USMI joined a coalition of housing finance organizations including the Mortgage Bankers Association, National Association of Home Builders, National Association of REALTORS®, and National Housing Conference, in sending a letter to U.S. House of Representatives Committee on Ways and Means Chairman Richard Neil. The undersigned organizations urged the committee to modify current law to make the mortgage insurance premium tax deduction permanent and to eliminate its income phaseout. As a diverse coalition of stakeholders in the housing finance system, they affirmed that the current AGI phaseout represents a burdensome eligibility criterion for American families to claim the mortgage insurance deduction and that millions more homeowners would benefit from a permanent extension that eliminates the AGI phaseout. Click here to read the letter.

Author: dcadmin

Newsletter: July 2021

As the August recess approaches, there have been several notable developments in the housing finance industry. Policymakers and industry leaders continue to focus on top priorities including new homeowner protections, the bipartisan infrastructure deal, housing affordability and supply, and down payment assistance (DPA), among others. Further, during the past month, U.S. Mortgage Insurers (USMI) released its latest Member Spotlight highlighting a Q&A with Enact’s President and CEO, Rohit Gupta; a statement congratulating Julia Gordon on her nomination to serve as Federal Housing Administration (FHA) Commissioner; and published two blog posts noting and discussing the top findings from USMI’s 2021 National Homeownership Market Survey. Below are some of the key developments USMI has been following over the last month.

Bipartisan Infrastructure Deal

USMI’s 2021 National Homeownership Market Survey

USMI Member Spotlight: Enact CEO Rohit Gupta Talks About First-Time Homebuyers

USMI Joins Coalition Letter to Infrastructure Bipartisan Senate Group on Usage of G-Fees

USMI’s Statement on Julia Gordon’s Nomination as FHA Commissioner

Biden Administration Announces New Homeowner Protections

FHFA Dropping Fee Introduced During COVID-19

House Financial Services Committee Holds Hearing with HUD Secretary Marcia Fudge

What We’re Reading: Congressional Proposals to Increase Homeownership

Bipartisan Infrastructure Deal. On July 28, the $1.2 trillion infrastructure deal cleared a major procedural vote in the Senate. The 67-32 vote passed with support from all 50 Democrats and 17 Republicans. This vote allows the Senate to start the debate and amendment process to resolve outstanding issues. Draft legislative text of the bill circulated on Thursday; however, the bill’s authors noted today that the text has not yet been finalized. According to the draft text, the bill would provide about $550 billion in new federal money for roads, bridges, and other physical infrastructure programs. While agreement on final text and clearing final votes in the House and Senate remain, if passed, the bill would mean the largest infusion of federal money into public works in more than a decade.

