As Congress returns from the August recess, regulators closed out the public comment periods for two proposed rules that will substantially impact the housing finance system and borrowers’ access to mortgage credit. Though there has been considerable focus on these important rulemakings over the past several months, policymakers, industry stakeholders, and USMI members remain hard at work supporting the housing finance system as we continue to adapt to and navigate the health and economic consequences of the COVID-19 pandemic. Below are the latest happenings from USMI and key topics we are tracking.

USMI Submits Comments to FHFA on Proposed Enterprise Regulatory Capital Framework (ERCF)

FHFA Director Calabria Testifies Before House Financial Services Committee

USMI Submits Comments to CFPB on General Qualified Mortgage (QM) Definition

Coalition Urges CFPB to Increase the QM Safe Harbor Threshold

ICYMI: USMI Column Published in The Dallas Morning News

USMI Submits Comments to FHFA on Proposed Enterprise Regulatory Capital Framework. On August 31, USMI submitted its comments to the Federal Housing Finance Agency (FHFA) on the re-proposed Enterprise Regulatory Capital Framework (ERCF). In its comments, USMI emphasized the importance of constructing a balanced, transparent, and analytically justified post-conservatorship capital framework for the government sponsored enterprises (GSEs), Fannie Mae and Freddie Mac. USMI President Lindsey Johnson said that “while sufficient levels of capital are important to the sustainable operation of Fannie Mae and Freddie Mac, excessive capital requirements could have a detrimental effect on mortgage availability.” She also added that these excessive capital requirements could, in turn, push mortgage lending outside of the conventional mortgage market.

USMI also called for more transparent and objective treatment of the GSEs’ counterparties, especially private mortgage insurers that already meet a set of rigorous capital and operational requirements known as the Private Mortgage Insurer Eligibility Requirements (PMIERs). In its comment letter, USMI provided the FHFA with detailed analysis to demonstrate that the capital credit for private MI should be increased to be consistent with historical analysis. Similarly, USMI suggested that the proposed rule should encourage, and not discourage, private capital to absorb more risk in front of the GSEs and taxpayers.

A number of other organizations shared similar assessments and recommendations. The Urban Institute said that “the capital requirements on purchase loans should be lower, and more credit should be given to mortgage insurance.” National Taxpayers Union recommended that “[t]he proposed rule should promote, and not disincentivize private capital—including transferring first-loss credit risk through the use of loan level credit enhancement, such as private mortgage [insurance] and through transferring other layers of credit risk through responsible CRT.”

Finally, USMI noted that the revised capital standard is only one element of comprehensive GSE reform, calling on the FHFA to ensure the GSEs are appropriately regulated, maintain their position as market makers, and preserve the bright line separation between the primary and secondary mortgage markets.

USMI’s full comments on the 2020 proposed rule can be found here, an executive summary can be found here, and its comments on the 2018 proposal can be found here.

FHFA Director Calabria Testifies Before House Financial Services. On September 16, FHFA Director Mark Calabria testified before the House Financial Services Committee and provided an overview of the FHFA’s response to the COVID-19 pandemic and the ERCF. A number of members on the Committee focused their comments and questions on the ERCF with Representative Steve Stivers (R-OH) noting in his comments to Director Calabria that in the ERCF “one of the things that doesn’t get credit is MI coverage that’s above the minimum level.” Congressman Stivers and several representatives from both sides of the aisle also shared concerns that the ERCF would negatively impact and inhibit the CRT market. Director Calabria committed to following up with Congressman Stivers to provide additional details on capital credit for greater MI coverage as well as credit for CRT. Additionally, Chairwoman Maxine Waters (D-CA) as well as Representatives Nydia Velazquez (D-NJ), Bill Foster (D-IL), and Alma Adams (D-NC) shared concerns that the capital requirements outlined in the ERCF are excessive and could increase mortgage rates, especially for minority borrowers. Finally, there were a number of questions and comments related to the GSEs’ exit from conservatorship and other reforms that should happen prior to their exit. Representative Ted Budd (R-NC) questioned Director Calabria about the GSEs pilot programs, IMAGIN and EPMI, and asked, “[s]hould a GSE in conservatorship or in any state be permitted to set capital [standards] for counterparties and then compete against them in the primary market?” Director Calabria shared that this is a regulatory issue that was delayed by COVID-19, but that it is an issue the FHFA is committed to resolving.

