Resource Filter: Reports

Press Release: New Report, “Private Mortgage Insurance: Stronger and More Resilient”

Over 10 Years of Reforms and Continued Evolution Make Private Mortgage Insurers Stronger and More Resilient

Industry has facilitated affordable, low down payment mortgages for over 33 million households, contributing to a more stable housing finance market

WASHINGTON — U.S. Mortgage Insurers (USMI), the association representing the nation’s leading private mortgage insurance (MI) companies, today released a report that highlights the many regulatory and industry-led reforms taken since the 2008 financial crisis to improve and strengthen the role of private MI in the nation’s housing finance system. The report, “Private Mortgage Insurance: Stronger and More Resilient,” analyzes the various steps the industry and regulators undertook and continue to take to ensure sustainable mortgage credit through all market cycles and to better serve low down payment borrowers in the conventional market, especially during critical times such as the present.

“Though private mortgage insurers have been a crucial part of the housing finance system for more than 60 years, this is definitely ‘not your father’s’ MI industry. Enhanced capital and operational standards, as well as increased active management of mortgage credit risk, including through the distribution of credit risk to the global reinsurance and capital markets, has put the industry in a stronger position,” said Lindsey Johnson, President of USMI. “These enhancements will enable the industry to be a more stabilizing force through different housing cycles — including the current COVID-19 crisis — which greatly benefits the GSEs and taxpayers and enhances the conventional mortgage finance system.”

The report also highlights the steps the industry has taken since the beginning of the pandemic to support the federal government foreclosure prevention programs, including the announcements made by Fannie Mae and Freddie Mac regarding forbearance programs and other mortgage relief available to support borrowers impacted by COVID-19. USMI members have focused their efforts on helping borrowers remain in their homes by supporting their lender customers during these challenging times.

Among the enhancements to the industry in the last several years, the report outlines and analyzes the following:

- Private Mortgage Insurer Eligibility Requirements (PMIERs) – Adopted in 2015 and updated in 2018 and 2020, PMIERs nearly doubled the amount of capital each mortgage insurer is required to hold. USMI members collectively hold more than $5.1 billion in excess of these requirements.

- New Master Policy – Updated terms and conditions from mortgage insurers for lenders, which provide lenders with greater clarity pertaining to coverage.

- Rescission Relief Principles – First published in 2013 and updated in 2017, these principles allow MIs to offer day-one certainty to lenders of coverage, including automatic relief after 36 timely payments.

- MI Credit Risk Transfer (MI-CRT) Structures – Private MI companies have transferred $41.4 billion in risk on over $1.8 trillion of insurance- in-force (IIF) since 2015—through both reinsurance and insurance-linked notes.

Through the programmatic execution of MI-CRT transactions, the industry continues to transition the business into an aggregate-manage and distribute model for mortgage credit risk. The implementation and expansion of MI-CRT programs have demonstrated the industry’s ability to tap multiple sources of capital to support new business and actively manage and distribute risk.

Since 1957, the MI industry has served the U.S. government and taxpayers as an effective and resilient form of private capital, standing as the first layer of protection against risk and mortgage defaults. Importantly, MI has enabled affordable, low down payment homeownership for more than 33 million people. In 2019 alone, more than 1.3 million borrowers purchased or refinanced a loan with private MI, accounting for nearly $385 billion in new mortgages.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org

Strength of MI Report

USMI’s report, “Private Mortgage Insurance: Stronger and More Resilient,” highlights the many regulatory and industry-led reforms taken over the last decade to improve and strengthen the role of private mortgage insurance (MI) in the nation’s housing finance system. The report analyzes the various regulatory enhancements and the industry-led initiatives that private MIs have taken and continue to take to ensure sustainable mortgage credit through all market cycles and to better serve low down payment borrowers in the conventional market, especially during critical economic times. Click below to read the report.

