On February 20, USMI joined a coalition of housing and banking industry stakeholders in sending a letter to banking regulators in support of efforts to modernize bank capital standards to strengthen financial stability and housing affordability. The groups wrote that a revised Basel III Endgame rule should support the critical role that private mortgage insurance (MI) plays in reducing risk for taxpayers while preserving and enhancing mortgage finance options for homebuyers. This includes providing loan-level capital relief commensurate with the level of private MI coverage and adjusting the Eligible Guarantor definition to include private mortgage insurers. USMI and its fellow signatories stand ready to serve as resources to regulators to assist in their bank capital modernization efforts. Click here to read the full letter.

Category: Uncategorized

Letter: Support for Housing for the 21st Century Act

On February 6, 2026, USMI submitted a letter to Speaker Johnson and Leader Jefferies in support of the Housing for the 21st Century Act. USMI urges quick passage of the bill by the U.S. House of Representatives and commends the leadership of the House Financial Services Committee in advancing this important bipartisan legislation. USMI appreciates Congress’ and the Administration’s focus on increasing the nation’s housing stock and helping Americans become homeowners while ensuring safety and soundness in the housing finance system. For the full letter, see here.

Mortgage Insurance: Deductible Once Again Starting Tax Year 2026

Statement: Senate Confirmation of FHA Commissioner, Ginnie Mae President, and FDIC Chairman

WASHINGTON — Seth Appleton, President of U.S. Mortgage Insurers (USMI), released the following statement regarding the Senate confirmation of Frank Cassidy as Federal Housing Administration (FHA) Commissioner, Joseph Gormley as President of the Government National Mortgage Association (Ginnie Mae), and Travis Hill as Chairman of the Board of Directors for the Federal Deposit Insurance Corporation (FDIC) by a vote of 53-43:

“USMI congratulates Frank Cassidy on his confirmation to serve as Assistant Secretary of Housing and Federal Housing Commissioner. Mr. Cassidy brings extensive experience in real estate and housing finance, and we look forward to working with him in this new role in support of mortgage financing that is affordable, accessible, and sustainable for working class families across the country while at the same time promoting safety and soundness in the U.S. housing finance system.”

“USMI further congratulates Joseph Gormley on his confirmation as President of Ginnie Mae, and Travis Hill on his confirmation as Chairman of the FDIC Board of Directors. We look forward to working with Mr. Gormley to promote a safe, sound, and liquid housing finance system, and with Mr. Hill to make prudent updates to bank capital rules that balance access to mortgage credit for low down payment homebuyers with a financially stable housing finance system.”

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Private mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

Letter: Joint Trade Letter to SEC on Prioritizing “Asset-Backed Securities Registration and Disclosure Enhancements”

