of equity and automatically terminates when 22% of the original value of the home has been paid off. That leads to lower monthly mortgage payments in the long run, in addition to the immediate benefit that is provided through the tens of thousands of dollars in cash that isn’t necessary to bring to the closing table.

For nearly 70 years, private MI has helped first-time and working-class homebuyers access the American dream of homeownership. Prospective homebuyers can learn more about these benefits and how private MI can help them join the millions of Americans who have saved billions by visiting LowDownPaymentFacts.com.

USMI Statement for the Record on “Diversifying Risk: The Benefits of Reinsurance and Credit Risk Transfers”

On April 22nd, USMI submitted a statement for the record for a hearing of the House Committee on Financial Services Subcommittee on Housing and Insurance entitled “Diversifying Risk: The Benefits of Reinsurance and Credit Risk Transfers”. In the statement, USMI described how private mortgage insurance (MI) is the original form of credit risk transfer (CRT) and, for nearly 70 years, has provided robust first-loss credit risk protection on single-family mortgages that remains in effect regardless of the execution and investor, as well as through all market cycles. It further described how the private MI industry has diversified its capital base with access to traditional reinsurance, forward reinsurance contracts, and capital markets-based transactions that reduce volatility and disperse exposures to mortgage credit risk. USMI continues to engage federal policymakers on prudent housing finance policies that enable access to homeownership opportunities, particularly for creditworthy borrowers without large cash down payments. Read the statement for the record here.

USMI Statement on Benefits Delivered by Trump Administration Tax Policies to First-Time and Working-Class Homebuyers

WASHINGTON — Seth Appleton, President of U.S. Mortgage Insurers (USMI), today released the following statement in recognition of Tax Day:

“President Trump and Congress delivered a tremendous win for hardworking families across the country by reinstating and making permanent the mortgage insurance (MI) premium tax deduction as part of the Working Families Tax Cuts Act. Because of their efforts, beginning with tax year 2026, millions of hard-working American homeowners could receive meaningful tax relief without increasing risk in the housing finance system.”

“It’s not the first time that first-time and working-class homebuyers have benefited from changes to the tax code made by President Trump and Congress. When the Tax Cuts and Jobs Act was signed into law during the President’s first term, the private MI industry passed along savings from lower corporate tax rates directly to homebuyers. Since then, private MI premium rates have decreased by 25% based on in-force premium yields – making homeownership even more affordable for American families.”

For Background:

- Data from U.S. Mortgage Insurers show that the private MI industry helped nearly 800,000 borrowers secure mortgage financing in the past year alone. First-time homebuyers represented approximately 65% of purchasers with private MI.

- During the time in which the MI premium deduction was previously in effect (from 2007-2021):

-

- The MI premium deduction was claimed 44 million times, representing a combined $65 billion in deductions for hardworking Americans.

-

- On average, 3.4 million homeowners claimed the deduction each year.

-

- During tax year 2021, the last year the deduction was available, the average deduction amount was $2,346 per qualified taxpayer.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

Private MI Saved Americans Hundreds of Billions of Dollars, Helped Them Achieve Homeownership Years Sooner

Enabling the American Dream: PMI Saved First-Time, Working-Class Homebuyers $258.1 Billion In Down Payments Due at Closing From 2020-2024

Cost of Private MI, the Most Powerful Financial Tool for Low Down Payment Homebuyers, Also Declined 25% in Recent Years As Measured by In-Force Premium Yields

WASHINGTON — U.S. Mortgage Insurers (USMI), the association representing the nation’s leading private mortgage insurance (MI) companies, released new data showing that in the five-year period between 2020 and 2024, private MI collectively saved American homebuyers more than $258 billion in down payments due at closing, enabling the American Dream for millions of first-time and working-class homebuyers with as little as three percent down, compared to a larger 20% down payment.

For nearly 70 years, the private MI industry has supported access to affordable homeownership for borrowers without large down payments, allowing them to come to the closing table with tens of thousands of dollars less in cash on average and allowing them to access homeownership decades sooner. USMI’s analysis examined the number of homeowners using private MI, average loan amount, and typical down payment for borrowers using loans with private mortgage insurance in each state between 2020-2024 to estimate a total overall savings generated of $258.1 billion during that period.

USMI’s “50 States of Low Down Payment Homebuying” report, released last summer, found that on average, it could take 26 years for a household earning the national median income in 2024 to save 20% plus closing costs for a home at the median national sales price of $412,500. However, with the help of private MI, that time decreases by 65% to purchase a home with 5% down.

“As we mark America’s 250th birthday this year, our data show that private MI saved Americans over $250 billion in cash due at the closing table in just five years alone, making homeownership more affordable and allowing Americans to become homeowners years sooner,” said Seth Appleton, president of USMI. “Private MI is a powerful financial tool that saves prospective homeowners tens of thousands of dollars at closing, and, as an added benefit, eligible homeowners can once again deduct MI premiums from their taxes thanks to the One Big Beautiful Bill Act.”

Starting in tax year 2026, qualifying low down payment homebuyers will once again be able to deduct mortgage insurance premiums on their federal taxes, providing new homebuyers with even more benefits. In 2021, the last year this deduction was previously available, 1.3 million homeowners claimed this deduction, for an average of nearly $2,400 per household.

In addition, private MI premium rates have decreased by 25% since 2017 based on publicly reported in-force premium yields, driven by the increased use of dynamic risk-based pricing and savings passed along to borrowers from the reduced corporate tax rates delivered by the Tax Cuts and Jobs Act signed into law during President Trump’s first term. This trend stands in stark contrast to other costs associated with homeownership, including homeowners insurance premium rates and utility rates.

Prospective homebuyers interested in how private MI can help them save money and achieve the American Dream sooner can learn more at LowDownPaymentFacts.com.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.