WASHINGTON — Lindsey Johnson, President of U.S. Mortgage Insurers (USMI), issued the following statement on the White House’s nomination of Julia Gordon to serve as Assistant Secretary for Housing, Federal Housing Commissioner, Department of Housing and Urban Development (HUD):

“USMI applauds the nomination of Julia Gordon to serve as Federal Housing Commissioner to lead the Federal Housing Administration (FHA). Gordon has broad experience in the housing finance system, specializing in supporting affordable homeownership and consumer protection policies for underserved markets. Her previous work, including nearly six years leading the National Community Stabilization trust (NCST), public service as manager of the single-family policy team at the Federal Housing Finance Agency (FHFA), and four years as senior policy counsel at the Center for Responsible Lending (CRL), will allow her to efficiently address the important issues facing the housing industry. We look forward to working closely with Gordon in seeking to promote a complementary, collaborative, and consistent housing finance system that enables sustainable homeownership for American families while also protecting taxpayers.”

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

USMI President Lindsey Johnson appeared on “Radian On Air” podcast with Radian President of Mortgage and USMI Chairman Derek Brummer. On the episode titled, “National Homeownership Month: Expanding Minority Homeownership,” they discussed the importance of homeownership, barriers for first-time homebuyers, solutions to address low housing supply, and the role of private MI in promoting homeownership.