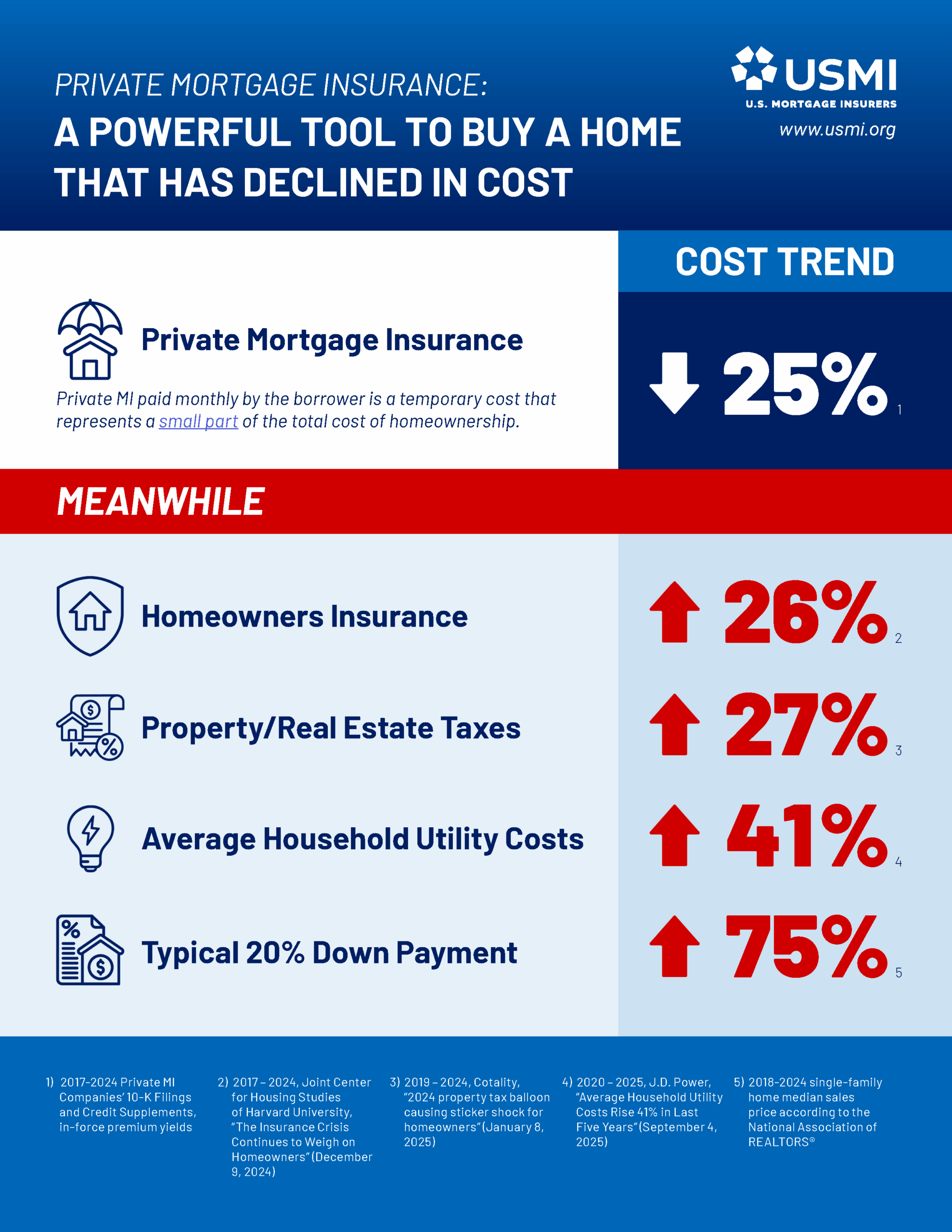

Blog: Private Mortgage Insurance: A Powerful Tool To Buy A Home That Has Declined In Cost

Private mortgage insurance is a powerful tool to buy a home that helps borrowers become homeowners with tens of thousands less at the closing table and without having to save for a 20% down payment. Private MI paid monthly by the borrower is a temporary cost that represents a small component of the total cost of homeownership. What’s more, private MI has declined in cost in recent years. Unlike other costs associated with homeownership that have increased significantly, such as homeowners insurance, property/real estate taxes, average household utilities, and the amount of money needed for a down payment, the cost of private MI has decreased by 25% based on in-force premium yields. See here or below for USMI’s new infographic detailing this striking difference!

Letter: FHFA Repeal of the Fair Lending, Fair Housing, and Equitable Housing Finance Plans

On September 25, 2025, USMI and its member companies provided feedback on the U.S. Federal Housing’s (FHFA) Notice of Proposed Rulemaking (NPR) repealing its “Fair Lending, Fair Housing, and Equitable Housing Finance Plans” regulation. USMI strongly supports FHFA’s work to reduce unnecessary regulatory burdens and believes FHFA’s proposal to repeal this regulation aligns with this work. USMI’s members are key partners to the GSEs, and we look forward to continued collaboration in helping low down payment borrowers affordably and sustainably achieve homeownership sooner in the conventional market. Read the full letter here.

Letter: Letter in Support of Jonathan McKernan’s Nomination

USMI sent a letter to Senate Committee on Finance Chairman Mike Crapo (R-ID) and Ranking Member Ron Wyden (D-OR) expressing strong support for the Honorable Jonathan McKernan to serve as the next Under Secretary for Domestic Finance at the U.S. Department of the Treasury. USMI urges the Committee to swiftly advance Mr. McKernan’s nomination to the full Senate for a confirmation vote. Read the full letter here.

Press Release: One Big Beautiful Bill Act Restores Mortgage Insurance Premium Tax Deduction, Delivering Tax Relief to Middle Class Homeowners

On average, qualified homeowners received a deduction of $2,364 in tax year 2021, the last year it was previously available

WASHINGTON — U.S. Mortgage Insurers, the association representing the nation’s leading private mortgage insurance (MI) companies, welcomes the inclusion of a provision to reinstate and make permanent the deductibility of MI premiums in the One Big Beautiful Bill Act that has now passed the House and Senate and is expected to soon be signed into law by President Trump. In doing so, Congress and the President return a deduction to taxpayers that will provide middle class homeowners with meaningful tax relief without increasing risk in the housing finance system.

Beginning in 2007, the tax code allowed qualified homeowners to deduct MI premiums paid to private MI companies and government agencies, including the Federal Housing Administration (FHA), U.S. Department of Veterans Affairs (VA), and U.S. Department of Agriculture’s (USDA) Rural Housing Service (RHS), from their federal income taxes. This deduction expired after tax year 2021.

During the time it was in effect:

- The MI premium deduction was claimed 44 million times, representing a combined $65 billion in deductions for hardworking Americans.

- 4 million homeowners claimed the deduction each year.

- The average deduction amount was $1,454 per qualified taxpayer.

Previous efforts to reinstate the deduction were supported by lawmakers from both parties and chambers of Congress, as well as a broad coalition of industry groups, housing advocates, and civil rights organizations, as well as lawmakers from both parties and chambers of Congress. Past standalone bills to reinstate the deduction were championed by Sens. Thom Tillis (R-NC) and Maggie Hassan (D-NH), as well as Reps. Vern Buchanan (R-FL-16) and Jimmy Panetta (D-CA-19). More information about MI tax deductibility and USMI’s advocacy to restore the deduction can be found here.