The report also highlights the steps the industry has taken since the beginning of the COVID-19 pandemic to support the federal government foreclosure prevention programs, including the announcements made by Fannie Mae and Freddie Mac regarding forbearance programs and other mortgage relief available to support borrowers impacted by COVID-19. USMI members have focused their efforts on helping borrowers remain in their homes by supporting their lender customers during these challenging times.

Among the enhancements to the industry in the last several years, the report outlines and analyzes the following:

- Private Mortgage Insurer Eligibility Requirements (PMIERs) – Adopted in 2015 and updated in 2018 and 2020, PMIERs nearly doubled the amount of capital each mortgage insurer is required to hold. USMI members collectively hold more than $5.1 billion in excess of these requirements.

- New Master Policy – Updated terms and conditions from mortgage insurers for lenders, which provide lenders with greater clarity pertaining to coverage.

- Rescission Relief Principles – First published in 2013 and updated in 2017, these principles allow MIs to offer day-one certainty to lenders of coverage, including automatic relief after 36 timely payments.

- MI Credit Risk Transfer (MI-CRT) Structures – Private MI companies have transferred $41.4 billion in risk on over $1.8 trillion of insurance- in-force (IIF) since 2015—through both reinsurance and insurance-linked notes.

Download the full report here.

Press Release: New Report Finds Low Down Payment Mortgage Lending Increased in 2019, Meanwhile Saving for a 20 Percent Down Payment Could Take 21 Years

WASHINGTON — U.S. Mortgage Insurers (USMI), the association representing the nation’s leading private mortgage insurance (MI) companies, today released its annual state-by-state report on low down payment mortgage lending. The report finds the number of low down payment loans backed by private MI increased 22.9 percent in 2019; meanwhile saving for a 20 percent down payment may take potential homebuyers 21 years to save — three times the length of time it could take to save a 5 percent down payment. USMI also found that the top five states for low down payment home financing with private MI were Texas, California, Florida, Illinois, and Ohio.

“Last year, over 1.3 million homeowners purchased a home or refinanced an existing mortgage with less than a 20 percent down payment using private mortgage insurance,” said Lindsey Johnson, president of USMI. “Given the current economic environment and the desire of many people to keep more cash on-hand, low down payment loans are more important than ever. Loans backed by private MI are a great option as a time-tested means for accessing homeownership sooner while still providing credit risk protection and stability to the U.S. housing system.”

The report examines the number of borrowers helped, the percentage of borrowers who were first-time homebuyers, average loan amounts, and average FICO credit scores. USMI also calculates the number of years to save a 20 percent versus a 5 percent down payment for each state plus the District of Columbia.

Key findings from the report:

- It could take 21 years on average for a household earning the national median income of $63,179 to save for a 20 percent down payment (plus closing costs), for a $274,600 single-family home, the national median sales price.

- The wait time decreases to 7 years with a 5 percent down payment insured mortgage — a nearly 67 percent shorter wait time at the national level.

- In 2019, the number of homeowners who qualified for a mortgage because of private MI reached over 1.3 million, nearly 60 percent of purchase mortgages went to first-time homebuyers, and more than 40 percent had annual incomes below $75,000. The average loan amount purchased or refinanced with MI was $269,072.

- Over the last five years, the role of private MI in the low down payment sector increased from 34.8 percent of the insured market in 2015 to 44.7 percent in 2019.

The below table shows the top five states in which MI was used by borrowers to purchase or refinance homes in 2019.

| State | Number of Borrowers Helped with Private MI | First-Time Homebuyers |

| Texas | 105,158 | 56 percent |

| California | 103,120 | 68 percent |

| Florida | 88,360 | 55 percent |

| Illinois | 58,654 | 64 percent |

| Ohio | 51,167 | 59 percent |

Private MI serves as a bridge for creditworthy homebuyers to qualify for home financing despite a low down payment. It provides protection against mortgage default credit risk and is structured to protect the government sponsored enterprises (GSEs), Fannie Mae and Freddie Mac, in the conventional mortgage market.

