On June 30, 2020, the Federal Housing Finance Agency (FHFA) published a Notice of Proposed Rulemaking (NPR) on the Enterprise Regulatory Capital Framework (ERCF). On August 31, USMI submitted comments to the NPR, emphasizing the importance of constructing a balanced, transparent, and analytically justified framework. USMI’s full comments can be found here and an executive summary can be found here. In 2018, FHFA issued a prior proposal for changing the risk-based capital framework for the GSEs. USMI also submitted a comment letter, which can be found here.

The Honorable Kathleen Kraninger Director Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20052

Re: Qualified Mortgage Definition Under the Truth in Lending Act (Regulation Z): Extension of Sunset Date, Docket No. CFPB-2020-0021

Dear Director Kraninger:

U.S. Mortgage Insurers (USMI) represents America’s leading providers of private mortgage insurance (MI). Our members are dedicated to a housing finance system backed by private capital that enables access to prudent and sustainable mortgage finance for borrowers while also protecting Fannie Mae and Freddie Mac (the GSEs) and the American taxpayer. The MI industry has more than six decades of expertise in underwriting and actively managing mortgage credit risk, and our member companies are uniquely qualified to provide insights on federal policies concerning underwriting standards for the conventional mortgage market, especially given our experience balancing prudent underwriting with access to affordable mortgage credit.

USMI appreciates the opportunity to comment on the Consumer Financial Protection Bureau’s (Bureau) Notice of Proposed Rulemaking (NPR) regarding the Extension of the Sunset Date for the Temporary GSE Qualified Mortgage (QM) definition. This is an important rulemaking that will work in tandem with the Bureau’s proposed rule to amend the General QM definition and USMI fully supports a smooth transition to a well-calibrated QM definition that promotes prudent underwriting and facilitates access to affordable conventional mortgages for creditworthy consumers. USMI and other housing finance stakeholders recognize that changes to the General QM definition will broadly inform underwriting standards and policies across the mortgage market and will have a significant impact on the number and profile of borrowers served by the conventional mortgage market.

Background

The Bureau’s 2013 Ability-to-Repay/Qualified Mortgage Rule (ATR/QM Rule) created a Temporary GSE QM category for mortgages that: (1) comply with statutory product restrictions, including a points and fees limit; and (2) and are eligible for purchase or guarantee by the GSEs. This QM category became known as the “GSE Patch” and was scheduled to expire the earlier of: (1) the GSEs exiting conservatorship; or (2) or January 10, 2021. The Bureau believed this sunset date would create “an adequate period for economic, market, and regulatory conditions to stabilize” and a “reasonable transition period to the General QM definition.”

For nearly seven years, the GSE Patch has served its intended purpose of maintaining credit availability in the conventional mortgage market. According to data from the Bureau and Federal Housing Finance Agency (FHFA), approximately 957,000 mortgages – or 16 percent of all closed-end first-lien residential mortgage originations – in 2018 fell outside the General QM loan definition but received QM status due to the GSE Patch. These borrowers only had access to financing in the conventional market due to the existence of the GSE Patch.

Expiration of the GSE Patch & Implementation of the New General QM Definition

The NPR would modify the sunset date for the GSE Patch such that its expiration would be the earlier of: (1) the GSEs exiting conservatorship; or (2) the effective date of the General QM final rule. The Bureau has indicated that it “does not intend to issue a final rule amending the General QM loan definition early enough for it to take effect before April 1, 2021” based on the proposed “six-month interval between Federal Register publication of a final rule and the rule’s effective date.”

Recommendation

Consistent with the fact that the GSE Patch was created as a temporary QM category, USMI has strongly supported moving to a QM definition that can be applied consistently throughout the mortgage market. The GSE Patch has played a critical role in maintaining access to mortgage credit and it is paramount that the Bureau provide a smooth transition from its expiration to the new General QM definition. USMI recommends that the Bureau set the sunset date for the GSE Patch to be at least six months after the effective date of the finalized General QM definition rule.

