As Congress returns from the August recess, regulators closed out the public comment periods for two proposed rules that will substantially impact the housing finance system and borrowers’ access to mortgage credit. Though there has been considerable focus on these important rulemakings over the past several months, policymakers, industry stakeholders, and USMI members remain hard at work supporting the housing finance system as we continue to adapt to and navigate the health and economic consequences of the COVID-19 pandemic. Below are the latest happenings from USMI and key topics we are tracking.

USMI Submits Comments to FHFA on Proposed Enterprise Regulatory Capital Framework. On August 31, USMI submitted its comments to the Federal Housing Finance Agency (FHFA) on the re-proposed Enterprise Regulatory Capital Framework (ERCF). In its comments, USMI emphasized the importance of constructing a balanced, transparent, and analytically justified post-conservatorship capital framework for the government sponsored enterprises (GSEs), Fannie Mae and Freddie Mac. USMI President Lindsey Johnson said that “while sufficient levels of capital are important to the sustainable operation of Fannie Mae and Freddie Mac, excessive capital requirements could have a detrimental effect on mortgage availability.” She also added that these excessive capital requirements could, in turn, push mortgage lending outside of the conventional mortgage market.

USMI also called for more transparent and objective treatment of the GSEs’ counterparties, especially private mortgage insurers that already meet a set of rigorous capital and operational requirements known as the Private Mortgage Insurer Eligibility Requirements (PMIERs). In its comment letter, USMI provided the FHFA with detailed analysis to demonstrate that the capital credit for private MI should be increased to be consistent with historical analysis. Similarly, USMI suggested that the proposed rule should encourage, and not discourage, private capital to absorb more risk in front of the GSEs and taxpayers.

A number of other organizations shared similar assessments and recommendations. The Urban Institute said that “the capital requirements on purchase loans should be lower, and more credit should be given to mortgage insurance.” National Taxpayers Union recommended that “[t]he proposed rule should promote, and not disincentivize private capital—including transferring first-loss credit risk through the use of loan level credit enhancement, such as private mortgage [insurance] and through transferring other layers of credit risk through responsible CRT.”

Finally, USMI noted that the revised capital standard is only one element of comprehensive GSE reform, calling on the FHFA to ensure the GSEs are appropriately regulated, maintain their position as market makers, and preserve the bright line separation between the primary and secondary mortgage markets.

USMI’s full comments on the 2020 proposed rule can be found here, an executive summary can be found here, and its comments on the 2018 proposal can be found here.

FHFA Director Calabria Testifies Before House Financial Services. On September 16, FHFA Director Mark Calabria testified before the House Financial Services Committee and provided an overview of the FHFA’s response to the COVID-19 pandemic and the ERCF. A number of members on the Committee focused their comments and questions on the ERCF with Representative Steve Stivers (R-OH) noting in his comments to Director Calabria that in the ERCF “one of the things that doesn’t get credit is MI coverage that’s above the minimum level.” Congressman Stivers and several representatives from both sides of the aisle also shared concerns that the ERCF would negatively impact and inhibit the CRT market. Director Calabria committed to following up with Congressman Stivers to provide additional details on capital credit for greater MI coverage as well as credit for CRT. Additionally, Chairwoman Maxine Waters (D-CA) as well as Representatives Nydia Velazquez (D-NJ), Bill Foster (D-IL), and Alma Adams (D-NC) shared concerns that the capital requirements outlined in the ERCF are excessive and could increase mortgage rates, especially for minority borrowers. Finally, there were a number of questions and comments related to the GSEs’ exit from conservatorship and other reforms that should happen prior to their exit. Representative Ted Budd (R-NC) questioned Director Calabria about the GSEs pilot programs, IMAGIN and EPMI, and asked, “[s]hould a GSE in conservatorship or in any state be permitted to set capital [standards] for counterparties and then compete against them in the primary market?” Director Calabria shared that this is a regulatory issue that was delayed by COVID-19, but that it is an issue the FHFA is committed to resolving.

USMI Submits Comments on General Qualified Mortgage Definition. On September 8, USMI submitted comments to the Consumer Financial Protection Bureau (CFPB) for its proposed rule on the General Qualified Mortgage (QM) Definition. USMI urged the Bureau “to strike a proper balance between prudent and transparent underwriting standards, and access to affordable and sustainable mortgage finance credit for home-ready borrowers.” It further noted that the current proposed rule could limit access to the conventional market for traditionally underserved borrowers. In its letter, USMI recommended that the QM Safe Harbor should be set at 200 basis points (bps) above the Average Prime Offer Rate (APOR) to ensure the QM definition does not inadvertently limit access to credit for home-ready borrowers, particularly Black and Hispanic borrowers who are twice as likely to have spreads above the proposed 150 bps Safe Harbor threshold.

USMI also agreed with the Bureau’s assessment that a hard 43 percent debt-to-income (DTI) ratio would be the most harmful option for the General QM definition because it would severely limit access to credit in the conventional market. This assessment was consistent with USMI’s 2019 comment letter in response to the CFPB’s Advance Notice of Proposed Rulemaking (ANPR) on the QM Definition. Also consistent with its 2019 comment letter, USMI suggests a better approach to a General QM definition would be a standard that includes a higher DTI threshold up to 50 percent with specified compensating factors.