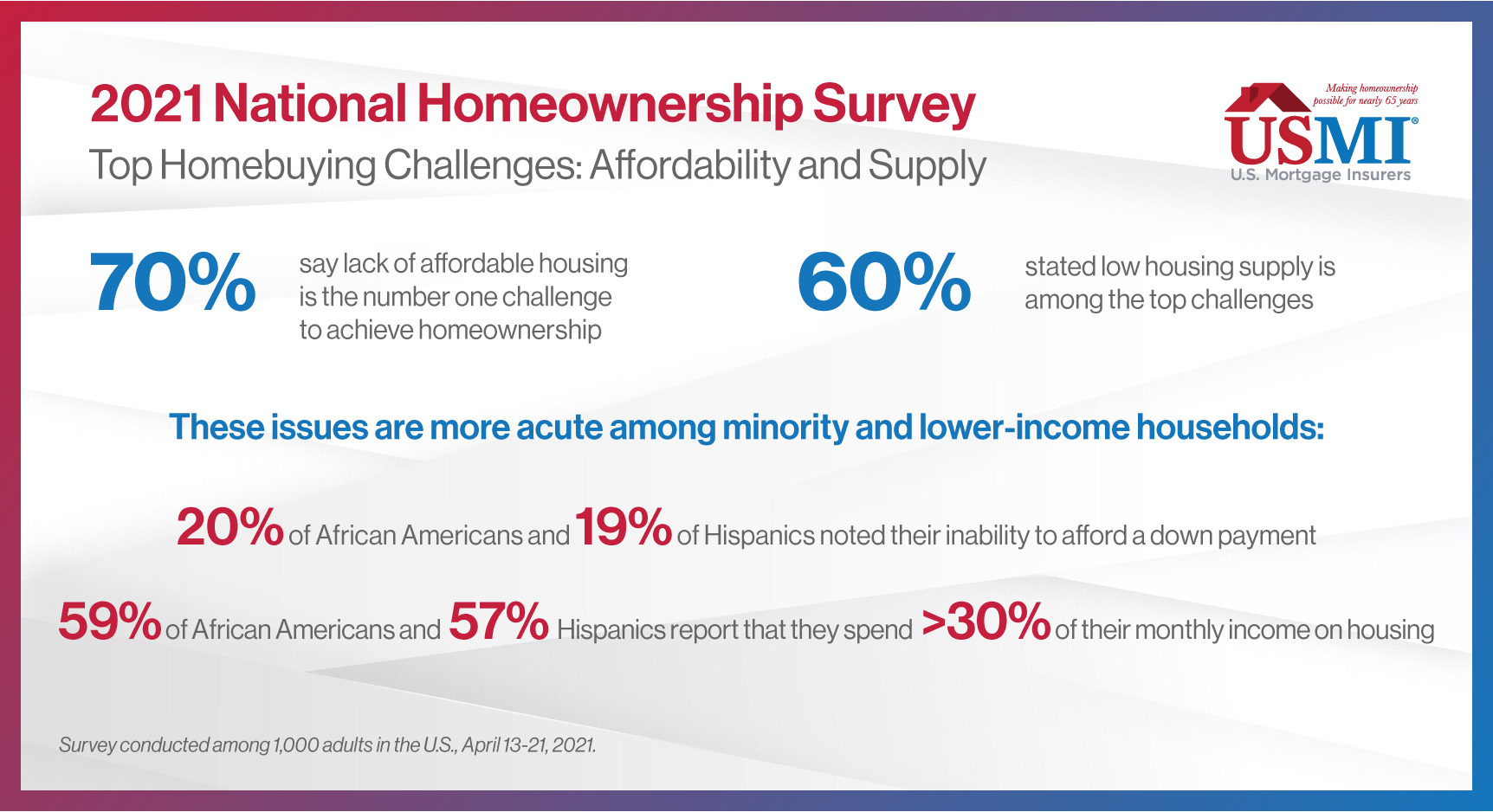

USMI’s 2021 National Homeownership Market Survey. Following the June release of USMI’s 2021 National Homeownership Market Survey, fielded by ClearPath Strategies to 1,000 adults in the U.S., USMI published two blog posts titled, “National Homeownership Market Survey: Key Takeaways,” and “Top Homebuying Challenges: Affordability and Supply.” In these posts, USMI highlights that more than 7 in 10 respondents view owning a home as important for stability and financial security. In addition, nearly 7 in 10 respondents ranked the lack of affordable housing as the number one housing challenge, while nearly 6 in 10 stated that low housing supply is another top issue, all of which become more acute among minority and lower income homebuyers. The latest blog notes that just this week, “the Federal Housing Finance Agency (FHFA) released its Home Price Index and reported that home prices were up 1.7 percent in May, and up an astonishing 18 percent year over year. This significant home price appreciation is largely driven by the lack of housing supply in today’s market and is impacting borrowers’ access to homeownership across the country.”

USMI Member Spotlight: Enact CEO Rohit Gupta Talks About First-Time Homebuyers. Earlier this month, USMI talked with Rohit Gupta, President and CEO of Enact, formerly Genworth Mortgage Insurance (MI), about the company’s new brand as well as how it is better positioned to serve low down payment borrowers and the first-time homebuyer market. Gupta said that private MI “is imperative in order for borrowers with low down payments to have access to home mortgage financing options,” and noted that Enact’s First-Time Homebuyer Market Report shows how the housing finance system continues to perform well with the private MI industry ensuring access to credit for first-time homebuyers.

USMI Joins Coalition Letter to Bipartisan Senate Infrastructure Group on Usage of G-Fees. Last week,USMI joined a coalition of housing finance organizations, including Mortgage Bankers Association (MBA), National Association of REALTORS®, and National Housing Conference, in sending a letter to the bipartisan Senate group negotiating infrastructure legislation. In this letter, the coalition requested that lawmakers refrain from utilizing guarantee fees (g-fees) charged by the government sponsored enterprises (GSEs), Fannie Mae and Freddie Mac, as a source of funding offsets. G-fees are charged by the GSEs and intended to cover the credit risk and other costs that the GSEs incur when they acquire single-family loans from lenders, and the consumer ultimately pays for these fees in their mortgage costs. It is important that future homeowners not be saddled with additional cost burdens, especially those from spending that is not housing-related. As representatives of institutions that span the entire housing finance ecosystem, the coalition reaffirmed the belief that g-fees should only be used as originally intended: “a critical risk management tool to protect against potential mortgage credit losses and to support the GSEs’ charter duties.”