In order to maximize the balance between access to credit, consumer protections, and sustainable homeownership, it is critical that housing industry stakeholders have sufficient time to fully understand and implement a new General QM standard. Depending on the complexity of the finalized revisions to the General QM definition, the significance of the penalties for a violation of the amended ATR/QM Rule, and the large number of mortgage industry participants (lenders, brokers, MIs, warehouse lenders, etc.) that will need to update their operations and systems, USMI recommends a six-month overlap period to mitigate issues associated with implementing a new General QM standard. During the six-month period, mortgage lenders should be permitted to use either the GSE Patch or the new General QM definition, such that a loan meeting either standard would qualify as a QM. This would afford industry participants an appropriate amount of time to develop, test, and implement new models and business operations/processes and facilitate a smooth transition to the new General QM framework. Further, a six-month overlap period would reduce compliance issues that could arise with a singular date that ends the GSE Patch and makes the new General QM definition effective. Specifically, the overlap period would fix the regulatory gap caused by using the mortgage consummation date for the GSE Patch and the loan application date for the proposed General QM definition.

Further, due to the ongoing COVID-19 pandemic, mortgage market participants, consumers, and the economy as a whole are grappling with an unprecedent level of uncertainty. Following the enactment of the “Coronavirus Aid, Relief, and Economic Security Act” (CARES Act), industry is working hard to support homeowners directly and indirectly affected by COVID-19, especially through the implementation of broad nationwide mortgage relief for homeowners with mortgages backed by the GSEs. Due to the extensive scope of the pandemic and the financial services industry’s appropriate focus on responding to the economic and health fallout from COVID-19, USMI believes that a six-month overlap period would promote an orderly implementation period for the new General QM framework while continuing to assist homeowners throughout the country.

***********************

Thank you again for the opportunity to comment on the Extension of the Sunset Date for the GSE Patch and your consideration of our recommendation. USMI and our member companies appreciate the Bureau’s thorough review of this very important issue and we look forward to a continued dialogue as the Bureau proceeds with finalizing and transitioning to a new General QM definition.

Sincerely,

Lindsey D. Johnson President U.S. Mortgage Insurers

The Honorable Kathleen L. Kraninger Director Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20552

Dear Director Kraninger:

The undersigned organizations are writing in response to the Consumer Financial Protection Bureau’s (Bureau) rulemaking regarding the definition of a Qualified Mortgage (QM). Our organizations represent diverse housing finance stakeholders, including consumer groups, lenders, and mortgage insurers, and we appreciate the opportunity to provide our joint perspectives in addition to our individual comment letters that were submitted in response to the Bureau’s Advance Notice of Proposed Rulemaking (ANPR). The Ability-to-Repay (ATR) rule in the Dodd-Frank Wall Street Reform and Consumer Protection Act is one of the most important consumer safeguards in the legislation, and the Bureau’s regulations to promulgate and execute it will directly affect access to safe and affordable mortgage finance credit. We all agree that maintaining access to affordable and sustainable mortgage credit should be a key objective of the Bureau’s revised rulemaking.

We appreciate the Bureau’s thoughtful approach to assessing and implementing potential changes to the QM definition. This letter contains our joint recommendation that the Bureau implement a QM definition that relies on measurable underwriting thresholds and the use of compensating factors for higher risk mortgages rather than either a pricing-based QM definition that uses the spread between the annual percentage rate (APR) and the Average Prime Offer Rate (APOR) as a proxy for underwriting requirements (the “APOR approach”) or a hard cut-off at either 43% or 45% DTI.

Specifically, this coalition strongly supports:

1. The continued use of a modified debt-to-income (DTI) ratio in conjunction with certain compensating factors, which could be used in the underwriting process and would provide guidance to creditors on their use; and

2. Significant changes to Appendix Q to rely on more flexible and dynamic standards for calculating income and debt.

Compensating Factors Would Enable Prudent Underwriting and Affordable Access to Credit