USMI also urged the CFPB to allow sufficient time for a smooth transition from the temporary QM category, the “GSE Patch,” to the new General QM definition. In August, USMI submitted comments to the CFPB on the GSE Patch, recommending the Bureau set the sunset date for the GSE Patch to be at least six months after the effective date of the General QM definition final rule. USMI wrote that “this time will be critical given the extensive and still undetermined scope of COVID-19 on the financial services industry as it focuses resources on responding to the economic and health fallout from the pandemic.”

Coalition Urges CFPB to Increase the QM Safe Harbor Threshold. USMI also co-signed a joint industry trade letter with 11 other housing policy and consumer advocate groups calling on the CFPB to increase the QM Safe Harbor threshold from 150 to 200 bps over the current APOR. USMI previously discussed the need for increasing the Safe Harbor threshold to mitigate borrower impact in a blog post. USMI wrote that based on its analysis of “mortgage originations, loan performance, market dynamics, and the need to ensure consumer access to affordable mortgage finance, we recommend that this threshold should be pegged to the same threshold as the QM status, which the NPR suggests should be 200 bps.” Doing so would result in a more level playing field and by changing that threshold, would mitigate the impact on borrowers.

ICYMI: USMI Column Published in The Dallas Morning News.On August 17, USMI published its latest column titled, “The Smarter Way to Buy a Home.” USMI breaks down the 20 percent down payment myth and explains how private mortgage insurance can help home-ready buyers get in their house sooner. USMI also highlights that private mortgage insurance is temporary, unlike other low-down payment options. USMI notes that once the borrower reaches 20 percent equity in their house, private mortgage insurance cancels—which is a significant advantage to borrowers considering a low down payment mortgage. Read the column in The Dallas Moring News.

USMI President Lindsey Johnson appeared on the Practical Wealth Show podcast with Curtis May and discussed how private mortgage insurance helps home-ready buyers get in their home sooner.

WASHINGTON — U.S. Mortgage Insurers (USMI), the association representing the nation’s leading private mortgage insurance (MI) companies, submitted its comment letter to the Consumer Financial Protection Bureau (CFPB or Bureau) for its proposed rule on the General Qualified Mortgage (QM) Definition under the Truth in Lending Act (Regulation Z).

“While the CFPB is undertaking a thoughtful process to update the General QM definition, USMI urges the Bureau to strike a proper balance between prudent and transparent underwriting standards, and access to affordable and sustainable mortgage finance credit for home-ready borrowers,” said Lindsey Johnson, President of USMI. “Changes to the QM definition will broadly inform standards and practices across the mortgage market, but the currently proposed rule could limit access to the conventional market for the very borrowers that have traditionally been underserved.”

To ensure the QM definition does not inadvertently limit access to credit for home-ready borrowers, and particularly minority borrowers, USMI recommends that the QM Safe Harbor should be set at 200 basis points (bps) above the Average Prime Offer Rate (APOR). USMI states that this modification to the proposed rule would create a level playing field for the QM standard across the conventional and government mortgage markets, adding that historical delinquency data demonstrates that conventional mortgages with rate spreads between 150 bps and 200 bps are prudently underwritten and sustainable loans that have performed well.

USMI highlights that “[a]ccording to 2019 Home Mortgage Disclosure Act (HMDA) data for conventional low down payment purchase mortgages (>80 percent loan-to-value ratio), Black and Hispanic borrowers were twice as likely as White borrowers to have mortgages with annual percentage rates in excess of the APOR plus 150 bps Safe Harbor spread. Under the proposed rule, many of the borrowers who are above the 150 bps threshold will be left only with the option of a Federal Housing Administration (FHA) loan, which means they have significantly fewer competitive choices in terms of product offerings and loans.”

Further, USMI agrees with the Bureau’s assessment that a hard 43 percent debt-to-income (DTI) ratio cap would be the most harmful option for the General QM definition because it would severely limit access to credit in the conventional market. Consistent with its September 2019 comment letter in response to the CFPB’s Advance Notice of Proposed Rule (ANPR) on the QM Definition, USMI continues to believe that the best approach to a General QM definition would be a standard that includes a higher DTI threshold with specified compensating factors.

In its comments, USMI advises the CFPB to preserve robust and measurable underwriting standards and practices as part of the requirements for “consider and verify” that have been proven to balance access to credit and prudent mortgage underwriting standards. With the elimination of reliance on a DTI cap and the introduction of a “consider and verify” standard for mortgage underwriting, it is critical that the CFPB identify specific requirements or best practices to be used by lenders to qualify for the compliance safe harbor.

Other recommendations to the CFPB include: working closely with federal regulators to implement a transparent and coordinated housing policy that promotes access to credit and prudent mortgage underwriting and creates a level playing field; and reconsidering its approach to adjustable-rate mortgages (ARMs) by amending the NPR to exclude 5-year ARM products from the proposed treatment of short-reset ARMs, as data demonstrates that ≥5-year ARM performance is in line with, or better than, >20-year fixed rate mortgages.

Finally, USMI urges the CFPB to provide sufficient time for a smooth transition from the temporary QM category (known as the government sponsored enterprises or “GSE Patch”) to the new General QM definition. This is particularly important given the extensive and undetermined scope of COVID-19 as the financial services industry appropriately focuses resources on responding to the economic and health fallout from the pandemic.