USMI Statement on Julia Gordon’s Nomination as FHA Commissioner. On June 28, USMI released a statement on President Biden’s nomination of Julia Gordon to serve as FHA Commissioner. Gordon has broad experience in the housing finance system, specializing in supporting affordable homeownership and promoting consumer protection policies for underserved markets. USMI President Lindsey Johnson said, “[w]e look forward to working closely with Gordon in seeking to promote a complementary, collaborative, and consistent housing finance system that enables sustainable homeownership for American families while also protecting taxpayers.”

Biden Administration Announces New Homeowner Protections. Last week, the Biden Administration unveiled additional actions to prevent foreclosures, offering loan modifications and payment reductions for homeowners with government-backed mortgages to help them stay in their homes, as the federal ban on foreclosures is set to end on July 31. The Biden Administration said about 1.8 million Americans remain in forbearance today, more than a year after emergency safeguards were put in place due to the COVID-19 crisis. The new loan modification programs for mortgages backed by the FHA, Department of Agriculture (USDA), and Department of Veterans Affairs will “aim to provide homeowners with a roughly 25 percent reduction in borrowers’ monthly principal and interest (P&I) payments to ensure they can afford to remain in their homes and build equity long-term.”

Additionally, on Thursday, the White House called on Congress to extend the eviction moratorium and announced that President Biden has “asked the U.S. Departments of Housing and Urban Development, Agriculture, and Veterans Affairs to extend their respective eviction moratoria through the end of September, which will provide continued protection for households living in federally-insured, single-family properties.” Today, FHA announced an extension of its single family eviction moratorium through September 30, and FHFA announced that it will be extending its COVID-19 real estate owned (REO) Eviction Moratorium through September 30, 2021. The REO eviction moratorium applies to properties that have been acquired by an Enterprise through foreclosure or deed-in-lieu of foreclosure transactions. The current moratorium was set to expire on July 31, 2021.

Lastly, late Thursday evening, U.S. House Financial Services Committee (HFSC) Chairwoman Maxine Waters (D-CA) and 100 Democratic cosponsors introduced H.R. 4791, the “Protecting Renters from Evictions Act of 2021,” which would extend the moratorium on residential evictions through December 31, 2021.

FHFA Dropping Fee Introduced During COVID-19. On July 16, the FHFA announced that the GSEs will eliminate the Adverse Market Refinance Fee for loan deliveries effective August 1, 2021. At the direction of FHFA, the GSEs implemented a 50-basis point refinance fee for mortgages at or above $125,000 to cover potential losses due to the COVID-19 pandemic. The fee took effect December 1, 2020 and, according to the MBA, added approximately $1,400 to the cost of refinancing most mortgages. “The COVID-19 pandemic financially exacerbated America’s affordable housing crisis,” said FHFA Acting Director Sandra L. Thompson, adding, “[e]liminating the Adverse Market Refinance Fee will help families take advantage of the low-rate environment to save more money.”

House Financial Services Committee Holds Hearing with HUD Secretary Marcia Fudge. On July 20, the HSFC held a hearing titled, “Building Back A Better, More Equitable Housing Infrastructure for America: Oversight of the Department of Housing and Urban Development,” (HUD) in which Secretary Marcia Fudge participated as a witness. During the hearing, legislators demonstrated bipartisan agreement on housing affordability becoming a growing challenge. Secretary Fudge indicated in her opening remarks that housing affordability “keeps families awake at night,” and said that housing is “the number one crisis in this country today.” Committee members discussed several facets of the issue and a variety of approaches to address it, particularly in support of first-time homebuyers finding themselves priced out of a competitive market. Representatives Blaine Luetkemeyer (R-MO) and Ted Budd (R-NC) inquired about HUD’s potential tools to combat the impacts of regulations on housing costs. Secretary Fudge conveyed that HUD is exploring tools at the federal level to incentivize localities to update their zoning policies and remove other statutory barriers to affordable housing. Representative Ted Budd (R-NC) asked Secretary Fudge about how the $213 billion in funding proposed in President Biden’s infrastructure plan for new and rehabilitation of existing affordable housing would be divided. Fudge noted that dollar amounts had not been decided but the administration is targeting the development of 2 million new units and rehabilitation of 500,000 existing units. Other topics discussed included accessibility and affordability of FHA credit, GSE lending to minority borrowers, HUD appraisal task force, climate risks, and Property Assessed Clean Energy (PACE) loans.

What We’re Reading: Congressional Proposals to Increase Homeownership. On July 19, USMI published a blog post titled, “Washington Focuses on Infrastructure and Equity with an Eye Toward Homeownership.” The blog notes that as policymakers shift their focus from the COVID-19 pandemic to negotiating and drafting legislative text for President Biden’s infrastructure proposals, Congressional Democrats are championing housing policies intended to promote equitable communities and give traditionally underserved Americans a stake in those communities. In this sense, the piece outlines and details the various legislative proposals put forth by Democratic legislators to help these underserved communities. Many of these proposals seek to address issues such as the critical housing supply shortage, first-time/first-generation DPA proposals, tax incentives to support homeownership, and home equity building opportunities.