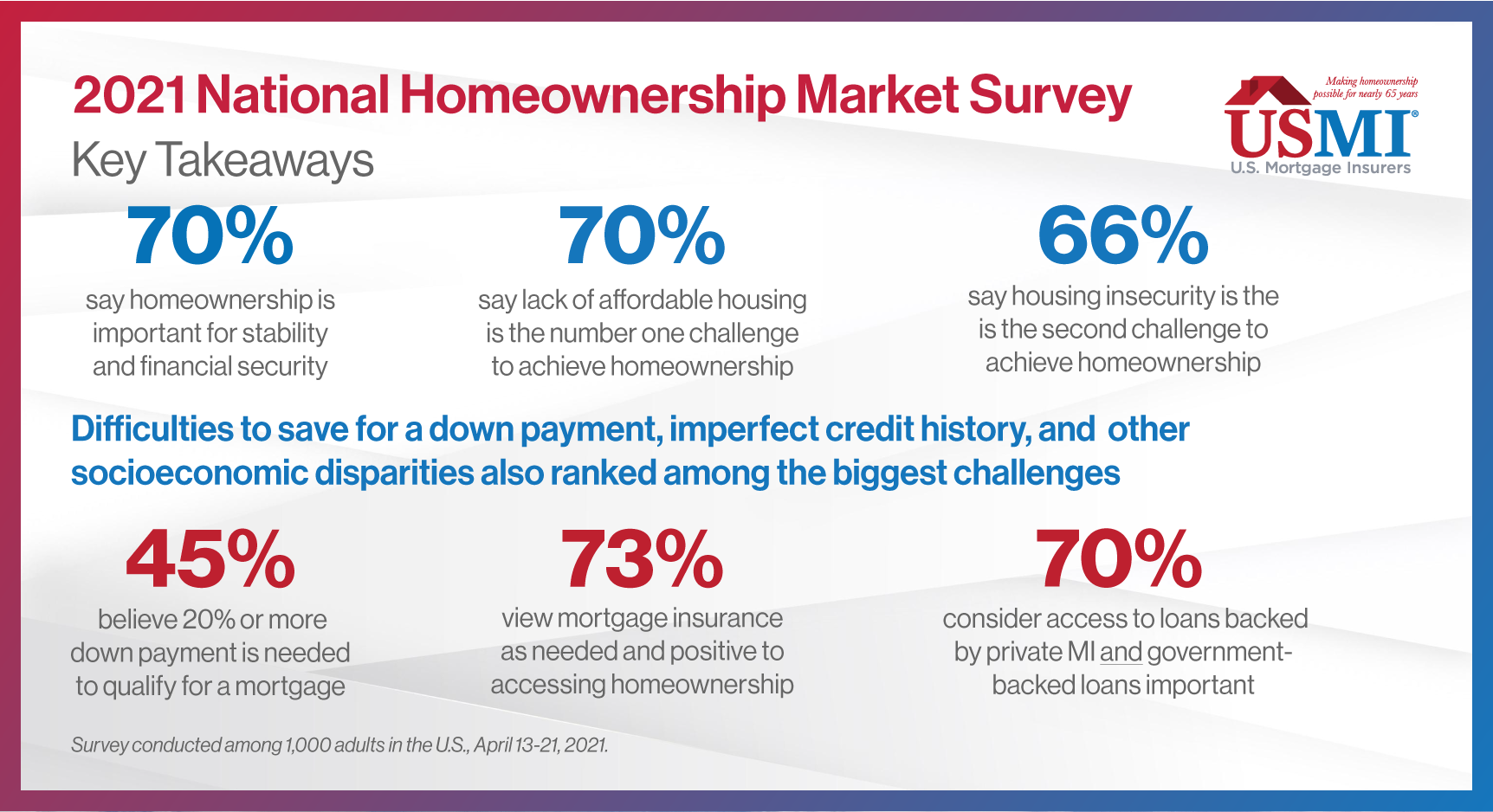

On June 22, USMI released the results of its 2021 National Homeownership Market Survey. ClearPath Strategies fielded the national survey among 1,000 U.S. adults in the general population from April 13-21. Quotas were set to ensure a cross sample of age, gender, race, region, and education as well as homeowners, first-time homebuyers, and prospective homebuyers. The purpose was to understand the perceptions around homeownership, the mortgage process, and the challenges people face when trying to purchase a home.

This blog is the first in a series that will explore the findings from this comprehensive survey around the housing and mortgage markets in the United States. We kick off the series with the seven key takeaways from the national survey. The complete findings from USMI’s national survey are available here.

Owning a home matters. More than 7 in 10 respondents see owning a home as important for stability and financial security. However, as we dig into the other key findings, economic and access gaps lead to challenges to buying a home.

Lack of affordable housing and low supply of housing ranked among the top homebuying challenges. In fact, nearly 7 in 10 respondents ranked the lack of affordable housing as the number one housing challenge and nearly 6 in 10 stated that low housing supply is another top issue. This is contextualized by the current historically low housing supply, which is most acute in the “starter home” segment of the market.

Housing insecurity during the pandemic was also a significant concern for Americans, particularly among minorities. Sixty-six percent of all respondents ranked housing insecurity, including concerns about the ability to make mortgage and rental payments, as the second highest housing challenge. A further dive into the survey findings underscores these economic concerns are particularly acute among minorities. African Americans and Hispanics said that falling behind on rent or mortgage payments was their number one concern. Twice the number of African American respondents (20 percent) and more than one-half times the number of Hispanic respondents (16 percent) reported this concern compared to white respondents (10 percent).

The inability to save for a down payment and imperfect credit history also ranked among the biggest challenges to buying a home. African American (74 percent) and Hispanic (66 percent) respondents reported that in addition to the lack of affordable homes or lack of supply on the market, the inability to save for a down payment (39 percent of all minorities) and imperfect credit history (37 percent of all minorities) are the biggest challenges they face when it comes to buying a home. Of all adults surveyed, 60 percent view “credit score” as having the most impact on the cost of a mortgage, while 81 percent said they understand the factors that impact one’s credit score and 79 percent view credit scores as being fair.

Socioeconomic disparities – such as lower income, lack of intergenerational wealth, limited savings, and the percentage of monthly income dedicated to housing costs – only add to the challenges to buying a home. These factors can lead to lower credit scores and higher overall debt loads to manage, which all can contribute to greater challenges to achieving homeownership. African American and Hispanic respondents rank these issues as more significant challenges compared to white respondents.

Many Americans still do not realize that low down payment mortgages are widely available. Up to 45 percent of all respondents mistakenly believe that you need a down payment of 20 percent or more to qualify for a mortgage. Thirty percent of all adults surveyed indicate that they are not familiar with down payment requirements. In truth, homebuyers can qualify with a down payment as low as 3 percent with private mortgage insurance, and as low as 3.5 percent with a loan backed by the Federal Housing Administration (FHA).

While down payments continue to be a significant challenge, mortgage insurance (MI) is seen as leveling the playing field and respondents express strong support for access to mortgages with MI in both the conventional and government-backed markets. Seventy-three percent of all respondents view mortgage insurance as needed and positive to accessing homeownership. MI provides access to home financing for those who might not otherwise be able to purchase a home due to limited funds for a down payment. Nearly 70 percent of respondents cited that it was important to have access to loans through the conventional market backed by private MI and government-backed loans through the FHA.