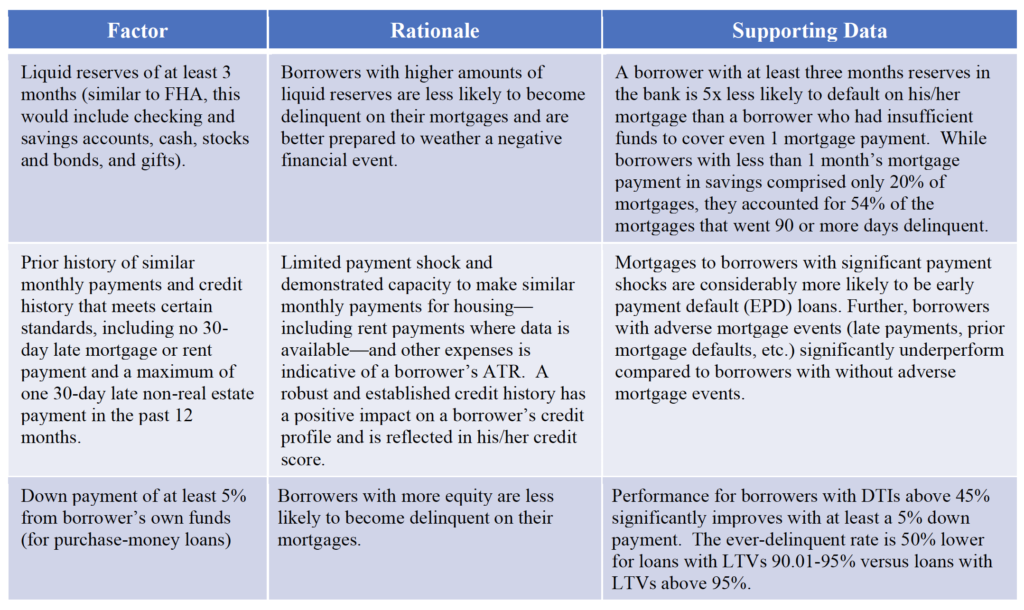

The Bureau should establish a set of transparent mitigating underwriting criteria – “compensating factors” – for mortgages with DTI ratios above 45% and up to 50%. While DTI is not the most predictive factor in assessing a borrower’s ability to repay, it can, in concert with compensating factors, function as a bright line that mitigates undue risk in the conventional market while continuing to provide affordable access to mortgage finance for creditworthy borrowers. Moreover, DTI is a widely and commonly used metric when considering a borrower’s ability to repay in mortgage loan underwriting and is the standard in the current rule issued in 2013. While a higher DTI may indicate increased stress for the borrower and a consequent strain on ability to repay, the presence of other positive credit characteristics – such as liquid reserves, limited payment shock, and/or a down payment from the borrower’s own funds – can mitigate the heightened risk and limit the risk layering that drives loan nonperformance. In fact, the automated underwriting systems (AUSs) used by Fannie Mae and Freddie Mac (the GSEs), as well as proprietary AUSs used by primary market lenders, have always used compensating factors to assess borrowers’ ATR, and such a multifactor approach has long been the standard for manual underwriting throughout the industry.

The efficacy of using compensating factors for high-DTI mortgages is demonstrated by the track record of loans acquired by the GSEs. Rather than introducing undue risk to the housing finance system, these loans have performed well. In fact, high-DTI loans (with ratios between 45.1% and 50%) underwritten using compensating factors outperform loans with lower DTI ratios (between 35.01% and 45%). The lower delinquency rates on the higher DTI loans are almost certainly due to the presence of appropriate compensating factors in the GSEs’ AUSs.

The table below reflects one specific set of compensating factors we believe are appropriate for borrowers with DTIs above 45% and up to 50% that could be tailored for the revised rule. These recommendations are based on: (1) internal analysis and efforts to “back into” the compensating factors currently used by the GSEs to avoid a dramatic shift in the market; and (2) known factors that significantly impact borrowers’ ATR. This is by no means an exhaustive list and we welcome further discussion about compensating factors and their respective predictiveness. The Bureau’s final rule on the QM definition could authorize the GSEs, Federal Housing Finance Agency (FHFA), or an independent standard-setting entity to formulate a transparent list of compensating factors and should make the underlying data and analysis available to the public for ongoing review and assessment to ensure that dynamic compensating factors can be updated to reflect changes in the market and mortgage credit risk environment.

Using an APOR-Only Approach Does Not Meet the Legislative Intent of the Statute and Does Not Appropriately Measure Ability to Repay

The APOR approach is premised on the faulty idea that pricing fully captures credit risk and that, in turn, credit risk is a reasonable marker for ability to repay. In the mortgage industry, a loan’s pricing reflects a number of factors outside of an individual borrower’s credit profile, including a lender’s balance sheet capacity, prepayment speeds, the value of mortgage servicing rights, business goals, and broader economic considerations. With regard to risk, pricing does consider down payment and credit score, but often fails to capture risk-mitigating characteristics such as borrower reserves, DTI ratios, and payment shock.