USMI released principles for Access and Affordability in January, in which it suggests that “existing DPA programs— and any expansions – should balance responsible underwriting that promotes sustainable homeownership and access to affordable low down payment mortgages. DPA programs should be targeted to serve the creditworthy borrowers who are unable to attain even a 3 [percent] or 3.5 [percent] down payment. It is important that DPA programs are structured and operated in a sustainable manner so as to not create excessive leverage and risk within the mortgage finance system, or pose undue risk to taxpayers and the economy, which will ultimately hurt vulnerable homeowners most.” Further, USMI encouraged policymakers, including HUD Secretary Marcia Fudge, to pursue policies that promote affordable and sustainable access to mortgage finance credit, but that do not add fuel to the fire in terms of artificially lowering what is already relatively affordable mortgage finance credit as such actions would inject more “demand” into the market without addressing the “supply” side—which will only drive-up home prices further, hurting affordability at the lower end of the market most.

Blog: Affordability and Supply Among Top Homebuying Challenges

The lack of affordable housing continues to be a focal point for the mortgage finance community as low- to-moderate income (LMI) and first-time homebuyers continue to report challenges in buying starter homes. In fact, today, the Federal Housing Finance Agency (FHFA) released its Home Price Index and reported that home prices were up 1.7 percent in May, and up an astonishing 18 percent year over year. This significant home price appreciation is largely driven by the lack of housing supply in today’s market and is impacting borrowers’ access to homeownership across the country. Therefore, it is no surprise this topic has become an elevated policy concern, as the “underbuilt” gap has dramatically increased over the last decade, and between 2018 and 2020, the housing stock deficit increased by more than 50 percent according to a recent Freddie Mac report.

The National Association of REALTORS® (NAR) recently released a report that highlights the dire housing supply situation our nation currently faces. “The state of America’s housing stock […] is dire, with a chronic shortage of affordable and available homes [needed to support] the nation’s population,” and adds that “[a] severe lack of new construction and prolonged underinvestment [have led] to an acute shortage of available housing […] to the detriment of the health of the public and the economy.” In addition to finding an underbuilt gap of 5.5 to 6.8 million housing units since 2001, the report notes that unbuilt single-family homes account for 2 million of those units. This shortage of available and affordable homes, coupled with a robust demand, is fueling the rise of housing prices for potential homebuyers, putting the goal of homeownership further out of reach. NAR’s Chief Economist Lawrence Yun stated in the report, “[t]here is a strong desire for homeownership across this country, but the lack of supply is preventing too many Americans from achieving that dream.” In late June, USMI released its 2021 National Homeownership Market Survey, fielded by ClearPath Strategies among 1,000 U.S. adults in the general population, which found that Americans understand the importance of owning a home: more than 7 in 10 respondents see this as important for stability and financial security.

USMI, in representing a sector of the industry that is dedicated to facilitating affordable low down payment lending and promoting sustainable homeownership, explored this topic in our recent survey, which found that lack of affordable housing and low supply of housing ranked among the top homebuying challenges. In fact, nearly 7 in 10 respondents ranked the lack of affordable housing as the number one housing challenge and nearly 6 in 10 stated that low housing supply is another top issue. These issues were more acute among minority and lower income homebuyers as 20 percent of African American and 19 percent of Hispanic respondents note their inability to afford a down payment. Further, more than half of African Americans (59 percent) and Hispanics (57 percent) reported spending over 30 percent of their monthly income on housing, the threshold for a household to be considered “housing-cost burdened.” The complete findings from USMI’s national survey are available here.

These challenges are front and center of the nation’s housing agencies, FHFA and the Federal Housing Administration (FHA). Last month, President Biden appointed Sandra L. Thompson as FHFA’s Acting Director, having previously served as the Deputy Director of the Division of Housing Mission and Goals since 2013. In her accepting remarks, Thompson stated that “[t]here is a widespread lack of affordable housing and access to credit, especially in communities of color,” adding that “[i]t is FHFA’s duty through our regulated entities to ensure that all Americans have equal access to safe, decent, and affordable housing.” President Biden also recently nominated Julia Gordon to be the Assistant Secretary for Housing and FHA Commissioner.