June marks the official start of summer and National Homeownership Month. This week, USMI released its 2021 National Homeownership Market Survey, which examined perceptions around homeownership, the mortgage process, and the challenges people face when trying to purchase a home. USMI also released its annual MI in Your State report in early June, which found borrowers were able to access home financing three times sooner in 2020 because of private mortgage insurance (MI). We dig further into these reports and more below.

USMI’s 2021 National Homeownership Market Survey. On June 22, USMI released its 2021 National Homeownership Market Survey. This new research, fielded by ClearPath Strategies to 1,000 adults in the U.S., found that nearly 7 in 10 (69 percent) ranked lack of affordable housing and nearly 6 in 10 (57 percent) ranked low housing supply among the biggest homebuying challenges. The survey also specifically looked at these responses by race to better understand minorities’ perceptions and challenges around homeownership, housing affordability, and the mortgage process. It also revealed that many people continue to not understand the down payment requirements to purchase a home. Housing insecurity (66 percent) was also among the top concerns from respondents. Socioeconomic disparities – such as lower income, lack of intergenerational wealth, limited savings, and the percentage of monthly income dedicated to housing costs – were reported to make these challenges more acute, particularly among minorities.

Black Homeownership Collaborative. In collaboration with more than 100 organizations and individuals involved in the Black Homeownership Collaborative, USMI supports policies that promote equity and work to increase homeownership rates among Black Americans. On June 18, the Collaborative unveiled a solutions-based initiative to close the Black homeownership gap. The Collaborative’s seven-point plan includes homeownership counseling, targeted down payment assistance, housing production, credit and lending reforms, civil and consumer rights enforcement, advancing homeownership sustainability, and marketing and outreach. The goal is to create 3 million net new Black homeowners by 2030. Read more at 3by30.org.

USMI’s MI in Your State Report. On June 2, USMI released its annual MI in Your State report on the role of private MI in all 50 states and the District of Columbia. The report found that home loans backed by private MI increased 53 percent in 2020, with more than 2 million borrowers securing mortgage financing — a record year for the industry’s 65-year-history. The report also found that saving for a 20 percent down payment could take potential homebuyers 21 years — three times longer than it could take to save 5 percent down. Texas, California, Florida, Illinois, and Michigan were the top five states for mortgage financing with private MI. Fact sheets for all 50 states, plus the District of Columbia, are available here.

Supreme Court Decision: Collins v. Yellen. On June 23, the Supreme Court released its opinion for Collins v. Yellen, giving the U.S. President greater control over the Federal Housing Finance Agency (FHFA) and the future of the government-sponsored enterprises (GSEs), Fannie Mae and Freddie Mac. The Court held that “[t]he Recovery Act’s restriction on the President’s power to remove the FHFA Director, 12 USC 4512(b)(2), is unconstitutional.” This provides President Biden with the authority and opportunity to nominate a new FHFA Director who will be in better alignment with the Biden Administration’s policy positions and priorities. The Court also held that GSE shareholders’ statutory claim must be dismissed since the FHFA’s actions regarding the Net Worth Sweep did not exceed its “powers or functions” as a conservator. This is undoubtedly a significant determination for the future of the leadership of FHFA, as well as the future of the GSEs. USMI continues to promote a housing finance system that is backed by private capital, and also promotes sensible reforms to the GSEs that include utility-like regulation of the GSEs.

Following the Court’s opinion, President Biden appointed Sandra Thompson, formerly the Deputy Director of the Division of Housing Mission and Goals, as the Acting Director of the FHFA. Prior to joining the FHFA in 2013, Acting Director Thompson spent more than 23 years at the Federal Deposit Insurance Corporation (FDIC), most recently as the Director of the Division of Risk Management Supervision. Her experience in financial supervision, consumer protection, and outreach will continue to benefit the FHFA and housing finance system. USMI looks forward to continued engagement with Acting Director Thompson and her FHFA colleagues to promote a robust conventional mortgage market and access to affordable mortgage credit.

Federal Agencies Extend Foreclosure Moratoria. On June 24, the White House announced a number of actions to protect renters and homeowners still experiencing financial hardships due to the COVID-19 pandemic. The Administration indicated that the U.S. Department of Housing and Urban Development (HUD), U.S. Department of Veterans Affairs (VA), and U.S. Department of Agriculture (USDA) are extending their foreclosure moratoria for one month, until July 31, 2021, and that homeowners with mortgages insured or guaranteed by the agencies may enter into COVID-related forbearance through September 30, 2021. FHFA followed with a statement that the GSEs are extending their foreclosure moratoria on single family foreclosures and real estate owned (REO) evictions through July 31, 2021. Homeowners with GSE-backed single family mortgages continue to be eligible for COVID-related forbearance.