Any QM definition that relies solely on the statutory ATR requirements or the price of a loan will be seriously flawed. ATR requirements are too broad and do not adequately reflect a borrower’s ability to repay. On the other hand, a loan’s price can be manipulated to gain QM safe-harbor status.

There are several important consumer protection concerns at issue. First, loans made within the QM safe harbor are not, practically speaking, subject to underwriting thresholds/requirements for determining ATR because if a loan meets the product feature requirements along with any other adopted QM standards, no adjudicative body or regulator can “look under the hood” and examine the fuller underwriting process.

Second, if the only underwriting protection is APOR, mortgages could be made to financially vulnerable borrowers at a price just below the safe harbor threshold even though the borrowers’ financial/credit profiles might otherwise call for greater underwriting analysis consideration and ATR protections. This mispricing of risk helped set the 2008 financial crisis in motion.

Third, using this approach assumes creditors are able to uniformly and accurately price risk of repayment, an assumption that was disproven in the financial crisis and ignores market and economic pressures that can drive underpricing of risk.

Fourth, an APOR approach could increase risk within the mortgage finance system as APOR is a trailing indicator of risk and can be procyclical. Therefore, periods of sharply rising rates could cause temporary suspensions in lending that could impact prime loans with higher risk attributes. Additionally, during periods of low rates and loose credit, borrowers run the risk of being overextended.

An APOR Approach Could Make It Harder for Creditworthy Low Down Payment and Minority Borrowers to Obtain Mortgages

Moving from a DTI-based QM standard to an APOR approach could reduce the ability of low down payment and minority borrowers to obtain conventional mortgages. For example, based on 2018 Home Mortgage Disclosure Act (HMDA) data, $11-12 billion in GSE purchase origination volume had loan-to-value (LTV) ratios of >80% and APRs with spreads in excess of APOR + 150 basis points. Further, based on the same dataset, African American and Hispanic borrowers were twice as likely as white borrowers to have mortgages with APRs in excess of the APOR + 150 basis points safe harbor spread.

Many qualified borrowers who are not able to obtain mortgages that meet an APOR standard under a revised QM definition would be denied access to homeownership opportunities while other qualified borrowers in this category would see their loan options reduced. Some mortgages that would normally have been made in the conventional market would gravitate towards the 100% taxpayer-backed FHA, an outcome that is inconsistent with the Administration’s housing finance reform principles and objectives as articulated in the September 2019 reports from the Department of the Treasury and the Department of Housing and Urban Development.

Regardless of the solution chosen, we urge that the transition period from the existing GSE Patch to the new QM framework be sufficiently long to allow market participants adequate time to plan for, and adjust to, new rules and underwriting standards. Any transition to a new QM rule ought to be smooth and well thought-out. Otherwise it risks regulatory uncertainty that might cause mortgage originators to retreat from lending to creditworthy homebuying and refinancing borrowers.

Thank you again for the opportunity to share our collective perspectives on the Bureau’s work regarding the QM definition. The expiration of the GSE Patch and what is developed to replace it will have significant implications for consumers’ access to affordable and sustainable mortgage finance credit. We hope to have a continued constructive dialogue through a robust comment process to result in the best future standard and we welcome the opportunity to serve as resources as the Bureau works toward a proposed, and then final, rule.

Sincerely,

Consumer Federation of America Community Home Lenders Association The Community Mortgage Lenders of America Independent Community Bankers of America National Association of Federally-Insured Credit Unions National Association of REALTORS® National Community Stabilization Trust National Consumer Law Center (on behalf of its low-income clients) U.S. Mortgage Insurers

CC: Andrew Duke Brian Johnson Mark McArdle Kirsten Sutton Thomas Pahl

WASHINGTON — Lindsey Johnson, President of U.S. Mortgage Insurers (USMI), today released the following statement on the organization’s comment letter submitted in response to the Consumer Financial Protection Bureau’s (“the Bureau”) Advance Notice of Proposed Rulemaking on the “Qualified Mortgage (QM) Definition under the Truth in Lending Act (Regulation Z).”