USMI continues to urge policymakers and the housing finance industry to focus on addressing this historic shortage of affordable homes to help balance housing prices and ensure access to homeownership. In a letter directed to the Department of Housing and Urban Development (HUD) Secretary Marcia Fudge, USMI urged HUD to avoid policies that would stoke more demand in the marketplace without addressing the supply issues, as not doing so will only worsen the affordability challenges. And while addressing supply and the shortage of affordable homes is imperative, policymakers must also not lose sight of addressing the issues that unnecessarily increase costs or create barriers for minority and lower income homebuyers. Importantly, expanding homeownership opportunities for these borrowers does not have to be at the expense of reforms made over the last decade that have strengthened the system to reduce risk, protect borrowers, and avoid another housing market collapse.

We appreciate that policymakers recognize the role of low down payment mortgage options in facilitating homeownership. USMI’s survey found that consumers view mortgage insurance (MI) as an important piece of the homeownership puzzle, specifically because MI levels the playing field by helping LMI and first-time buyers access home financing. In fact, 73 percent of all respondents view MI as needed and positive to obtaining homeownership, and nearly 70 percent of respondents citing that it is important to have access to these low down payment loans through both the conventional market backed by private MI and government-backed loans through FHA.

Letter: Infrastructure Bipartisan Senate Group on Usage of G-Fees

USMI joined a coalition of other housing finance organizations, including National Association of REALTORS® and National Housing Conference, in sending a letter to the bipartisan Senate group negotiating infrastructure framework. In this letter, the coalition requested that lawmakers refrain from utilizing Fannie Mae and Freddie Mac (the government sponsored enterprises or “GSEs”) guarantee fees (“g-fees”) as a source of funding offsets. As representatives of institutions that span the entire housing finance ecosystem, the coalition reaffirmed the belief that g-fees should only be used as originally intended: as a critical risk management tool to protect against potential mortgage credit losses and to support the GSEs’ charter duties. Read the full letter here.

Member Spotlight: Q&A with Rohit Gupta of Enact

USMI’s member spotlight series focuses on how the private mortgage insurance (MI) industry works to address several critical issues within the housing finance system, including expanding access to affordable mortgage credit for first-time and minority homebuyers, protecting taxpayers from risk in the mortgage finance system, and providing recommendations on ways to reform the system to put it on a more sustainable path for the long-term.

This month we chat with Rohit Gupta, President and CEO at Enact. Enact, previously known as Genworth Mortgage Insurance, is an operating segment of Genworth Financial that has provided MI products and services in the U.S. since 1981. Enact operates across all 50 states and the District of Columbia, working with lenders and other partners to help people responsibly achieve and maintain the dream of homeownership by ensuring the broad availability of affordable low down payment mortgage loans.

Gupta talks about the company’s new brand and how it is better positioned to serve low down payment borrowers and the first-time homebuyer market. He also discusses the housing supply and what the U.S. government can do to help increase homeownership.

(1) Your company recently changed its name yet remains committed to helping families across the country either purchase a home or refinance existing mortgages to lower interest rates. Can you speak to the important role that Enact and private mortgage insurance plays in the housing finance system?

You are absolutely correct! We did change our name to Enact, and along with our lending partners, we remain committed to helping more low down payment borrowers safely and affordably achieve the dream of homeownership. Over the years, we have built upon our trusted reputation for quality service, in-depth understanding of our customers’ business, best-in-class underwriting, and risk and capital management expertise through multiple housing cycles.

Private mortgage insurance (PMI) is imperative in order for borrowers with low down-payments to have access to home mortgage financing options. Our Chief Economist Tian Liu’s annual First-Time Homebuyer Market Report highlights how the housing finance system continued to perform well during the fourth quarter of 2020, as the PMI industry ensured access to credit for first-time homebuyers. Credit availability for potential first-time homebuyers can be especially vulnerable given this segment of the market relies heavily on low down payment mortgages. For the full year (2020), low down payment conventional mortgages backed by PMI financed approximately 900,000 first-time homebuyers, that’s a 25% increase from 2019. Even in the midst of the global COVID-19 pandemic, the mortgage industry quickly and successfully shifted a large number of employees from the office to working from home by leveraging technology. This ensured that qualified borrowers could continue accessing credit, while maintaining social distancing protocols.

(2) Please tell us about your quarterly first-time homebuyer market report. Your last report highlighted how 2020 was an unprecedented year, resulting in a record number of first-time homebuyers. Why do you believe this was the case? And what should the industry continue to do or improve to keep first-time homebuyers accessing the housing market?

Our quarterly first-time homebuyer market report provides comprehensive coverage for the first-time homebuyer market, covering conventional, Federal Housing Administration (FHA), VA, USDA as well as the non-agency market. 2020 was a unique year because a number of factors came together – single-family homes became our office, children’s classroom, family’s restaurant, movie theater, and gym. Even as we start to see light at the end of the tunnel, homes will likely take on a bigger role for many people, making them more valuable to potential buyers.

