USMI President Lindsey Johnson appeared on “Best Real Estate Investing Advice Ever” with Joe Fairless to discuss her background in mortgage finance and the role of private mortgage insurance in today’s mortgage system.

Listen here.

USMI President Lindsey Johnson appeared on “Best Real Estate Investing Advice Ever” with Joe Fairless to discuss her background in mortgage finance and the role of private mortgage insurance in today’s mortgage system.

Listen here.

The Honorable Kathleen L. Kraninger

Director

Consumer Financial Protection Bureau

1700 G Street NW

Washington, DC 20552

Dear Director Kraninger:

The undersigned organizations are writing in response to the Consumer Financial Protection Bureau’s (Bureau) rulemaking regarding the definition of a Qualified Mortgage (QM). Our organizations represent diverse housing finance stakeholders, including consumer groups, lenders, and mortgage insurers, and we appreciate the opportunity to provide our joint perspectives in addition to our individual comment letters that were submitted in response to the Bureau’s Advance Notice of Proposed Rulemaking (ANPR). The Ability-to-Repay (ATR) rule in the Dodd-Frank Wall Street Reform and Consumer Protection Act is one of the most important consumer safeguards in the legislation, and the Bureau’s regulations to promulgate and execute it will directly affect access to safe and affordable mortgage finance credit. We all agree that maintaining access to affordable and sustainable mortgage credit should be a key objective of the Bureau’s revised rulemaking.

We appreciate the Bureau’s thoughtful approach to assessing and implementing potential changes to the QM definition. This letter contains our joint recommendation that the Bureau implement a QM definition that relies on measurable underwriting thresholds and the use of compensating factors for higher risk mortgages rather than either a pricing-based QM definition that uses the spread between the annual percentage rate (APR) and the Average Prime Offer Rate (APOR) as a proxy for underwriting requirements (the “APOR approach”) or a hard cut-off at either 43% or 45% DTI.

Specifically, this coalition strongly supports:

1. The continued use of a modified debt-to-income (DTI) ratio in conjunction with certain compensating factors, which could be used in the underwriting process and would provide guidance to creditors on their use; and

2. Significant changes to Appendix Q to rely on more flexible and dynamic standards for calculating income and debt.

Compensating Factors Would Enable Prudent Underwriting and Affordable Access to Credit