“As takers of first-loss mortgage credit risk with more than six decades of expertise and experience underwriting and actively managing that risk, USMI members understand the need to balance prudent underwriting with a clear and transparent standard that maintains access to affordable and sustainable mortgage finance credit for home-ready borrowers. The upcoming expiration of the temporary QM category, often referred to as the ‘GSE Patch,’ provides an important opportunity for the Bureau to assess what has developed within the marketplace since the enactment of the QM Rule. Notably, mortgage lending has been done with far greater diligence by market participants to ensure consumers have a reasonable ability-to-repay (ATR) and has resulted in a much stronger housing finance system. Further, the GSE Patch has played a critical role in maintaining credit availability. In our comments to the Bureau, we offer specific recommendations for replacing the current GSE Patch to establish a single transparent and consistent QM definition in a way to balance access to mortgage finance credit and proper underwriting guardrails to ensure consumers’ ATR. USMI’s recommendations include:

Maintaining the ATR and product restrictions as part of any updates to the QM definition to ensure discipline in the lending community and to protect consumers;

Retaining specific underwriting guardrails such as the current debt-to-income (DTI) component of the QM definition, but modifying the specific threshold to better serve consumers; and

Developing a single set of transparent compensating factors for loans with DTIs above 45 and up to 50 percent for defining QM across all markets, similar to how the GSEs, FHA, and VA use compensating factors in their respective markets today.

“Retaining specific thresholds in measuring a consumer’s income, assets, and financial obligations better serves consumers and ensures that the statutory and regulatory intent of measuring a consumer’s ATR is met. Further, adjusting the current DTI limit from 43 percent to 45 percent for all loans, and up to 50 percent for loans with accompanying compensating factors creates a more transparent and level playing field that provides greater certainty for borrowers and lenders and reduces the impact of the expiration of the GSE Patch. USMI believes that the development of a single transparent industry standard will facilitate greater consistency across all lending channels and ensure there is not market arbitrage to achieve QM status.

“USMI applauds the Bureau for undertaking the necessary process for updating this critical rule that is aimed at enhancing lending standards and consumer protection. We look forward to working with the Bureau as it seeks to implement any changes to this important rule.”

Following the release of the Bureau’s ANPR in July, USMI published a blog with observations and recommendations for replacing the GSE Patch.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

Luisa De Gaetano Polverosi Associate Managing Director Moody’s Investor Service 7 World Trade Center 250 Greenwich Street New York, NY 10007

Dear Ms. De Gaetano Polverosi:

U.S. Mortgage Insurers (USMI) welcomes the opportunity to provide comments on the “Proposed Update to Moody’s Approach to Rating US Prime RMBS”. Our members are supportive of the proposed update to Moody’s methodology, and view this update as a necessary step toward examining and updating various models, and also as a step toward prudently revitalizing the private securitization market for Residential Mortgage-Backed Securities (RMBS). We applaud the recognition that the value of private mortgage insurance (MI) extends beyond the government-sponsored enterprise (GSE) segment of the housing finance system and we believe that RMBS investors can greatly benefit from the loss severity reduction resulting from MI.

Of particular interest to our members is the proposed update to the evaluation of private MI. Lenders originating mortgages with loan-to-value (LTV) ratios above 80% typically obtain MI to maintain maximum flexibility for secondary market execution. Currently, however, the lack of credit for MI in the rating determination provides little incentive for these mortgages to be included in RMBS structures and transactions. The proposed changes to the methodology address this issue and lenders will no longer be disincentivized to direct mortgages with LTVs above 80% to the RMBS market, thus increasing access to liquidity in support of homeownership and offering investors more choices with regard to taking credit risk in this vital segment of the mortgage market.

Our members appreciate that the proposed update to Moody’s methodology has been the result of an investment of considerable time and effort in data analysis, as well as careful attention to the development of the mortgage lending landscape. While the proposal as published is an improvement, in the spirit of mutually beneficial ongoing dialogue, we would like to offer some commentary on the proposed methodology. Generally speaking, we feel that additional transparency, particularly more details around the benefits of MI, the proposed changes to rejection rates, and Moody’s methodology of determining maximum insurance payout and allocation based on the insurer’s rating, would be highly beneficial to market participants and enable more detailed analysis of the proposal, in addition to some minor recommended adjustments.