Demographically, we’re also seeing the peak demand from the Millennial generation, the largest cohort in history. Cyclically, interest rates are at record-low levels, which supports housing affordability. Last year, the industry was instrumental in helping borrowers and lenders cope with record demand when shelter and safety were more important than ever for people, and we should continue to rely on technology and data to help potential first-time homebuyers. Our product makes a low down-payment possible, and today serves more first-time homebuyers than any other low down-payment mortgages. I believe that is something the industry should continue focusing on and sharing with the mortgage industry.

(3) The record-low housing supply is consistently increasing home prices. How is this affecting borrowers’ ability to purchase a home?

Today, rising home prices and the lack of inventory are major hurdles for homebuyers. Our industry has limited ability to influence housing supply, but we do and can play a role in making the down payment more affordable through our product. Also, we play an important role in educating borrowers on becoming responsible homeowners and lenders on our products to help their borrowers. Finally, we play an important role in keeping the mortgage origination and servicing process efficient, thereby lowering the cost to borrowers.

(4) Do you think this first-time homebuyer trend could persist? If so, why? And if not, what can the industry stakeholders and government do to ensure future generations can obtain the American Dream of buying a home?

I am optimistic about the first-time homebuyer trend because of its close relationship to homeownership. The COVID-19 pandemic has made homes and homeownership more important than ever. Even though demand continues to outpace supply, supply has been expanding. Housing starts have been over the 1.5-million-unit pace (the historical average) in seven of the past eight months. It will take some time for supply to catch up to demand, but I am confident that the housing industry will be able to deliver.

Rohit Gupta’s Biography

Rohit Gupta, President and CEO of Enact, is passionate about helping more people responsibly achieve and maintain the dream of homeownership. Rohit works with lenders, regulators, and policy leaders to advocate for the value of mortgage insurance to a sustainable housing finance system.

Along with his advocacy, Rohit served as chairman and remains a Board member of the U.S. Mortgage Insurers trade association. He also serves on the Boards of the Mortgage Bankers Association Residential Board of Governors and Housing Policy Executive Council. Additionally, Rohit is a catalyst for community change and serves as the chair of the Genworth Foundation Board, and a board member of American Cancer Society Triangle Leadership Council, and Pratham USA.

Prior to being named CEO, Rohit held the positions of Chief Commercial Officer & Senior Vice President of Products, Intelligence and Strategy, as well as Vice President – Commercial Operations. Rohit has an MBA in Finance from University of Illinois at Urbana Champaign and an undergraduate degree in Computer Science & Technology from Indian Institute of Technology. He resides in Raleigh, North Carolina with his wife and two children.

Blog: Washington Focuses on Infrastructure and Equity with an Eye Toward Homeownership

At the midpoint of the first session of the 117th Congress, policymakers are shifting their focus from the COVID-19 recovery to other priorities on the horizon, chiefly infrastructure, and proposed changes to the tax code to fund investments.

Congressional Democrats are rallying around President Biden’s infrastructure proposals, the American Jobs Plan and American Families Plan, which take a holistic view of infrastructure by including traditional infrastructure projects like roads, bridges, railways, and housing as well as non-traditional infrastructure concepts like universal preschool and childcare. Specifically, Democrats are championing housing policies intended to promote equitable communities and give traditionally underserved Americans a stake in those communities. This includes increasing access to homeownership and wealth-building opportunities.

While both parties agree on the need to upgrade the nation’s roads and bridges, and increase broadband access, Republicans and some Democrats have expressed concerns about the expansive scope of the proposed infrastructure projects, along with certain “pay for” provisions.

Housing and Homeownership in America

There is also growing bipartisan attention to the state of housing in the U.S. Even while a record number of first-time homebuyers entered the market in 2020, longstanding concerns about housing access and affordability have been amplified due to rapidly rising home prices. While homeowners have experienced significant equity gains over the past several years, including nearly 11 percent in 2020, strong home price appreciation (HPA) and severely limited supply has locked some borrowers out of the market. This situation has raised concerns from both Republicans and Democrats, as some of the strongest HPA has occurred in rural states.