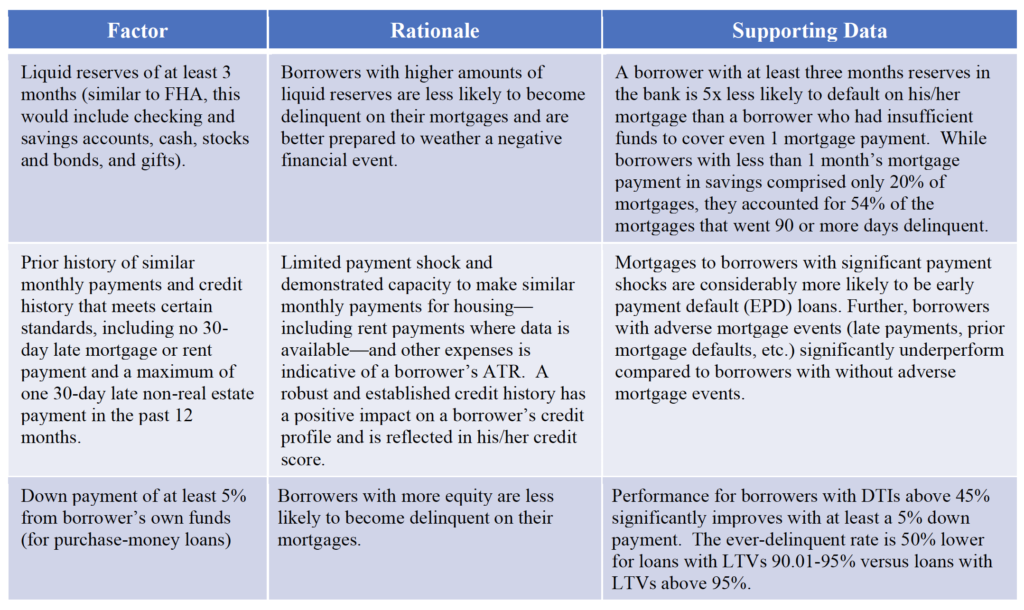

The Bureau should establish a set of transparent mitigating underwriting criteria – “compensating factors” – for mortgages with DTI ratios above 45% and up to 50%. While DTI is not the most predictive factor in assessing a borrower’s ability to repay, it can, in concert with compensating factors, function as a bright line that mitigates undue risk in the conventional market while continuing to provide affordable access to mortgage finance for creditworthy borrowers. Moreover, DTI is a widely and commonly used metric when considering a borrower’s ability to repay in mortgage loan underwriting and is the standard in the current rule issued in 2013. While a higher DTI may indicate increased stress for the borrower and a consequent strain on ability to repay, the presence of other positive credit characteristics – such as liquid reserves, limited payment shock, and/or a down payment from the borrower’s own funds – can mitigate the heightened risk and limit the risk layering that drives loan nonperformance. In fact, the automated underwriting systems (AUSs) used by Fannie Mae and Freddie Mac (the GSEs), as well as proprietary AUSs used by primary market lenders, have always used compensating factors to assess borrowers’ ATR, and such a multifactor approach has long been the standard for manual underwriting throughout the industry.

The efficacy of using compensating factors for high-DTI mortgages is demonstrated by the track record of loans acquired by the GSEs. Rather than introducing undue risk to the housing finance system, these loans have performed well. In fact, high-DTI loans (with ratios between 45.1% and 50%) underwritten using compensating factors outperform loans with lower DTI ratios (between 35.01% and 45%). The lower delinquency rates on the higher DTI loans are almost certainly due to the presence of appropriate compensating factors in the GSEs’ AUSs.

The table below reflects one specific set of compensating factors we believe are appropriate for borrowers with DTIs above 45% and up to 50% that could be tailored for the revised rule. These recommendations are based on: (1) internal analysis and efforts to “back into” the compensating factors currently used by the GSEs to avoid a dramatic shift in the market; and (2) known factors that significantly impact borrowers’ ATR. This is by no means an exhaustive list and we welcome further discussion about compensating factors and their respective predictiveness. The Bureau’s final rule on the QM definition could authorize the GSEs, Federal Housing Finance Agency (FHFA), or an independent standard-setting entity to formulate a transparent list of compensating factors and should make the underlying data and analysis available to the public for ongoing review and assessment to ensure that dynamic compensating factors can be updated to reflect changes in the market and mortgage credit risk environment.

Using an APOR-Only Approach Does Not Meet the Legislative Intent of the Statute and Does Not Appropriately Measure Ability to Repay

The APOR approach is premised on the faulty idea that pricing fully captures credit risk and that, in turn, credit risk is a reasonable marker for ability to repay. In the mortgage industry, a loan’s pricing reflects a number of factors outside of an individual borrower’s credit profile, including a lender’s balance sheet capacity, prepayment speeds, the value of mortgage servicing rights, business goals, and broader economic considerations. With regard to risk, pricing does consider down payment and credit score, but often fails to capture risk-mitigating characteristics such as borrower reserves, DTI ratios, and payment shock.

Any QM definition that relies solely on the statutory ATR requirements or the price of a loan will be seriously flawed. ATR requirements are too broad and do not adequately reflect a borrower’s ability to repay. On the other hand, a loan’s price can be manipulated to gain QM safe-harbor status.

There are several important consumer protection concerns at issue. First, loans made within the QM safe harbor are not, practically speaking, subject to underwriting thresholds/requirements for determining ATR because if a loan meets the product feature requirements along with any other adopted QM standards, no adjudicative body or regulator can “look under the hood” and examine the fuller underwriting process.

Second, if the only underwriting protection is APOR, mortgages could be made to financially vulnerable borrowers at a price just below the safe harbor threshold even though the borrowers’ financial/credit profiles might otherwise call for greater underwriting analysis consideration and ATR protections. This mispricing of risk helped set the 2008 financial crisis in motion.

Third, using this approach assumes creditors are able to uniformly and accurately price risk of repayment, an assumption that was disproven in the financial crisis and ignores market and economic pressures that can drive underpricing of risk.

Fourth, an APOR approach could increase risk within the mortgage finance system as APOR is a trailing indicator of risk and can be procyclical. Therefore, periods of sharply rising rates could cause temporary suspensions in lending that could impact prime loans with higher risk attributes. Additionally, during periods of low rates and loose credit, borrowers run the risk of being overextended.

An APOR Approach Could Make It Harder for Creditworthy Low Down Payment and Minority Borrowers to Obtain Mortgages

Moving from a DTI-based QM standard to an APOR approach could reduce the ability of low down payment and minority borrowers to obtain conventional mortgages. For example, based on 2018 Home Mortgage Disclosure Act (HMDA) data, $11-12 billion in GSE purchase origination volume had loan-to-value (LTV) ratios of >80% and APRs with spreads in excess of APOR + 150 basis points. Further, based on the same dataset, African American and Hispanic borrowers were twice as likely as white borrowers to have mortgages with APRs in excess of the APOR + 150 basis points safe harbor spread.