Rejection Rate Assumptions

Looking at the proposed rejection rates, a more detailed representation of the slope and/or shape of the line between the Baseline Assumption and Aaa Assumption would be useful, as well as more details surrounding the Aaa Assumption’s rejection rate range of 5-15% in the absence of a GSE backstop. In additional, the variability of the Aaa Assumption should include disclosures of all the factors that can drive a final determination.

We would also encourage the rejection rate assumptions to reflect MIs’ updated Master Policies which increased clarity on terms and streamlined the payment of claims to ensure that MI coverage results in timely, consistent, and accurate policy and claim administration. The proposed update’s rejection rate assumptions should account for the imbedded Rescission Relief (contractual circumstances under which an MI waives it rights to rescind coverage on a mortgage) applicable to the loans in a specific transaction. Mortgages that are already subject to Rescission Relief should have lower assumed rejection rates, and the various milestones regarding Rescission Relief should also be considered in the overall lifetime projections. Our member companies are more than willing to provide detailed information on Rescission Relief to Moody’s to assist with the refinement of implementation of the rejection rate assumptions.

Further, the proposed update to the rating methodology should reflect overall improvements in mortgage originators’ underwriting standards, as well as the MI industry’s new capital framework that is driven by the GSEs’ Private Mortgage Insurer Eligibility Requirements (PMIERs). All MI companies comply with PMIERs’ stringent capital and operational requirements and the industry has nearly doubled its pre-crisis capital, an indication of the industry’s strength and that MI on loans included in securitizations should improve credit enhancement levels in rated RMBS transactions.

The rejection rate haircut should also reflect the Representations & Warranties of a particular transaction and encourage stronger language by providing a benefit to RMBS issuers that provide investors with an extra layer of protection. There have been significant improvements to lenders’ underwriting practices, including the use of independent validation sources, over the last several years that would serve to reduce the overall rejection rates and improve credit enhancement levels, and should therefore be considered for loans that will be repurchased due to loan manufacturing defects or where the trust will be made whole due to servicing defects. Lastly, with regards to the differential treatment of the GSE backstop, USMI encourages Moody’s to consider broadening that category to create a level playing field by including additional types of credit enhancement backstops from a variety of counterparties that would supplement private MI’s credit risk protection.

Maximum Insurance Payout and Allocation

The proposed update includes analysis of expected losses but currently lacks visibility into the benefit of MI as it relates to the Moody’s Individual Loan Analysis credit enhancement (MILAN CE) framework. We would like to request that Moody’s disclose detailed methodology regarding treatment of MI in the MILAN framework. In practice, it is critical that a RMBS issuer be able to quantify the benefit of MI with a certain insurer rating in each of the rating scenarios. Therefore, we believe the RMBS market will greatly benefit from Moody’s publishing the Idealized Expected Loss Table which demonstrates the conversion from non-rejected insured losses to idealized losses in correspondence to the insurance rating of MI in each loss scenario. Without seeing the Idealized Expected Loss Table, it is difficult to comment on this specific component of the proposed methodology update, but there are a couple of general comments related to this element of the rating methodology we would like to offer.

The first is that since the rating of private MIs depends on many factors beyond their capital adequacy, it is possible that purely using an overall company rating may be overly conservative. For examples, ratings of private MIs may not fully reflect the benefit of credit risk transfer programs the MI industry executes with global capital markets and reinsurers, which have transformed the MI business model from “buy-and-hold” to “buy-manage-distribute” and significantly strengthen MIs’ capital positions and claims paying ability during stress periods. While the insurer rating may be reflective as an overall measure of counterparty risk, the incorporation of non-claims payment factors means that items not related to the ability to pay all claims are taken into consideration. It would be very helpful to have access to MI rating sensitivity analysis, as well as loss scenarios that inform the proposed methodology updates.

The second comment is that we would like to understand how the maximum insurance payout (MIP) plateaus and how the state-based insurance regulatory framework has been reflected. Of the private MI companies that ceased writing new business during the financial crisis approximately a decade ago, their cash payouts currently range from approximately 75% to 100%, with the remainder being deferred payment obligations (DPO) – facts that support very high MIP assumptions.