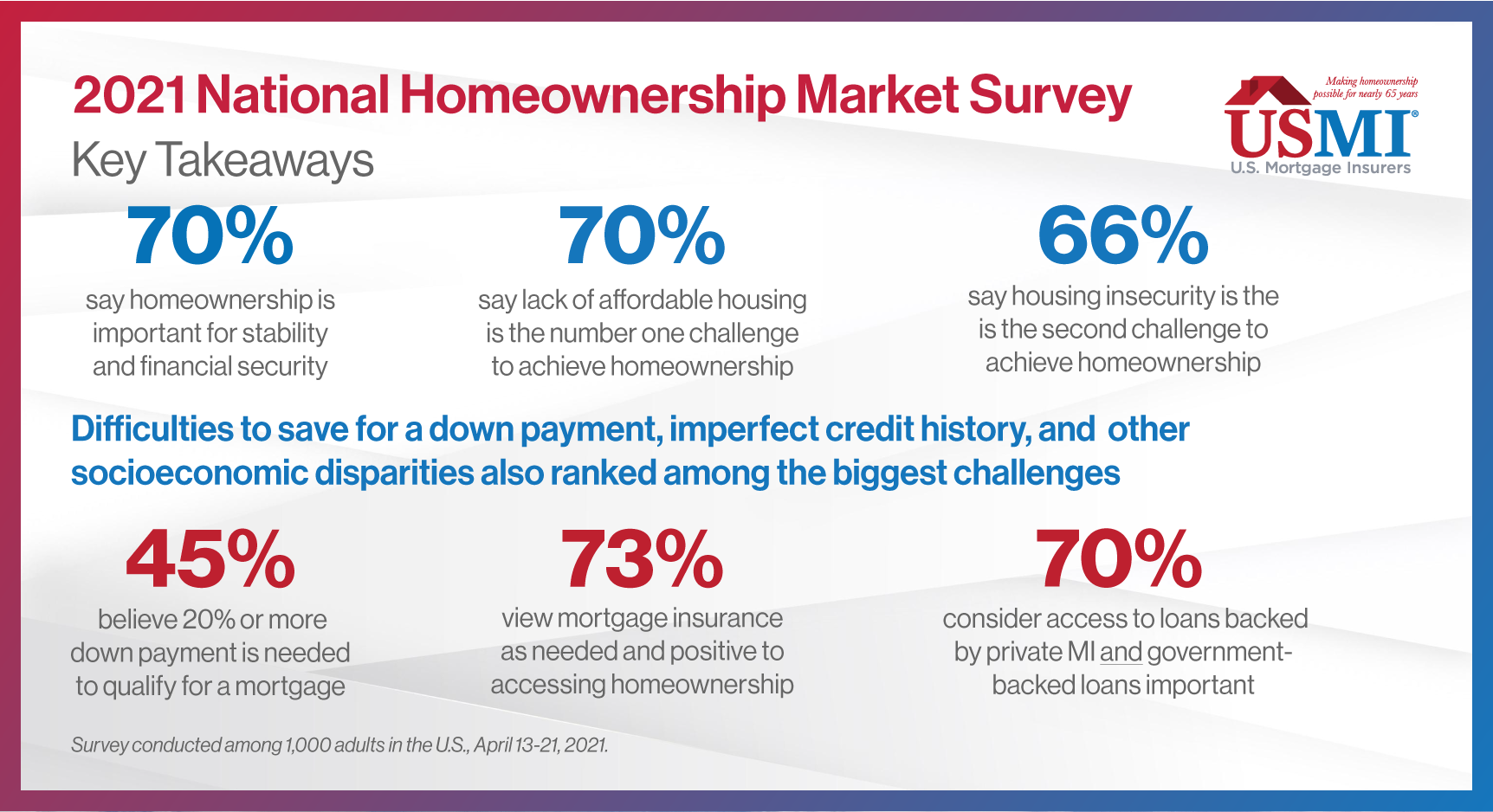

These trends have garnered nationwide attention as the effects of COVID-19 reinforced the importance of stable housing, and the value of homeownership and wealth building among Americans. Simultaneously, Millennials aspire to enter the home purchase market in larger numbers. Today, interest rates are low but as interest in homeownership has risen among first-time buyers, so has its cost. Additionally, in a tight purchase market, affordability—and the 20 percent down payment that 45 percent of Americans believe is required to obtain a mortgage, as reported in USMI’s 2021 National Homeownership Market Survey—is farther out of reach, particularly for those who do not have intergenerational wealth or equity from a previous/current home.

Not only policymakers are eyeing solutions to these challenges. As employers look to attract and retain younger workers, some companies have introduced innovative ways to help employees bridge the down payment gap, or other ways to sustainably increase housing affordability. Redwood Trust has introduced a benefit—the Redwood Employee Home Access Program—that covers the cost of mortgage insurance (MI) for employees. When the program launched in April 2021, Redwood CEO Chris Abate noted that “homeownership is the bedrock of our communities. It builds family wealth and contributes to a sense of inclusion, security, and wellbeing,” and added that Redwood seeks to put homeownership within reach of all its employees. Abate encouraged other employers to offer this benefit, similar to subsidizing health insurance. This type of incentive increases affordability, while also maintaining sustainability, as MI will remain in place and offer protection against the risk of higher loan-to-value loans.