The complete report is available here, along with fact sheets for all 50 states and the District of Columbia.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

Press Release: Private Mortgage Insurers Transfer Nearly $34 Billion in Risk on Nearly $1.3 Trillion of Insurance-in-Force from 2015-2019

USMI releases details on the developments and growth of private mortgage insurance credit risk transfer

WASHINGTON — U.S. Mortgage Insurers (USMI) today announced that private mortgage insurance (MI) companies transferred nearly $34 billion in risk on nearly $1.3 trillion of insurance-in-force from 2015 to 2019. USMI released details on the developments and growth of the MI credit risk transfer (MI CRT) market, which outlines the types of structures being used by the industry to transfer risk to reduce volatility and exposure of mortgage credit risk within the mortgage finance system, including to the government sponsored-enterprises (GSEs), and therefore taxpayers. It also finds that active adoption of CRT by private mortgage insurers has transformed the industry to help better insulate it from the cyclical mortgage market and enhanced their ability to be more stable, long-term managers and distributors of risk.

“Through innovative new MI CRT structures, the industry is taking additional steps to enhance MI resiliency and the risk protection provided to the conventional mortgage market. MI CRT demonstrates that MI companies are sophisticated experts in pricing and actively managing mortgage credit risk,” said Lindsey Johnson, President of USMI. “Private MI plays a critical function in the housing finance system by serving as the first layer of protection against mortgage defaults. MI is also one of the only sources of private capital that has been available through all market cycles. After the financial crisis, the MI industry improved its safety and soundness through enhanced capital and operational standards, which in turn made us more resilient to withstand severe economic stress.”

USMI examined the two main MI CRT structures: Reinsurance and Capital Markets. It found that mortgage insurers have executed 18 reinsurance deals since 2015, transferring over $25 billion of risk on over $530 billion of insurance-in-force. As for the Capital Markets structure, the industry introduced MI Insurance Linked Note (ILN) programs beginning in 2015. Since then, mortgage insurers have issued 19 ILN deals, transferring $7.8 billion of risk on over $730 billion ofinsurance-in-force.

“While the MI industry has distributed credit risk for decades, these innovative CRT structures adopted by the industry in 2015 have transformed it from a ‘buy-and-hold’ into an ‘aggregate-manage-and-distribute’ model,” said Johnson. “The financial risk management approach of private MI companies has become much more countercyclical and significantly benefits the housing finance system.”

Because private mortgage insurers typically hold a portion of the first loss there is an alignment of incentives that ensures quality underwriting continues to be done by the industry, which reduces investors’ risk exposure, and ensures quality control on risk for investors and within the broader financial system. The investor base in these transactions continues to grow exponentially as the frequency of transactions increases, and the MI CRT investors to date represent trillions of dollars of private capital under management that provides a stable, deep pool of liquidity for the market.

“The MI CRT structures underscore the resilient nature and benefits of MI and the private capital it supplies to the housing market, safeguarding taxpayers against mortgage defaults, and ensuring that the private MI industry will continue to play a vital role in the mortgage finance system,” added Johnson.

More information on MI CRT is available here.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership.

Report: Urban Institute Report Highlights Role Private Mortgage Insurers Have Played to Protect Taxpayers, Expand Access to Homeownership for 60 Years

For 60 years, private mortgage insurance (MI) has helped more than 25 million families become successful homeowners. To commemorate this milestone, the Urban Institute examined the industry’s history and the positive role MI has served for homebuyers and the mortgage finance system overall. Urban notes in its study, “[p]rivate mortgage insurers have played a crucial role over the past six decades enabling first-time homebuyers to gain access to high-[loan-to-value] conventional financing while reducing losses for the GSEs.” The report confirms that the presence of private mortgage insurance makes it easier for creditworthy borrowers with limited down payments to access conventional mortgage credit. This is the primary function of MI – to help borrowers qualify for home financing.