Conclusion

Thank you again for the opportunity to comment on the “Proposed Update to Moody’s Approach to Rating US Prime RMBS.” Our members appreciate the data-driven analysis and proposed update, and look forward to continuing a mutually beneficial dialogue, including on the topic of recognition of the value of private MI. This important shift can help promote new interest in private label RMBS, as lenders will have increased secondary market execution flexibility when it comes to their insured mortgage production. By providing an avenue for mortgages with private MI to contribute to the supply of collateral for RMBS, we will see improved liquidity for lenders and an expansion of mortgage credit investment opportunities for private capital investors.

Questions or requests for additional information may be directed to Lindsey Johnson, President of USMI, at ljohnson@usmi.org or 202-280-1820.

Sincerely,

Lindsey D. Johnson President U.S. Mortgage Insurers

Alfred M. Pollard General Counsel Federal Housing Finance Agency Eighth Floor 400 Seventh Street, SW Washington, D.C. 20219

RE: Comments/RIN 2590-AA95

Dear Mr. Pollard:

This letter is submitted by U.S. Mortgage Insurers (USMI), a trade association comprised of the leading private mortgage insurance (MI) companies in the United States.0F1 Together, the private mortgage insurance industry has helped nearly 30 million homeowners over the past 60 years, including more than 1 million in the past year alone.

USMI is dedicated to a housing finance system backed by private capital that enables access to housing finance for all creditworthy borrowers while protecting taxpayers. USMI supports meaningful and appropriate capital requirements for Fannie Mae and Freddie Mac (the “Enterprises”) and appreciates the Federal Housing Finance Agency (FHFA) for initiating this rulemaking process, and for affording us an opportunity to submit comments.

Currently, the Enterprises use a FHFA-developed Conservatorship Capital Framework (CCF) to align business and pricing decisions (e.g. G-Fees) with economic risk. The notice of proposed rulemaking (NPR) states that during conservatorship, FHFA expects the Enterprises to “use assumptions about capital described in the rule’s risk-based capital requirements in making pricing and other business decisions,” even though the new standards will not be used to determine capital compliance until after the conservatorship ends.1F2 Therefore, the final regulation could have an immediate real-world impact on the Enterprises’ activities and the cost and availability of mortgage credit. As a result, this rulemaking is very significant for our members, other participants in housing finance, and the American public.

The Honorable Mitch McConnell Majority Leader United States Senate S-230, U.S. Capitol Washington, DC, 20510

The Honorable Chuck Schumer Minority Leader United States Senate S-221, U.S. Capitol Washington, DC 20510

Dear Majority Leader McConnell and Leader Schumer:

The undersigned organizations, representing a wide range of perspectives in the housing and mortgage finance industry, write to strongly encourage the confirmation of Dr. Mark Calabria as Director of the Federal Housing Finance Agency (FHFA).

A longtime public servant, Dr. Calabria is a respected expert in housing finance with detailed knowledge of the intricacies of the housing and mortgage finance markets. As one of the Congressional staffers who helped craft the Housing and Economic Recovery Act of 2008, Dr. Calabria has demonstrated a keen understanding of the critical role of the FHFA as both regulator and conservator of Fannie Mae and Freddie Mac (the “Enterprises”). Additionally, through his experience as a staffer on the U.S. Senate Committee on Banking, Housing, and Urban Affairs, and at the National Association of REALTORS®, National Association of Home Builders, and the U.S. Department of Housing and Urban Development, Dr. Calabria understands the need for FHFA to be transparent and methodical in its development and enforcement of policies.

The FHFA has an incredibly important mission of ensuring for a liquid and robust mortgage market, while regulating the Enterprises and their $5.4 trillion in mortgage credit risk, along with the Federal Home Loan Bank system.1 It is critical for the Senate to proceed expeditiously to confirm a permanent Director at the FHFA in order to best promote an efficient national secondary mortgage market that facilitates access to affordable mortgage financing for all creditworthy borrowers during all market conditions. Dr. Calabria recognizes the need to balance this mission with the protection of taxpayers from mortgage credit risk while avoiding market disruptions when improving and implementing policy. Any new Director should also maintain increased transparency with essential public feedback to guarantee that any potential changes are in the best interests of consumers, the supporting industries, and the overall economy.