USMI writes, “[d]epending on the complexity of the finalized revisions to the General QM definition, the significance of the penalties for a violation of the [ability to repay]/QM Rule, and the large number of mortgage industry participants that will need to update their operations and systems, USMI recommends that the Bureau set the sunset date for the GSE Patch to be at least six months after the effective date of the general QM definition final rule. This would allow lenders to use either the GSE Patch or the new General QM definition during the mortgage underwriting process.”

USMI’s full comments on the CFPB’s proposed General QM Definition can be found here; its comment letter to the Bureau on the GSE patch extension can be found here; the 2019 comment letter to the CFPB’s Advance NPR can be found here; and its blog on why the Safe Harbor threshold should be increased can be found here.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org

The Honorable Kathleen Kraninger Director Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20052

Re: Qualified Mortgage Definition under the Truth in Lending Act (Regulation Z): General QM Loan Definition, Docket No. CFPB 2020-0020

Dear Director Kraninger:

U.S. Mortgage Insurers (USMI)1 represents America’s leading providers of private mortgage insurance (MI). Our members are dedicated to a strong housing finance system backed by private capital that enables access to prudent and sustainable mortgage finance for borrowers, while also protecting Fannie Mae and Freddie Mac (the GSEs) and the American taxpayer from mortgage credit-related losses. The MI industry has more than six decades of expertise in underwriting and actively managing mortgage credit risk. Our member companies are uniquely qualified to provide insights on federal policies concerning underwriting standards for the conventional mortgage market, especially given our experience balancing prudent underwriting with access to affordable credit.

USMI appreciates the opportunity to comment on the Consumer Financial Protection Bureau’s (Bureau) NNotice of Proposed Rulemaking (NPR)2 regarding changes to the General Qualified Mortgage (QM) definition. Done right, a revised General QM definition will promote prudent underwriting that enables home-ready borrowers to receive fairly priced and affordable conventional mortgages. USMI and other housing finance stakeholders recognize that changes to the General QM definition will broadly inform underwriting standards and practices across the mortgage market. As discussed below, we are concerned that, as contemplated, the proposed rule could limit access to the conventional market for the very borrowers that have traditionally been underserved.

In our comments below, USMI will discuss the following observations and recommendations:

The Safe Harbor should be set at 200 basis points (bps) above the Average Prime Offer Rate (APOR) to ensure that the General QM definition does not inadvertently limit access to credit for home-ready borrowers, and particularly minority borrowers.

As part of the requirements for “consider and verify,” the Bureau’s final rule should preserve robust and measurable underwriting standards and practices that have been proven to balance access to credit and prudent mortgage underwriting standards.

It is critical that the Bureau work closely with federal regulators to implement a transparent and coordinated housing policy that promotes access to credit, prudent mortgage underwriting, and creates a level playing field.

The Bureau should reconsider its approach to adjustable-rate mortgages (ARMs) and amend the NPR to exclude five-year ARM products from the proposed treatment of short-reset ARMs.

USMI agrees with the Bureau’s assessment that a hard 43% debt-to-income (DTI) ratio cap would be the most harmful option for the General QM definition because it would severely limit access to credit in the conventional market. Consistent with our comment letter dated September 16, 2019 in response to the Bureau’s Advance Notice of Proposed Rulemaking on the QM Definition, we continue to believe that the best approach to a General QM definition would be a standard that includes a higher DTI threshold with specified compensating factors. Please see Appendix A for additional information about a General QM definition that retains a DTI limit.

Overview of QM Definition or the Conventional Market

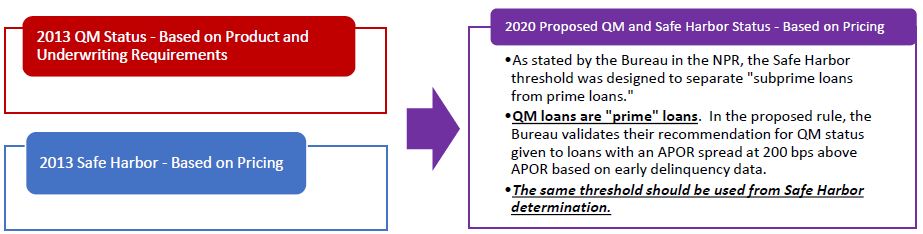

2013 ATR/QM Rule Street Reform and Consumer Protection Act (Dodd-Frank)4 that created specific mortgage product restrictions and required the Bureau to promulgate the Ability-to-Repay/Qualified Mortgage Rule (ATR/QM Rule). The Bureau’s final ATR/QM Rule – issued in June 2013 and made effective on January 10, 2014 – created a General QM category with a 43% DTI limit and requirements concerning product features and points and fees, as well as a temporary QM category for mortgages that met statutory limitations on product features and points and fees and are eligible for purchase by Fannie Mae or Freddie Mac. This temporary QM category has become known as the “GSE Patch,” and the 2013 final rule stipulated that the GSE Patch would sunset the earlier of: (1) the GSEs exiting conservatorship; or (2) January 10, 2021. The GSE Patch has served its intended purpose of maintaining credit availability in the conventional mortgage market and CoreLogic estimates that approximately 16% of 2018 mortgage originations ($260 billion) were made as QM loans by virtue of the GSE Patch. We note that, under the Patch, QM loans have included mortgages with DTI ratios up to 50% with compensating factors.

