Private MI Saved Americans Hundreds of Billions of Dollars, Helped Them Achieve Homeownership Years Sooner

The Trump administration and policymakers on Capitol Hill are actively working to make homeownership more affordable and attainable – a goal USMI has long championed. Private mortgage insurance (MI) has turned the American Dream of homeownership into reality for tens of millions of Americans, decades sooner, and with tens of thousands of dollars less due at the closing table.

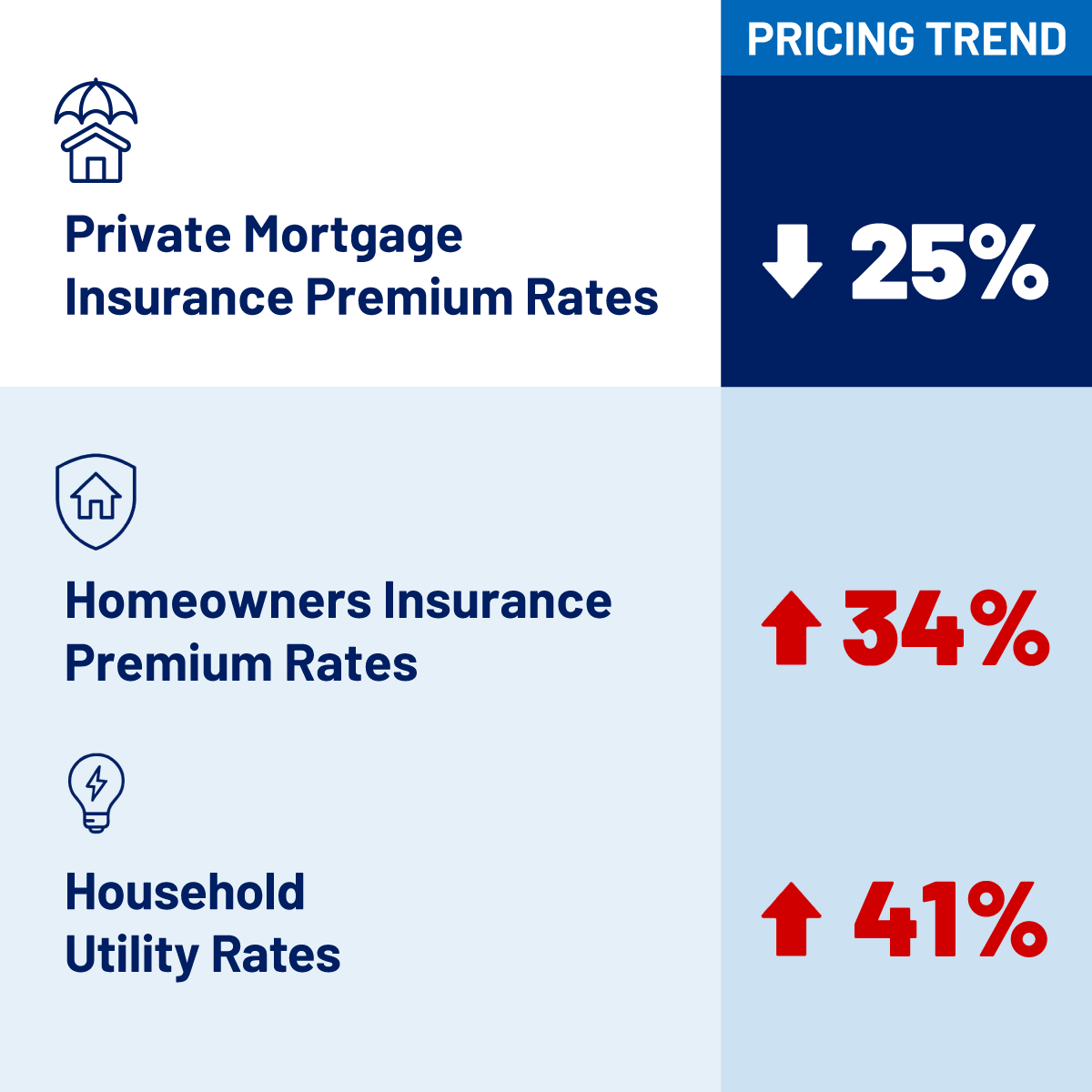

Private MI is not only a powerful financial tool that enables access to affordable and attainable homeownership, but it also has gotten cheaper. Private MI premium rates, as measured by public data on in-force premium yields, have declined 25% or more in recent years, even as many other costs of homebuying and homeownership have climbed. Private MI is also once again tax deductible starting with tax year 2026, thanks to the One Big Beautiful Bill Act, signed into law by President Trump last summer.