MI Premium Tax Deductibility Proposal in Congress. On June 18, USMI joined with the Mortgage Bankers Association, National Association of Home Builders, and National Association of REALTORS® on letters to Chairman Richard Neal (D-MA) and Ranking Member Kevin Brady (R-TX) of the House Committee on Ways and Means as well as Chairman Ron Wyden (D-OR) and Ranking Member Mike Crapo (R-ID) of the Senate Finance Committee. The groups expressed their support for making the mortgage insurance premium tax deduction permanent and eliminating the adjusted gross income (AGI) phaseout. Analysis from USMI demonstrates that, even after the doubling of the standard deduction in the 2017 tax law, nearly 2.4 million Americans continue to benefit from this important homeownership deduction. Importantly, nearly 60 percent of the taxpayers taking the deduction had AGIs of less than $75,000, demonstrating the importance of this deduction for low- and moderate-income families. The current phaseout represents a burdensome eligibility criterion for American families to claim the MI deduction and millions of homeowners could benefit from a permanent extension that eliminates the AGI phaseout. In April, USMI sent letters to the Joint Committee on Taxation, House Ways and Means Committee, and Senate Finance Committee outlining the legislative proposal.

Credit Risk Retention Rule. On June 11, USMI joined with several other housing and finance organizations on a comment letter to banking and housing regulators. The letter provided observations and recommendations with respect to the review of certain provisions of the 2014 Credit Risk Retention Rule that was jointly issued by the Office of the Comptroller of the Currency, the Board of Governors of the Federal Reserve System, the FDIC, the Securities and Exchange Commission, the FHFA, and HUD. Following careful analysis of the changes issued by the Consumer Financial Protection Bureau (CFPB) in its final Qualified Mortgage (QM) rule, the organizations expressed strong support for the continued alignment of the Qualified Residential Mortgage (QRM) and QM frameworks.

HUD Confirmations and Nominations. This month, Adrianne Todman was confirmed as HUD’s Deputy Secretary, Damon Smith was nominated to serve as the agency’s General Counsel and Julia Gordon was nominated to serve as the commissioner of the Federal Housing Administration (FHA). Smith previously served as the acting general counsel for HUD in 2014. Gordon had managed the single-family policy team at the FHFA from 2011 to 2012, and more recently, was a member of the FHFA and HUD agency review team for the Biden administration. USMI looks forward to working with HUD leadership and the FHA team on policies to best serve borrowers and responsibly facilitate access to homeownership.

What We’re Listening To: “Radian On Air” Podcast. Lindsey Johnson sat down with Radian President of Mortgage and current USMI Chairman Derek Brummer for the company’s latest podcast episode of “Radian On Air” titled, “National Homeownership Month: Expanding Minority Homeownership.” They discussed the importance of homeownership, barriers for first-time homebuyers, solutions to address low housing supply, and the role of private MI in promoting homeownership. Listen to the full episode here.

What We’re Watching: New American Funding Panel on Down Payment Assistance & Increasing Black Homeownership. On May 20, Lindsey Johnson joined Freddie Mac’s Sam Noel, and Stockton Williams, Executive Director of National Council of State Housing Agencies, in a virtual discussion hosted by New American Funding for its New American Dream initiative. Panelists discussed the pressing problem of bridging the down payment gap, how potential homebuyers can overcome that obstacle, and how to increase and sustain Black homeownership.

What We’re Reading: Redwood Trust’s Employee Home Access Program. In case you missed it, Redwood Trust announced its Employee Home Access Program (“the Redwood Benefit”), an MI benefits program for its workforce that supports employees seeking a path to homeownership. Through the program, Redwood is reimbursing all MI costs to help its employees put down roots in areas of their choosing. Citing limited access to affordable housing supply and challenges to access affordable housing, Redwood CEO, Chris Abate encouraged other corporate leaders to offer MI support for their employees: “If as a corporate leader you’re focused on environmental, social and governance objectives, I urge you to consider this benefit for your employees, too.”

ClearPath Strategies fielded USMI’s 2021 National Homeownership Market Survey of 1,000 adults in the U.S. It was commissioned online April 13-21. Quotas were set to ensure a cross sample of age, gender, race, region, and education as well as homeowners, first-time homebuyers, and prospective homebuyers. The purpose was to understand the perceptions around homeownership, the mortgage process, and the challenges people face when trying to purchase a home.