The Dodd-Frank Act went beyond previous federal consumer protection laws that were largely intended to root out predatory, subprime mortgage products, including the Home Ownership and Equity Protection Act (HOEPA) that defined a class of “higher priced mortgage loans” (HPMLs). HOEPA was later expanded in 2001 and 2008 to provide for a presumed violation of the law when a lender engaged in a pattern of originating higher-priced mortgages without verifying and documenting the borrower’s ATR. Dodd-Frank went beyond HPMLs to address concerns about mortgage underwriting practices by creating specific mortgage product restrictions and requiring the CFPB to promulgate a rule defining “Qualified Mortgage” based on specific underwriting criteria. As promulgated in the 2013 final rule, QM and Safe Harbor were determined by two separate measures: QM status was based on product and underwriting requirements; and Safe Harbor was based on loan pricing. Given that distinction, the different standards made a certain amount of sense. Under the 2020 proposed rule, however, QM status and Safe Harbor are measured using the same metric – price – so there is no longer any reason to set those standards at different spread amounts. As further discussed below, and as the Bureau validates based on early delinquency data, this spread threshold should be set at 200 bps above APOR.

2020 NPR The NPR would remove the 43% DTI limit and instead grant QM status to a mortgage “only if the annual percentage rate (APR) exceeds [the] APOR for a comparable transaction by less than two percentage points as of the date the interest rate is set.” Although the NPR recommends establishing the pricing threshold for defining QM loans at an APR spread of 200 bps over APOR, it also preserves the APR spread over APOR of 150 bps to distinguish between Safe Harbor and Rebuttable Presumption QM loans.

QM Safe Harbor Threshold Should be Increased to APOR Plus 200 bps

Safe Harbor Threshold Will Determine the Conventional Mortgage Market If the final General QM rule maintains a pricing-based QM, the Bureau should increase the spread that is used to delineate Safe Harbor loans and Rebuttable Presumption loans from 150 bps to 200 bps over APOR. This would not only align the delineation with the APOR threshold that the Bureau recommends using to determine QM status, but would also broaden access to the conventional QM market for more home-ready borrowers and create a more level and coordinated housing finance system across the government and conventional mortgage markets.

Determining the Safe Harbor threshold impacts the makeup for the conventional market and who it will be able to serve under a new General QM definition because so few Rebuttable Presumption mortgages have been originated in the conventional market since the final QM rule was implemented in 2014. This is because mortgage lenders have sought to minimize their legal risk by almost exclusively originating QM Safe Harbor loans, thus effectively making the Safe Harbor threshold the standard for QM loans. Home Mortgage Disclosure Act (HMDA) data shows that only 4.6% of purchase QM conventional mortgages and 2.5% of refinance QM conventional mortgages from 2019 were above the APOR plus 150 bps Safe Harbor threshold. However, this data should not be mistakenly interpreted as an indication that there is not a market interest in safely lending above this threshold. In fact, lenders are willing to make loans with pricing above 150 bps when those loans have Safe Harbor status, as evidenced by the fact that loans insured by the Federal Housing Administration (FHA) are five times more likely to be originated with spreads above 150 bps than conventional market loans because the FHA Safe Harbor delineation is set at close to 200 bps. It is also important to look at the performance of loans with higher spreads. Historical GSE 60 plus days delinquency data underscores that loans with spreads up to 200 bps above APOR have performed well, are sustainable mortgages that have been made to creditworthy borrowers, and should qualify for QM Safe Harbor treatment.

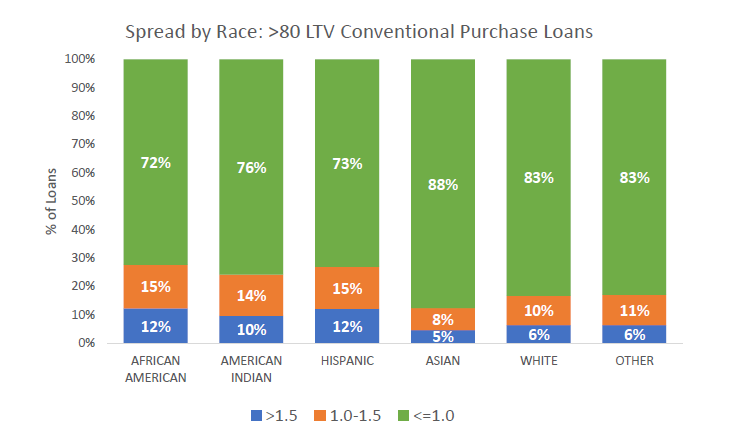

Minority Borrowers are Denied Greater Choice and Access to Credit as a Result of a Safe Harbor Threshold at 150 bps Above APOR Failure to increase the QM Safe Harbor threshold to 200 bps above APOR misaligns the Safe Harbor definition across the government and conventional mortgage markets and results in the same mortgage being a QM Safe Harbor in one channel, but merely a Rebuttable Presumption QM in another, effectively denying that borrower true choice in lenders and mortgage products. This impact is particularly acute for minority borrowers who overwhelmingly rely on low down payment mortgages to purchase their homes. According to 2019 HMDA data for conventional low down payment purchase mortgages (>80% loan-to-value or LTV), Black and Hispanic borrowers were twice as likely as White borrowers to have mortgages with APRs in excess of the APOR plus 150 bps Safe Harbor spread.