As we celebrate America’s 250th birthday this year, we also have reached a fitting milestone: USMI’s analysis estimated that Americans saved over $250 billion in cash due at closing thanks to private MI between 2020 and 2024 alone!

Because private MI protects lenders, the GSEs, taxpayers, and investors from the heightened risk of loss associated with low down payment mortgage loans, private MI allows prospective homebuyers to come to the closing table years sooner and with tens of thousands of dollars less in cash, allowing them to put down as little as three percent compared to a 20 percent down payment. By examining the number of homeowners using private MI, average loan amount by state, and average down payment in each state between 2020-2024, USMI calculated a total overall savings for homebuyers of an estimated $258.1 billion. That’s more than a quarter-trillion dollars that homeowners collectively saved in down payment costs.

What does this mean for the average American family? A USMI report released last summer found that a household earning the national median income of $80,610 might take 26 years to save 20% (plus closing costs) for a $412,500 home, the median sales price for a single-family home in 2024. By using private MI and purchasing a home with five percent down, the time decreases by 65% and allows homebuyers to access homeownership with $60,000 less needed in savings, allowing them to begin building generational wealth, equity, and memories years sooner.

It’s a common myth that a 20% down payment is necessary to buy a home and a 2024 USMI survey found that the ability to save up for a down payment is one of the biggest challenges that Americans face when buying a home.

Yet, with the help of private MI, millions of American homebuyers have discovered that this barrier can be overcome. In 2024 alone, more than 800,000 homebuyers across all 50 states secured home financing with low down payments with the help of private MI. First-time buyers represented 65% of purchase loans backed by private MI in 2024, a seven percent increase over the past five years. Using private MI allowed these individuals to access homeownership sooner while retaining more of their savings, which can significantly help homeowners who may experience unexpected costs such as home repairs or temporary interruptions in income.

Private MI premium rates have also declined 25% in recent years! This is thanks to the increased use of risk-based pricing and savings passed along to borrowers from the reduced corporate tax rates delivered by the Tax Cuts and Jobs Act signed into law during President Trump’s first term. This trend stands in stark contrast to other costs associated with homeownership that have increased in recent years, including homeowners insurance premium rates and utility rates.

Private MI not only helps homebuyers qualify for conventional mortgage financing sooner – for most, the cost is temporary. Unlike the MI premiums paid on the vast majority of loans insured by the Federal Housing Administration (FHA) and other government-backed programs, which typically cannot be cancelled, private MI paid monthly by the borrower can be cancelled once a certain amount of equity is established, leading to lower monthly mortgage payments in the long term in addition to the immediate benefits it provides through tens of thousands of dollars less due at closing.

Additionally, starting next tax season, there will be an additional way that private MI puts money back in the pockets of qualifying homeowners. The One Big Beautiful Bill Act, passed last July, reinstated and made permanent the deductibility of MI premiums beginning in tax year 2026. The return of the deduction stands to once again benefit taxpayers and provide working-class homeowners with meaningful tax relief without increasing risk in the housing finance system. From 2007 through 2021, millions of homeowners claimed the MI tax deduction, allowing them to save more of their hard-earned dollars for combined deductions of $65 billion. In the last year it was available, qualifying taxpayers received back an average of nearly $2,400. For American families, that’s real money — enough to cover monthly bills, save for retirement, or help with school expenses. Thanks to the One Big Beautiful Bill Act, that tax relief is now back for good.

For decades, private MI has supported the American Dream of homeownership, and USMI members stand ready to work alongside Congress and the Administration to continue to enable the American Dream for first-time and working-class homebuyers. If you are interested in learning more about how private MI can help you save money and get to the closing table sooner, learn more at LowDownPaymentFacts.com.