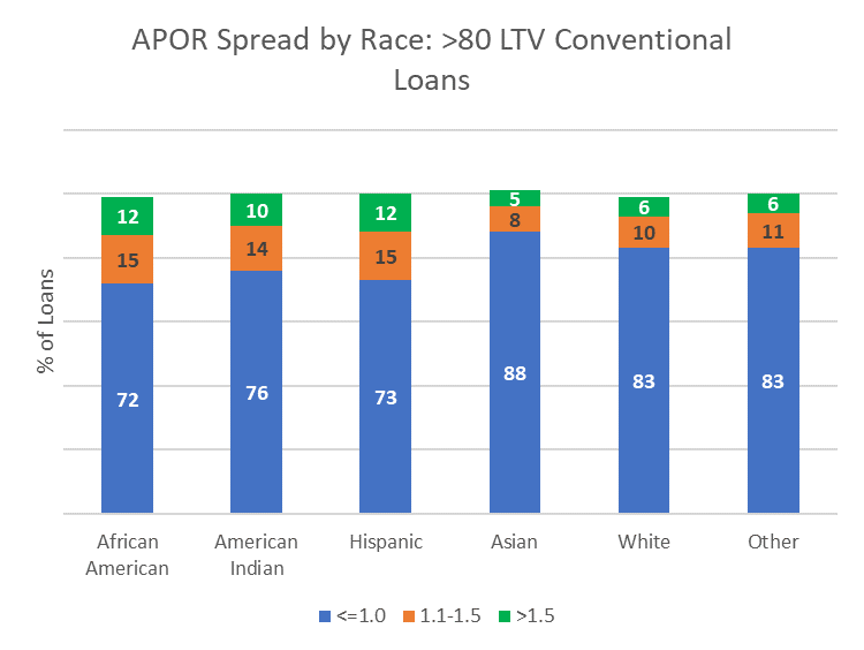

USMI Submits Comments on General Qualified Mortgage Definition. On September 8, USMI submitted comments to the Consumer Financial Protection Bureau (CFPB) for its proposed rule on the General Qualified Mortgage (QM) Definition. USMI urged the Bureau “to strike a proper balance between prudent and transparent underwriting standards, and access to affordable and sustainable mortgage finance credit for home-ready borrowers.” It further noted that the current proposed rule could limit access to the conventional market for traditionally underserved borrowers. In its letter, USMI recommended that the QM Safe Harbor should be set at 200 basis points (bps) above the Average Prime Offer Rate (APOR) to ensure the QM definition does not inadvertently limit access to credit for home-ready borrowers, particularly Black and Hispanic borrowers who are twice as likely to have spreads above the proposed 150 bps Safe Harbor threshold.

USMI also agreed with the Bureau’s assessment that a hard 43 percent debt-to-income (DTI) ratio would be the most harmful option for the General QM definition because it would severely limit access to credit in the conventional market. This assessment was consistent with USMI’s 2019 comment letter in response to the CFPB’s Advance Notice of Proposed Rulemaking (ANPR) on the QM Definition. Also consistent with its 2019 comment letter, USMI suggests a better approach to a General QM definition would be a standard that includes a higher DTI threshold up to 50 percent with specified compensating factors.

USMI also urged the CFPB to allow sufficient time for a smooth transition from the temporary QM category, the “GSE Patch,” to the new General QM definition. In August, USMI submitted comments to the CFPB on the GSE Patch, recommending the Bureau set the sunset date for the GSE Patch to be at least six months after the effective date of the General QM definition final rule. USMI wrote that “this time will be critical given the extensive and still undetermined scope of COVID-19 on the financial services industry as it focuses resources on responding to the economic and health fallout from the pandemic.”

Coalition Urges CFPB to Increase the QM Safe Harbor Threshold. USMI also co-signed a joint industry trade letter with 11 other housing policy and consumer advocate groups calling on the CFPB to increase the QM Safe Harbor threshold from 150 to 200 bps over the current APOR. USMI previously discussed the need for increasing the Safe Harbor threshold to mitigate borrower impact in a blog post. USMI wrote that based on its analysis of “mortgage originations, loan performance, market dynamics, and the need to ensure consumer access to affordable mortgage finance, we recommend that this threshold should be pegged to the same threshold as the QM status, which the NPR suggests should be 200 bps.” Doing so would result in a more level playing field and by changing that threshold, would mitigate the impact on borrowers.

ICYMI: USMI Column Published in The Dallas Morning News. On August 17, USMI published its latest column titled, “The Smarter Way to Buy a Home.” USMI breaks down the 20 percent down payment myth and explains how private mortgage insurance can help home-ready buyers get in their house sooner. USMI also highlights that private mortgage insurance is temporary, unlike other low-down payment options. USMI notes that once the borrower reaches 20 percent equity in their house, private mortgage insurance cancels—which is a significant advantage to borrowers considering a low down payment mortgage. Read the column in The Dallas Moring News.