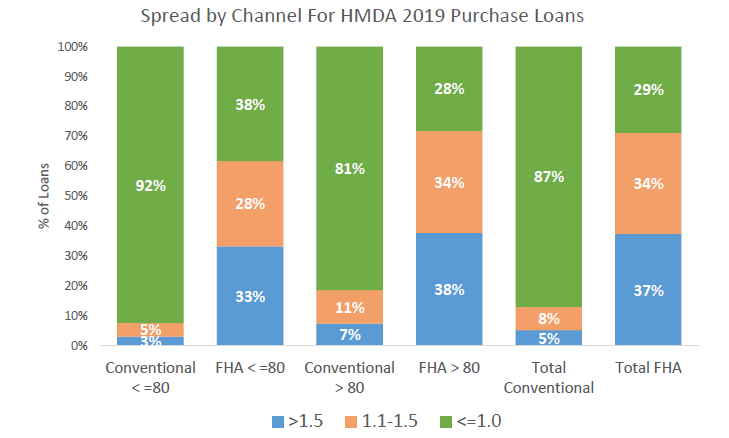

Market Impact from the Calculations for the APOR Spread As discussed below, the different method for calculating the APOR spread for FHA loans results in loans qualifying for FHA QM Safe Harbor status that would merely qualify for Rebuttable Presumption status in the conventional market. As seen in the chart below, FHA loans are six times more likely to have pricing spreads greater than 150 bps above APOR than conventional loans. In 2019, only 7% of high LTV conventional purchase mortgages were above the APOR plus 150 bps Safe Harbor threshold (representing approximately 82,000 borrowers and $23 billion in origination volume) while 38% of FHA’s high LTV purchase mortgages were above the threshold (representing approximately 252,000 borrowers and $63 billion in origination volume).

The de minimis amount of QM Rebuttable Presumption lending in the conventional market strongly suggests that borrowers – most of whom are minorities – with loan spreads above the proposed APOR plus 150 bps threshold would likely have no real choice other than loans insured by the FHA, because their lenders will only want to originate Safe Harbor loans. To underscore this significant reduction in competition, consider that for 2019 there were nearly three times the number of HMDA reporting lenders for conventional purchase loans than FHA purchase loans (approximately 3,200 versus 1,200).

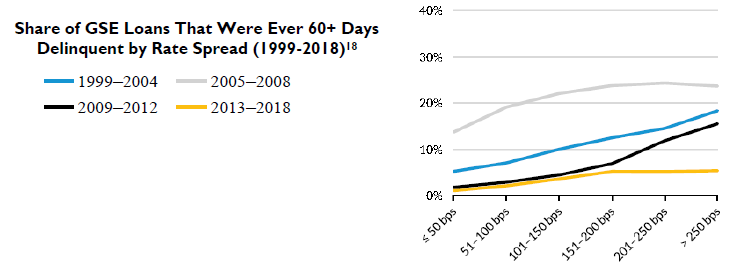

Safe Harbor at APOR Plus 200 bps Results in Safe, Sustainable Mortgages The NPR proposes a pricing threshold to determine whether a loan is a QM and sets the threshold at an APR of up to 200 bps above APOR. The Bureau justifies this threshold using early delinquency data as an indicator of determining consumers’ ATR. The NPR specifically states that “…the Bureau tentatively concludes that this threshold would strike an appropriate balance between ensuring that loans receiving QM status may be presumed to comply with the ATR provisions and ensuring that access to responsible, affordable mortgage credit remains available to consumers” (emphasis added). The proposed QM threshold is predicated on the Bureau’s analysis of early delinquency levels and historical GSE data on 60 plus days delinquent rates demonstrates that increasing the QM Safe Harbor threshold from 150 bps to 200 bps above APOR does not result in a significant deterioration in loan performance that would warrant a different and highly impactful legal characterization. While delinquency is correlated with rate spread, the graph below shows a minimal increase in delinquency rates, especially for the 2013-2018 vintages, which reflect post-crisis enhanced underwriting standards as a result of Dodd-Frank, subsequent rulemakings, and improved lender practices and technologies. This cohort of originations is most indicative of future loan quality and proves that setting the QM Safe Harbor at 200 bps above APOR does not materially increase risk in the system but does indeed expand access to conventional mortgage credit.

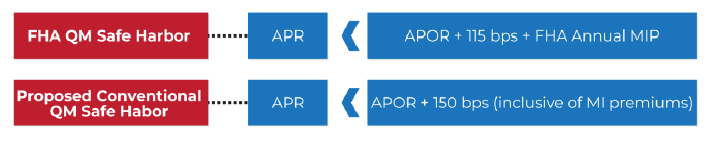

Safe Harbor at APOR Plus 150 bps Creates an Unlevel Playing Field Where Lending is Dictated by Regulatory Standards rather than Borrower Credit Profile Dodd-Frank required the Bureau, U.S. Department of Housing and Urban Developments, U.S. Department of Veterans Affairs, and the Rural Housing Service to create their own QM definitions, including delineating between Safe Harbor and Rebuttable Presumption. The result is a patchwork of standards based on which entity purchases, insures, or guarantees a mortgage loan. In the case of loans insured by the FHA, the delineation between Safe Harbor and Rebuttable Presumption is calculated differently than for conventional loans. This difference has resulted in lenders being much more willing to originate FHA-insured loans with spreads above APOR plus 150 bps because FHA uses a “floating standard” to calculate Safe Harbor that is not impacted by the amount of FHA premium charged. Based on the current FHA Annual Mortgage Insurance Premium (MIP), the FHA QM Safe Harbor is effectively APOR plus 200 bps. As a result, USMI’s recommendation would effectively create a level playing field between FHA and conventional standards for Safe Harbor QMs.