Dr. Calabria has a deep understanding of the secondary mortgage market and the complex policy issues that affect the entities the FHFA oversees. Dr. Calabria’s decades of experience in the public and private sectors have prepared him to execute the duties of Director and address the agency’s mission and significant regulatory priorities.

We respectfully request the swift confirmation of Dr. Calabria as Director of the FHFA to protect and ensure the continuation of a strong real estate market and overall economy.

Sincerely,

American Academy of Housing and Communities American Land Title Association (ALTA) The Commercial Real Estate Finance Council (CREFC) Community Associations Institute Consumer Mortgage Coalition Leading Builders of America Make Room Manufactured Housing Association for Regulatory Reform (MHARR) Manufactured Housing Institute Mortgage Bankers Association Nareit National Affordable Housing Management Association The National Apartment Association National Association of Home Builders The National Association of Housing Cooperatives National Association of REALTORS® National Council of State Housing Agencies National Leased Housing Association National Multifamily Housing Council The Real Estate Roundtable Real Estate Services Providers Council, Inc. (RESPRO) The Realty Alliance U.S. Mortgage Insurers

USMI joined nearly 60 other organizations in supporting a full Senate vote on the nomination of Pam Patenaude as HUD Deputy Secretary. Click below to read the full coalition letter. Click here to download the letter as a PDF.

On July 31st, USMI submitted the following response to the request for comment regarding the Consumer Financial Protection Bureau’s notice of assessment of the Ability-to-Repay/Qualified Mortgage rule. USMI applauds the Bureau for undertaking an assessment of this critical rule that is aimed at enhancing lending standards and consumer protection, now that sufficient time has passed since it went into effect. As described in the letter, USMI encourages the Bureau to assess whether different QM standards across the various regulatory agencies have negatively impacted consumers. Click here to read the full letter.

USMI delivered the following letter to members of the Senate Banking Committee last night:

May 20, 2015

The Honorable Richard Shelby

Chairman

U.S. Senate Committee on Banking, Housing, and Urban Affairs

534 Dirksen Senate Office Building

Washington, DC 20510

Dear Chairman Shelby:

U.S. Mortgage Insurers (“USMI”) welcomes the effort to make progress on increasing the reliance on private capital in housing finance as part of consideration by the Senate Banking Committee of the Financial Regulatory Improvement Act of 2015.

Specifically, USMI supports Section 706, which calls on the Government Sponsored Enterprises (“GSEs”) to engage in front-end risk sharing transactions. This directive would make greater use of private capital to “de-risk” the GSEs, lower the exposure and costs for the enterprises and taxpayers and should lower costs to borrowers. USMI supports this effort, and will continue to work with the Committee during the legislative process on clarifications to ensure the legislation has the intended effect of being “transaction neutral” to permit a variety of methods of up front risk sharing, with all risk sharing counterparties held to equivalent standards.

Promotion of greater up front risk sharing will help build a strong, stable housing finance system that provides access to sustainable and affordable mortgage credit while protecting taxpayers. We look forward to favorable action on this important effort.

USMI Supports Affordable Housing Principles and Calls for Transparency in FHFA Duty to Serve Plans

USMI submitted comments on the Federal Housing Finance Agency’s (FHFA’s) proposal for how the government sponsored housing enterprises Fannie Mae and Freddie Mac should serve underserved markets. USMI supports both principles of facilitating the financing of affordable housing for low-to-moderate income families consistent with the Enterprises’ overall public purposes while maintaining a strong financial condition and reasonable economic return. To that end, among other things USMI calls for full transparency into the economics of the Plans to ensure policy aims are met in the most efficient way available. USMI looks forward to working with MI customers, FHFA, the Enterprises, and other market stakeholders to help the Enterprises meet their “Duty to Serve” obligations. The text of the USMI comment letter can be found here.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

In letters to House and Senate Budget Committee leadership, USMI joined a broad group of more than a dozen housing organizations urging Congress to use GSE G-fees for their intended purpose, to support homeownership stability.

“By preventing g-fees to be used as a funding offset, this budget point of order gives lawmakers a vital tool to prevent homeowners from footing the bill for unrelated spending,” the letters said. “We urge you to once again include it in this year’s Budget Resolution.”

Click here for the full text of the House and Senate letters.