The survey finds that 7 in 10 say lack of affordable housing is the biggest homebuying challenge in the United States, while many do not understand down payment requirements. Housing insecurity (66 percent) and low supply (57 percent) closely followed. Socioeconomic disparities – such as lower income, lack of intergenerational wealth, limited savings, and the percentage of monthly income dedicated to housing costs – were reported to make these challenges more acute.

“This survey underscores the need to address the nation’s undersupply of housing, and specifically affordable housing, because too many people are being left out of the market or face significant barriers to get into the housing market,” said Lindsey Johnson, President of USMI. “Our survey shows that low- to moderate-income households and underserved communities struggle to become homeowners due to several major factors including low housing supply, lack of affordable housing, and personal economic factors such as imperfect credit score or the inability to afford a 20 percent down payment.”

USMI members continue to help millions of borrowers bridge the down payment gap. USMI supports sensible regulatory and legislative reforms to further address barriers to homeownership and promote an equitable and sustainable housing finance system backed by private capital. In collaboration with more than 100 organizations and individuals involved in the Black Homeownership Collaborative, USMI also supports policies that promote equity and work to increase homeownership rates among Black Americans.

Full survey results can be found here. Press release on the survey can be found here.

2021 National Homeownership Market Survey Also Finds Most Americans Don’t Understand Availability of Low Down Payment Mortgage Options

WASHINGTON — U.S. Mortgage Insurers (USMI) today released its 2021 National Homeownership Market Survey that finds nearly 7 in 10 (69 percent) ranked lack of affordable housing and nearly 6 in 10 (57 percent) ranked low housing supply among the biggest homebuying challenges in the United States. The survey also revealed that many people continue to not understand the down payment requirements to purchase a home. Housing insecurity (66 percent) was also among the top concerns from respondents. Socioeconomic disparities – such as lower income, lack of intergenerational wealth, limited savings, and the percentage of monthly income dedicated to housing costs – were reported to make these challenges more acute. The survey also specifically looked at these responses by race to better understand minorities’ perceptions and challenges to homeownership.

“This survey underscores the need to address the nation’s undersupply of housing, and specifically affordable housing, because too many people are being left out of the market or face significant barriers to get into the housing market,” said Lindsey Johnson, President of USMI. “Our survey shows that low- to moderate-income households and underserved communities struggle to become homeowners due to several major factors including low housing supply, lack of affordable housing, and personal economic factors such as imperfect credit score or the inability to afford a 20 percent down payment.”

USMI’s survey found that when broken down by race these economic factors are even more pronounced. Seventy-four percent of African American and 65 percent of Hispanic respondents reported that in addition to the lack of affordable homes or low supply, the inability to save for a down payment (39 percent of all minorities) and imperfect credit history (37 percent of all minorities) are the biggest challenges they face when it comes to buying a home.

Housing insecurity during the pandemic was also a significant concern among survey respondents, particularly for minorities. The number one concern among African American and Hispanic respondents was falling behind on rent or mortgage payments. In fact, twice the number of African American respondents (20 percent) and more than one and half times the number of Hispanic respondents (16 percent) reported this concern compared to white respondents (10 percent).

“The survey also shows that more education is needed around the mortgage finance process, particularly to ensure more buyers understand that low down payment mortgage options are widely available,” said Johnson.

USMI’s survey found that up to 45 percent of all respondents mistakenly believe that you need a down payment of 20 percent or more to qualify for a home purchase. Another 30 percent indicated that they do not know about down payment requirements. In truth, you can qualify with a down payment as low as 3 percent. The survey also asked respondents about the role of mortgage insurance. According to survey respondents, the top reasons for MI are it “levels the playing field” and “increases lower-income families’ access to homeownership.” A majority of respondents also said it was important to have access to low down payment loans through both the conventional and government-backed markets, such as the Federal Housing Administration (FHA).

USMI members support sensible regulatory and legislative reforms to remove barriers to homeownership, and they promote an equitable and sustainable housing finance system backed by private capital. In collaboration with more than 100 organizations and individuals involved in the Black Homeownership Collaborative, USMI also supports policies that promote equity and work to increase homeownership rates among Black Americans.