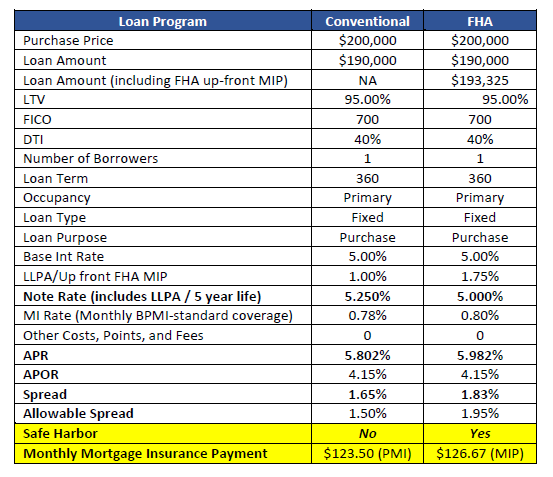

The table below demonstrates how, under the NPR, two loans with identical loan terms and credit characteristics would both be considered QM under the conventional and FHA standards. However, the FHA-insured mortgage would have Safe Harbor status, while the conventional mortgage would merely receive Rebuttable Presumption status. This highlights the current regulatory imbalance that results in many borrowers effectively having no choice on mortgage products because of lenders’ unwillingness to originate Rebuttable Presumption loans.

Another critical difference between the FHA and conventional market calculations is how fees charged by the GSEs and the Government National Mortgage Association (Ginnie Mae) for guaranteeing mortgages affect a loan’s pricing. Unlike the GSEs, Ginnie Mae does not charge risk-based loan-level price adjustments (LLPAs) that factor into a loan’s APR. While the GSEs’ guarantee fees (G-Fees) are in some part based on the attributes of a specific borrower and property, G-Fees and LLPAs also can be –and are – used by the GSEs, Federal Housing Finance Agency (FHFA), and other federal policymakers to accomplish specific public policy or credit risk management goals that can be wholly separate from the credit risk associated with a particular mortgage loan. Further, pricing changes, such as the impact of a finalized rule on GSE capital requirements, adverse market fees based on market developments, or the implementation of new accounting standards have the potential to create temporary credit contractions due to the lag in APOR factoring in new GSE fees and a period of time where APOR is not truly reflective of the mortgage market.

The impact of LLPAs and G-Fees on a conventional loan’s APR could be further magnified by the GSE capital rule that the FHFA recently re-proposed. USMI urges the Bureau and FHFA to study the intersection of these two rulemakings before finalizing either. To the extent that the final capital rule would result in higher G-Fees and/or LLPAs to meet market expectations for a reasonable return on equity (ROE), given the materially higher capital called for under the re-proposed rule, those fees would result in higher APRs and spreads over APOR that could deny a loan Safe Harbor status. USMI urges the Bureau to work with FHFA to ensure clarity and transparency with regard to how the proposed capital requirements could impact the QM Safe Harbor determination.

Implementation of a “Consider and Verify” Standard and Elimination of Appendix Q With the removal of the 43% DTI limit and Appendix Q from the General QM loan definition, an important element of the NPR is the requirement that a lender “consider and verify” a borrower’s income, assets and debt obligations, as well as provides a compliance safe harbor for the use of Bureau approved external standards. USMI continues to have concerns with a QM standard that relies only on the limited Dodd-Frank product restrictions without any other standards or bright line thresholds that would ensure a borrower has a true ATR. The proposed “consider” requirement is especially subjective and the NPR does not currently include specific standards that a lender must meet in order to satisfy this element of the QM definition. In order to provide clarity to market participants, the final rule should identify specific requirements or best practices to be used by lenders to qualify for the “consider and verify” compliance safe harbor. While under the proposed approach in the NPR a specific DTI threshold would be removed from the General QM definition, we think that a properly crafted standard for “consider and verify” could function to encourage the kind of robust underwriting that is needed to assess a borrower’s ATR. For example, one way in which a creditor might document how it “considered” a loan with an elevated DTI would be to use a specific set of underwriting criteria, including compensating factors for consumers with elevated DTIs as recommended in USMI’s 2019 comment letter. Such an approach would be more consistent with the intent of a General QM definition that includes underwriting guardrails and would better ensure creditors appropriately consider critical elements in assessing and ensuring a borrower’s ATR. Further, a set of transparent compensating factors would provide for great consistency across government and conventional mortgage markets and would be more meaningful for considering and determining a borrower’s ATR.