Many qualified borrowers who are not able to obtain mortgages that meet an APOR standard under a revised QM definition would be denied access to homeownership opportunities while other qualified borrowers in this category would see their loan options reduced. Some mortgages that would normally have been made in the conventional market would gravitate towards the 100% taxpayer-backed FHA, an outcome that is inconsistent with the Administration’s housing finance reform principles and objectives as articulated in the September 2019 reports from the Department of the Treasury and the Department of Housing and Urban Development.

Regardless of the solution chosen, we urge that the transition period from the existing GSE Patch to the new QM framework be sufficiently long to allow market participants adequate time to plan for, and adjust to, new rules and underwriting standards. Any transition to a new QM rule ought to be smooth and well thought-out. Otherwise it risks regulatory uncertainty that might cause mortgage originators to retreat from lending to creditworthy homebuying and refinancing borrowers.

Thank you again for the opportunity to share our collective perspectives on the Bureau’s work regarding the QM definition. The expiration of the GSE Patch and what is developed to replace it will have significant implications for consumers’ access to affordable and sustainable mortgage finance credit. We hope to have a continued constructive dialogue through a robust comment process to result in the best future standard and we welcome the opportunity to serve as resources as the Bureau works toward a proposed, and then final, rule.

Sincerely,

Consumer Federation of America Community

Home Lenders Association

The Community Mortgage Lenders of America

Independent Community Bankers of America

National Association of Federally-Insured Credit Unions

National Association of REALTORS®

National Community Stabilization Trust National Consumer Law Center (on behalf of its low-income clients)

U.S. Mortgage Insurers

CC:

Andrew Duke

Brian Johnson

Mark McArdle

Kirsten Sutton

Thomas Pahl

For a full PDF of this letter, click here.

WASHINGTON — U.S. Mortgage Insurers (USMI) President Lindsey Johnson issued the following statement on the decision made by the U.S. Congress to extend the tax deduction for mortgage insurance (MI) premiums in the H.R.1865 – Further Consolidated Appropriations Act, 2020.

“We are pleased Congress extended the mortgage insurance tax deduction for years 2018 through the end of 2020. Private MI has helped more than 30 million middle-income Americans become homeowners over the last 60 years, and for over 10 years the deductibility of mortgage insurance has helped benefit millions of these hard-working borrowers—the majority of whom made annual incomes of less than $75,000.

“This tax deduction was first available to taxpayers in 2007 and extended multiple times since then on a bipartisan basis. The last deduction expired at the end of 2016, and with this last extension for amounts paid or accrued after December 31, 2017, and before December 31, 2020, lawmakers demonstrate their commitment towards helping low-down payment and first-time homebuyers.

“Over the last six decades, private MI has bridged the gap between a 20 percent down payment and access to mortgage finance credit. In the past year alone, MI helped more than 1.2 million homeowners purchase or refinance homes.”

According to the most recent IRS statistics of income, in 2017 alone more than 2.285 million taxpayers benefited from the MI premium tax deduction. The deduction is available to homeowners with MI who have an adjusted gross income under $100,000 and phases-out for adjusted gross incomes up to $110,000. USMI data show that nearly 60 percent of purchase loans with private MI go to first-time homebuyers and more than 40 percent of borrowers with private MI have incomes below $75,000.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

WASHINGTON — U.S. Mortgage Insurers (USMI) President Lindsey Johnson issued the following statement on the decision made by the U.S. Congress to extend the tax deduction for mortgage insurance (MI) premiums in the H.R.1865 – Further Consolidated Appropriations Act, 2020.

“We are pleased Congress extended the mortgage insurance tax deduction for years 2018 through the end of 2020. Private MI has helped more than 30 million middle-income Americans become homeowners over the last 60 years, and for over 10 years the deductibility of mortgage insurance has helped benefit millions of these hard-working borrowers—the majority of whom made annual incomes of less than $75,000.

“This tax deduction was first available to taxpayers in 2007 and extended multiple times since then on a bipartisan basis. The last deduction expired at the end of 2016, and with this last extension for amounts paid or accrued after December 31, 2017, and before December 31, 2020, lawmakers demonstrate their commitment towards helping low-down payment and first-time homebuyers.

“Over the last six decades, private MI has bridged the gap between a 20 percent down payment and access to mortgage finance credit. In the past year alone, MI helped more than 1.2 million homeowners purchase or refinance homes.”

According to the most recent IRS statistics of income, in 2017 alone more than 2.285 million taxpayers benefited from the MI premium tax deduction. The deduction is available to homeowners with MI who have an adjusted gross income under $100,000 and phases-out for adjusted gross incomes up to $110,000. USMI data show that nearly 60 percent of purchase loans with private MI go to first-time homebuyers and more than 40 percent of borrowers with private MI have incomes below $75,000.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.