ClearPath Strategies fielded USMI’s 2021 National Homeownership Market Survey of 1,000 adults in the U.S. It was commissioned online April 13-21. Quotas were set to ensure a cross sample of age, gender, race, region, and education as well as homeowners, first-time homebuyers, and prospective homebuyers. The purpose was to understand the perceptions around homeownership, the mortgage process, and the challenges people face when trying to purchase a home.

The complete findings from USMI’s national survey are available here.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org

USMI joined Mortgage Bankers Association, National Association of Home Builders, and National Association of REALTORS® in submitting letters to Chairman Richard Neal and Ranking Member Kevin Brady of the House Committee on Ways and Means as well as Chairman Ron Wyden and Ranking Member Mike Crapo of the Senate Finance Committee. The letters recommend that the mortgage insurance premium tax deduction be made permanent and the adjusted gross income (AGI) phaseout be eliminated. The current phaseout represents a burdensome eligibility criterion for American families to claim MI deduction and millions more homeowners would benefit from a permanent extension that eliminates the AGI phaseout. As affordability remains a persistent barrier to homeownership across the country, permanently making the MI premium tax deductible and eliminating the AGI phaseout would support both existing homeowners as well as prospective homebuyers.

Texas, California, Florida, Illinois, and Michigan among top states for mortgage financing with private MI

WASHINGTON — U.S. Mortgage Insurers (USMI), the association representing the nation’s leading private mortgage insurance (MI) companies, today released its annual report on mortgage financing supported by private MI at the national and state levels. The report finds that home loans backed by private MI increased 53 percent in 2020, a record-setting year for the nearly 65-year-old industry, with more than 2 million borrowers securing mortgage financing. Meanwhile, the report finds that saving for a 20 percent down payment could take potential homebuyers 21 years — three times the length of time it could take to save a 5 percent down payment. Texas, California, Florida, Illinois, and Michigan were the top five states for mortgage financing with private MI.

“Access to low down payment loans was more important than ever this past year as many homebuyers weighed other economic concerns during the pandemic. Mortgage insurance levels the playing field and provides lower- and middle-income households with access to mortgage credit, and the more than 2 million borrowers served this past year reached a new milestone for our industry,” said Lindsey Johnson, President of USMI.

Private MI has enabled over 35 million people access to affordable, low down payment mortgages, serving as a bridge for homebuyers to qualify for home financing despite putting less than 20 percent down. The latest USMI report examines the number of borrowers served, the percentage of borrowers who were first-time homebuyers, average loan amounts, and average FICO credit scores. USMI also calculates the number of years to save 20 percent versus 5 percent down payments for each state plus the District of Columbia.

Key findings from the report include:

It could take 21 years on average for a household earning the national median income of $68,703 to save for a 20 percent down payment (plus closing costs), for a $299,900 single-family home, the national median sales price.

The wait time decreases to seven years with a 5 percent down payment insured mortgage — a nearly 67 percent shorter wait time at the national level.

In 2020, the number of homeowners who qualified for a mortgage because of private MI reached over 2 million.

Nearly 60 percent of purchase mortgages went to first-time homebuyers, and more than 40 percent had annual incomes below $75,000. The average loan amount purchased or refinanced with private MI was $289,482.

The private MI industry supported $600 billion in mortgage originations in 2020. Approximately 65 percent was for new purchases while 35 percent was for refinanced loans, resulting in approximately $1.3 trillion in outstanding mortgages with active private MI coverage at year’s end.

The below table shows the top five states in which private MI was used by borrowers to purchase or refinance homes in 2020.

State

Number of Borrowers Helped with Private MI

First-Time Homebuyers

Texas

164,737

58 percent

California

160,103

70 percent

Florida

130,800

55 percent

Illinois

93,976

64 percent

Michigan

72,646

59 percent

Throughout 2020, the private MI industry worked closely with federal policymakers, industry groups, and consumer organizations to support homeowners experiencing financial hardships due to the COVID-19 pandemic. The industry updated its guides and processes to align with the policies of the Federal Housing Finance Agency (FHFA) and government-sponsored enterprises’ (GSEs), Fannie Mae and Freddie Mac, to implement nationwide forbearance programs.

Loans backed by private MI provide protection against mortgage credit risk and are structured to protect the GSEs in the conventional mortgage market. Private MI has proven to be a reliable method for shielding the GSEs, having paid nearly $60 billion in claims since the 2008 financial crisis and housing market downturn.

The complete report is available here, along with fact sheets for all 50 states and the District of Columbia.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org