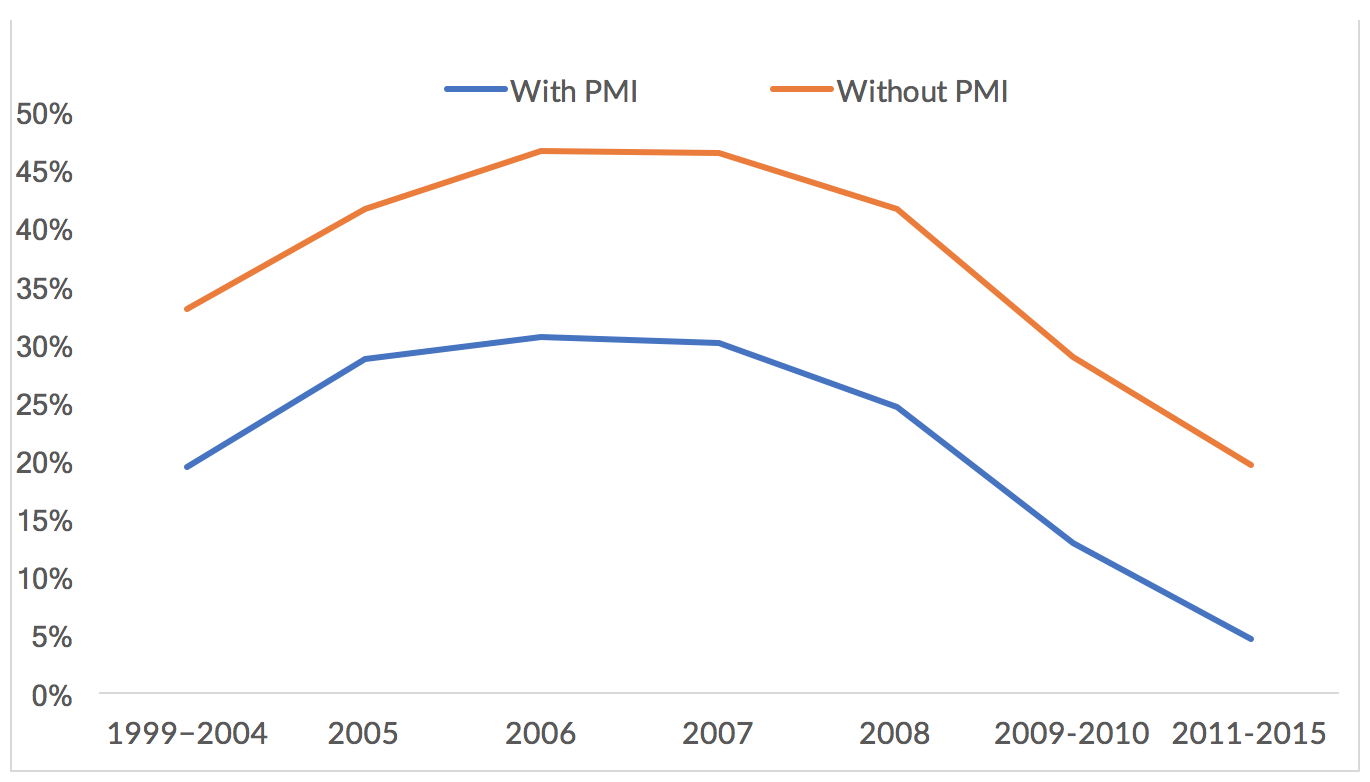

The report also focuses on the role MI plays to reduce taxpayers’ exposure to mortgage credit risk. MI insures the first-loss credit risk to the government sponsored enterprises (GSEs), Fannie Mae and Freddie Mac, helping to reduce GSE losses, and therefore taxpayers’ losses, on defaulted mortgages. And historical experience and data show MI works. Urban found that GSE loans with MI consistently have lower loss severities than those without MI. In fact, for nearly 20 years, loans with MI have exhibited lower loss severity each origination year. The Urban analysis shows that “for 30-year fixed rate, full documentation, fully amortizing mortgages, the loss severity of loans with PMI is 40 percent lower than [loans] without.”