Also related to the “consider and verify” standard, USMI supports the NPR’s proposal to eliminate the requirement that mortgage lenders use Appendix Q to calculate a borrower’s income and debt obligations and to allow other forms of documenting and verifying income, assets, and debt. Widely understood, accessible, and trusted standards for determining income and debt are critical for consistent and prudent mortgage underwriting. However, the static nature of Appendix Q has proven problematic, especially as financial technology (fintech) and workforce trends continue to evolve. By eliminating Appendix Q, the Bureau opens the door to the use of more flexible and dynamic standards and processes for calculating income and debt, which is especially important for creditworthy borrowers with non-traditional forms of income who would be disadvantaged should lenders be required to use Appendix Q.

The NPR notes that lenders would have the flexibility to develop their own income and debt verification standards or could rely on “verification standards the Bureau specifies,” which potentially includes the following: Fannie Mae’s Single Family Selling Guide; Freddie Mac’s Single-Family Seller/Servicer Guide; FHA’s Single Family Housing Policy Handbook; the VA’s Lenders Handbook; and the Field Office Handbook for the Direct Single Family Housing Program, and the Handbook for the Single Family Guaranteed Loan Program of the U.S. Department of Agriculture (USDA).23 These guides and the standards contained within are widely understood by mortgage market participants and, unlike federal regulations, can be, and are, easily revised to account for housing market or broader economic developments or fintech innovation. In the final rule, the Bureau should detail a transparent process by which it will evaluate, approve, and supervise verification standards developed by individual market participants or through a collaborative entity, such as an industry self-regulatory organization.

Notwithstanding the elimination of underwriting thresholds in the General QM definition, in the low down payment segment of the conventional market, MI companies will continue to apply and rely on their underwriting guidelines to assess individual borrowers for purposes of determining ATR and overall creditworthiness. The MI industry’s underwriting guidelines and role as “second pairs of eyes” have proven beneficial with identifying credit risk trends, most notably risk layering and ensuring prudent conventional mortgages.

Regulatory Alignment Realizing this rulemaking’s impact on the size of the conventional market and its underwriting guardrails, it is critical to highlight the historical link between the QM definition and the Credit Risk Retention Rule, which includes an exemption from the five percent retention requirement for assetbacked securities collateralized exclusively by mortgages that are deemed “qualified residential mortgages” (QRMs). Due to the two standards being linked by statute and the requirement that QRM be “no broader than” the definition for QM, the promulgating agencies established a QRM framework that fully aligns with QM. The housing finance system has functioned well under this alignment which has enhanced financial stability, protected investors, promoted compliance, and preserved consumers’ access to affordable credit. The promulgating agencies announced that they would postpone consideration of changes to the QRM standard until June 2021 to factor in any changes to the QM definition. USMI urges housing and financial regulators to preserve the full alignment between the QM and QRM standards in order to preserve current housing market functions and processes.

It is critical that housing finance regulators, including the Bureau, FHFA, and FHA, have a transparent and coordinated approach to the federal government’s housing policy. In addition to preserving the alignment between the QM and QRM standards, USMI urges the Bureau to work closely with the FHFA on the implications for QM due to its proposed GSE capital rule, and with the FHA to align QM standards. Robust coordination will ensure that borrowers are best served by housing market participants and that the federal government, and therefore taxpayers, are adequately protected from losses related to mortgage credit risk.

Treatment of Adjustable-Rate Mortgages The NPR would modify the assessment of ARMs for purposes of determining QM status, such that lenders “must treat the maximum interest rate that could apply at any time during [the] five-year period [after the date on which the first regular periodic payment will be due] as the interest rate for the full term of the loan to determine the annual percentage rate.” This provision would likely reduce the availability of three- and five-year ARM products in the conventional mortgage market. USMI believes that this element of the NPR should be reconsidered and amended to exclude five-year ARM products from the proposed treatment of short-reset ARMs. Based on internal analysis of the performance for five-year ARM products, USMI member company data demonstrates that ≥5-year ARM performance is in line with, or better than, >20-year fixed-rate mortgages. Further, private MIs’ guidelines treat five year ARMs as a “fixed-rate mortgage” based on historical performance.

Implementation of the New General QM Definition The NPR indicates that a new General QM definition will likely not take effect before April 1, 2021, based on the Bureau’s determination that “a six-month period between Federal Register publication of a final rule and the final rule’s effective date would give creditors enough time to bring their systems into compliance with the revised regulations.” The Bureau has also proposed that the GSE Patch expire no earlier than: (1) the GSEs exiting conservatorship; or (2) the effective date of the General QM final rule. As explained in our comment letter on the Bureau’s proposed rule regarding the sunset of the GSE Patch, it is critical that the Bureau provide for a smooth transition from the GSE Patch to the new General QM definition.

Depending on the complexity of the finalized revisions to the General QM definition, the significance of the penalties for a violation of the ATR/QM Rule, and the large number of mortgage industry participants (lenders, brokers, MIs, warehouse lenders, etc.) that will need to update their operations and systems, USMI recommends that the Bureau set the sunset date for the GSE Patch to be at least six months after the effective date of the General QM definition final rule. During this six-month period, lenders should be permitted to use either the GSE Patch or the new General QM definition during the mortgage underwriting process, such that a loan meeting either standard would qualify as a QM. This would afford industry participants an appropriate amount of time to develop, test, and implement new models and business operations in order to smoothly transition to the new General QM framework. More specifically, the six-month overlap period would fix the regulatory gap caused by using the mortgage consummation date for the GSE Patch and the loan application date for the proposed General QM definition.