“By restoring this tax deduction, Congress and the President are standing up for American homeowners, homebuyers, and taxpayers,” said Seth Appleton, President of U.S. Mortgage Insurers. “We welcome the inclusion of this deduction in the One Big Beautiful Bill Act and the tax relief it will deliver to millions of hard-working American homeowners with low down payment mortgages.”

USMI’s “2024 National Homeownership Market Survey” found that Americans see private MI as providing benefits including enabling borrowers to qualify for mortgage financing with a down payment as low as 3%, allowing access to homeownership and the ability to begin building equity sooner. Rather than waiting years to save for large down payments, private MI allows homebuyers to get off the sidelines sooner and is a small cost that has declined in recent years due to the 2017 Trump tax cuts and enhanced risk-based pricing. Allowing MI premiums to be deducted at parity with mortgage interest payments further reduces costs for eligible low down payment borrowers.

“Just as Congress has taken action to deliver tax relief to individual taxpayers and support middle class homeowners by reinstating and making permanent the MI premium deduction, the private MI industry serves as a strong, dedicated source of private capital that each and every day enables homeownership for American families and protects taxpayers writ large from the risks of future housing downturns,” said Appleton. “In fact, since the GSEs entered conservatorship, the private MI industry has covered nearly $60 billion in claims, shielding the GSEs and the taxpayers who stand behind them from significant financial losses.”

Recently released data from U.S. Mortgage Insurers show that the private MI industry helped more than 800,000 borrowers secure mortgage financing in 2024. First-time homebuyers who will now be able to claim the MI premium deduction represented approximately 65% of purchasers with private MI. In addition, the industry supported nearly $300 billion in mortgage originations in 2024, according to public filings, representing $300 billion worth of mortgage credit extended to borrowers for which Fannie Mae and Freddie Mac (the GSEs), taxpayers, lenders, and investors are protected from risk of loss.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to affordable and sustainable housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

Press Release: Despite Market Challenges, Private Mortgage Insurers Helped More Than 800,000 Borrowers in 2024 Become Homeowners

Approximately 65% of purchasers that used private MI were first-time homebuyers

WASHINGTON — U.S. Mortgage Insurers, the association representing the nation’s leading private mortgage insurance (MI) companies, released its annual volume data for last year that show the industry helped more than 800,000 borrowers secure mortgage financing in 2024. Approximately 96% of these mortgages were new purchases, and first-time homebuyers represented approximately 65% of purchasers with private MI. In addition, the industry supported nearly $300 billion in mortgage originations in 2024, according to public filings. This represents $300 billion worth of mortgage credit extended to borrowers for which Fannie Mae and Freddie Mac (the GSEs), taxpayers, lenders, and investors are protected from risk of loss.

In 2024, the private MI market also served a large number of low- and moderate-income borrowers. Nearly 35% of those that purchased or refinanced a mortgage with private MI had annual incomes below $75,000, and the average loan amount with private MI was approximately $365,000, according to GSE data. The private MI industry has enabled nearly 40 million people to access affordable, low down payment mortgages in its 68-year history.

“At a time when nearly 80% of Americans believe owning a home is very important to them, despite challenges from interest rates and inventory, private MI continues to make the dream of homeownership possible for millions of people across the country that don’t have access to a 20% cash down payment,” said Seth Appleton, President of USMI.

USMI’s “2024 National Homeownership Market Survey” found that the ability to afford a down payment ranks as the top challenge to buying a home. The survey further found that Americans see private MI as providing benefits including enabling borrowers to qualify for mortgage financing with a down payment as low as 3%, and allowing them to access homeownership and the ability to begin building equity sooner. Rather than waiting years to save for large down payments, private MI allows homebuyers to get off the sidelines quicker and is a small cost that has declined in recent years due to the Trump tax cuts and enhanced risk-based pricing.

By design, private MI serves as the first layer of private capital protecting the housing system against default risk, protecting more than $1.4 trillion in GSE mortgages and shielding taxpayers from risk. The industry has significantly expanded its role as a “second pair of eyes” during mortgage underwriting and post-close processes to serve as a check on fraud and credit quality. In addition, the strength and resiliency of private MI has been reinforced by safeguards and requirements that have been revised and refined over the years, including the Private Mortgage Insurer Eligibility Requirements (PMIERs), which set robust, granular requirements for insuring loans acquired by the GSEs.

“Since the GSEs entered conservatorship, the private MI industry has covered nearly $60 billion in claims, shielding the GSEs and the taxpayers who stand behind them from significant financial losses,” said Appleton. “A strong, dedicated source of private capital that protects taxpayers from the risks of future housing downturns and also works for homebuyers is truly a win-win.”

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to affordable and sustainable housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.