Loss Severity for GSE Loans with and without PMI, by Origination Year Groupings

Sources: Fannie Mae, Freddie Mac, and the Urban Institute.

Note: GSE = government-sponsored enterprise; PMI = private mortgage insurance. The GSE credit data are limited to 30-year fixed-rate, full documentation, fully amortizing mortgage loans. Adjustable-rate mortgages and Relief Refinance Mortgages are not included. Fannie Mae data include loans originated from the first quarter of 1999 (Q1 1999) to Q4 2015, with performance information on these loans through Q3 2016. Freddie Mac data include loans originated from Q1 1999 to Q3 2015, with performance information on these loans through Q1 2016.

This data, coupled with the more than $50 billion in claims our industry paid since the GSEs entered conservatorship—which represents over 97% of valid claims paid, underscores how MI provides significant first-loss protection for the government and taxpayers. By design, MI provides protection before the risk even reaches the GSEs’ balance sheets. As the government explores ways to further reduce mortgage credit risk while also ensuring Americans continue to have access to affordable home financing, the data shows private MI is an important solution.

The MI industry, like nearly all other industries in financial services, was tested like never before through the financial crisis. Urban’s report acknowledges the challenges the industry has overcome from the financial crisis and the opportunities ahead for the industry. Coming out of the crisis, the MI industry is even stronger with more robust underwriting standards, stronger capital positions, and improved risk management. Additionally, in the last two years, private mortgage insurers have materially increased their claims paying ability in both good and bad economic times due to new higher capital standards under the Private Mortgage Insurance Eligibility Requirements (PMIERs).

Urban notes that the industry “should be more resilient going forward” because of the important changes applied to the industry today – including the enhanced capital, operational, and risk standards ‒ and highlights the broad agreement among parties studying GSE reform for the need to reduce the government’s footprint and increase the role of private capital. These developments have helped strengthen the industry and new reforms can allow MI to take on an even greater role to continue protecting taxpayers and expanding access to homeownership for the next 60 years and beyond.

Report: Assessing Proposals to Reform America’s Housing Finance System

Nearly a decade after the financial crisis, the housing finance system remains largely structurally unreformed. There have been several legislative pushes for comprehensive reform after American taxpayers provided $187 billion in bailout assistance to Fannie Mae and Freddie Mac (the “GSEs”) and since both GSEs were placed into conservatorship in 2008, though all comprehensive reform efforts to date have failed to be enacted.

USMI firmly believes that reform is necessary to put our housing finance system on a more sustainable path so that creditworthy borrowers will have access to prudent and affordable mortgage credit in the future and so that taxpayers are better shielded from housing related credit risks. For more than 60 years, private mortgage insurance (MI) has played a critical role in providing access to mortgage credit and protecting taxpayers. The 115th Congress and the Trump Administration have a unique opportunity to address this last unfinished reform to truly put America’s housing finance system on a sustainable path. Recently, there have been a number of reform proposals from think tanks, trade associations, and others—each articulating a specific set of principles or visions for the structure of the new future housing finance system, and elements of the transition to a future state.

This paper, Assessing Proposals to Reform America’s Housing Finance System, seeks to analyze various proposals through the lens of USMI’s housing finance reform principles, with particular attention to the role of private capital to protect against taxpayer risk exposure in the proposed future systems. Several thoughtful legislative proposals for housing finance reform exist, but this paper is restricted to analysis of several of the white papers and reform proposals put forward by think tanks and trade associations. Simply returning to the pre-conservatorship status quo does nothing to strengthen the housing finance system, and USMI looks forward to working with industry and consumer groups, Congress, and the Administration to identify the best reforms to put America’s housing finance system on a sustainable path.

USMI appreciates the work the of authors and stakeholders who assembled these proposals, and we look forward to working with policymakers and other stakeholders to advance necessary reforms to enhance our housing finance system.