Further, mortgage market participants, consumers, and the economy as a whole are grappling with an unprecedented level of uncertainty due to the COVID-19 pandemic. The mortgage industry is working diligently to support homeowners directly and indirectly affected by COVID-19, especially through the implementation of broad nationwide mortgage relief for homeowners following the enactment of the “Coronavirus Aid, Relief, and Economic Security Act” (CARES Act). Given the extensive scope of the pandemic and the financial services industry’s appropriate focus on responding to the economic and health fallout from COVID-19, USMI believes that a six-month overlap period would promote an orderly implementation timeframe for the new General QM framework while continuing to assist homeowners throughout the country.

**************************

Thank you again for the opportunity to comment on the proposed General QM definition and your consideration of our recommendations to best balance prudent mortgage underwriting and credit risk management with borrower access to mortgage finance credit. USMI and our member companies appreciate the Bureau’s thorough review of this very important issue and we look forward to continued dialogue as the Bureau proceeds with finalizing and implementing a new General QM definition.

Sincerely,

Lindsey D. Johnson President U.S. Mortgage Insurers

WASHINGTON — U.S. Mortgage Insurers (USMI), the association representing the nation’s leading private mortgage insurance (MI) companies, submitted its comment letter to the Federal Housing Finance Agency (FHFA) for its re-proposed Enterprise Regulatory Capital Framework (ERCF). In its letter, USMI emphasizes the importance of constructing a balanced, transparent, and analytically justified post-conservatorship capital framework for the government sponsored enterprises (GSEs), Fannie Mae and Freddie Mac.

“USMI supports FHFA’s efforts on this important rulemaking. While sufficient levels of capital are important to the sustainable operation of Fannie Mae and Freddie Mac, excessive capital requirements could have a detrimental effect on mortgage availability and costs for consumers, and can inadvertently push mortgage lending outside of the conventional mortgage market,” said Lindsey Johnson, President of USMI. “As FHFA advances this rulemaking, a balance must be struck between prudently managing the GSEs’ risk and protecting taxpayers, while also ensuring that affordable low down payment mortgages remain available for borrowers.”

In its comments, USMI notes the important issues and specific components of the proposed rule that require further attention, as they could potentially create unintended negative consequences. USMI urges the adoption of a final regulation that appropriately balances taxpayer protection and support for the housing markets, consistent with the GSEs’ charters and unique role in the mortgage finance system. Continued access to sustainable, affordable conventional mortgages is particularly important for minorities, lower income individuals, and first-time homebuyers.

Further, USMI advocates for a rule that gives interested parties the opportunity to fully understand the basis for the elements of the proposal and submit beneficial comments to FHFA. USMI, along with other industry participants, continue to be concerned that subjective determinations have the potential to cause great harm to the housing market and are inappropriate if the GSEs are released from conservatorship. Moreover, the current proposed rule would require capital levels that are significantly higher than is necessary for the GSEs’ post 2008 financial crisis and does not reflect the improved loan underwriting required by the GSEs and the Dodd-Frank Act.

USMI’s comments also caution FHFA to avoid adopting a bank capital model given the insurance nature of the GSEs’ business, suggesting they should be subject to an insurance capital framework and that, if necessary, adjustments can be made to account for systemic risk. Additionally, USMI recommends that the risk-adjusted capital rule should be based on credit risk and be as risk-sensitive as possible, having non-credit risk concerns addressed through separate regulatory requirements.

USMI also advocates for more transparent and objective treatment of the GSEs’ counterparties, especially private mortgage insurers that meet a set of rigorous capital and operational requirements known as the Private Mortgage Insurer Eligibility Requirements (PMIERs). USMI adds that private mortgage insurers should not be subject to additional measures of creditworthiness given they already comply with, and exceed, PMIERs. Further, USMI suggests that the proposed rule should promote private capital through the use of both loan level credit enhancement, such as private MI, and through responsible credit risk transfer (CRT). For CRT, the proposed rule should be adjusted to reflect the risk-reduction benefit that is attained by properly priced CRT, and eliminate non-credit risk related buffers that overly penalize CRT to a point that will disincentivize the GSEs’ from de-risking.

Finally, USMI underscores that a revised capital standard is only one element of GSE reform, writing: “The FHFA should use its considerable authority, both as the regulator and conservator, to take steps to ensure that the GSEs are appropriately regulated and do not cross the bright line between primary and secondary mortgage markets. Specifically, we believe that the GSEs should be subject to utility-like regulation, with capped rates of return, restricted to explicitly authorized secondary market activities, and with open and transparent underwriting engines and systems, and publicly disclosed pricing. Doing so would maintain the GSEs as market makers, provide stability through different market cycles, protect taxpayers, and ensure accessibility to sustainable and affordable mortgage finance credit.”

USMI’s full comments on the 2020 NPR can be found here and an executive summary can be found here. Its comments on the 2018 NPR can be found here.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

On June 30, 2020, the Federal Housing Finance Agency (FHFA) published a Notice of Proposed Rulemaking (NPR) on the Enterprise Regulatory Capital Framework (ERCF). On August 31, USMI submitted comments to the NPR, emphasizing the importance of constructing a balanced, transparent, and analytically justified framework. USMI’s full comments can be found here and an executive summary can be found here. In 2018, FHFA issued a prior proposal for changing the risk-based capital framework for the GSEs. USMI also submitted a comment letter, which can be found here.