Housing Supply is Critical

In Washington, the conversations around housing access and affordability have recognized the impact of limited housing supply on house prices as a primary driver of around affordability issues. Strong demand over the past twelve months has exacerbated the dearth of supply of such homes, construction of which has lagged pre-2008 levels. Congress has already introduced a variety of bipartisan legislation focused on increasing the supply of housing for low- and middle-income Americans, including the “Yes in My Backyard Act” (HR 3198/S 1614) and the “Housing Supply and Affordability Act” (HR 2126/S 902). Further, President Biden’s proposed budget for fiscal year 2022 contains tax incentives for the construction of low-income housing units for both renters and owner-occupants. Democratic infrastructure proposals aim to further increase supply by dedicating funding for affordable housing development.

Bridging the Down Payment Gap

USMI’s 2021 National Homeownership Market Survey noted that the inability to save for a down payment is among the biggest challenges Americans face when it comes to buying a home. The Biden administration and Congressional Democrats are also aware of this, and how it particularly affects those who lack intergenerational wealth to bridge the down payment gap and first-time homebuyers facing a historically competitive housing market. A number of legislative proposals have been put forward related to down payment assistance (DPA) and supporting homeownership. However, policymakers remain cognizant that the housing market does not need additional demand pushed into the market—the key will be increasing homeownership, particularly among traditionally underserved groups, without further decreasing affordability in the housing market.

First-Time/First-Generation DPA Proposals:

“Housing Is Infrastructure Act of 2021”: Released on April 14, House Financial Services Committee (HFSC) Chairwoman Maxine Waters (D-CA) introduced a bill including legislative text (Section 116) for targeted DPA which also exists as a standalone bill, the “Down Payment Toward Equity Act of 2021”. Chairwoman Waters’ proposal appropriates up to $10 billion for targeted DPA that is limited to first-time, first-generation homebuyers (although those who have lost homes due to foreclosure, deed-in-lieu or short sale also are eligible). Further, income for qualified recipients is limited to 120 percent of area median income (AMI), except in areas with high costs of housing, in which case income limit rises to 180 percent of AMI. Down payment grants are limited to $20,000 (or $25,000 in the case of a qualified homebuyer who is a socially and economically disadvantaged individual). The bill also includes conditional repayment terms for recipients who sell their home within five years.

“American Housing and Economic Mobility Act of 2021”: Introduced on April 22 by Rep. Emanuel Cleaver (D-MO) and Sen. Elizabeth Warren (D-MA), the American Housing and Mobility Act aims to increase housing supply and mitigate the historical effects of discriminatory lending. It provides for DPA grants for first-time homebuyers with incomes <120 percent of AMI and who have resided at least four years in a geographic area that was historically denied access to mortgage finance due to official government policy. The bill also proposes investing $445 billion over 10 years in the Housing Trust Fund, and $25 billion over 10 years in the Capital Magnet Fund.

“First-Time Homebuyer Act”: Introduced on April 26 by Reps. Earl Blumenauer (D-OR) and Jimmy Panetta (D-CA), the First-Time Homebuyer Act would provide a tax credit for first-time homebuyers for the lesser of 10 percent of the purchase price of the property acquired or $15,000 for joint tax filers.Assistance would be restricted to homebuyers with incomes ≤160 percent of AMI purchasing homes for ≤110 percent of their area’s median purchase price. This legislation is similar to President Biden’s campaign proposal to provide $15,000 tax credits to homebuyers.

Comparison of DPA Legislation

| Down Payment Toward Equity Act | American Housing and Economic Mobility Act | First-Time Homebuyer Act | |

| Lead Sponsor | Rep. Waters (D-CA) | Rep. Cleaver (D-MO) & Sen. Warren (D-MA) | Rep. Blumenauer (D-OR) |

| Structure | Grant with 5-year occupancy requirement (5-year repayment schedule in the event homeowner sells the property) | Grant | Tax credit with a 4-year recapture period |

| Maximum Assistance | $20k and $25k for homebuyers who are socially and economically disadvantaged individuals | ≤3.5% of the appraised value of the property (or ≤3.5% of maximum principal obligation if the appraised value exceeds the principal obligation amount) | Lower of 10% of the purchase price or $15k (for married tax filers) subject to inflation |

| Targeting | |||

| First-time Homebuyer requirement | Yes and first-generation | Yes and have lived for 4 years prior to enactment in a geographic area historically subject to discrimination or official segregation | Yes |

| Income Restriction | ≤120% of AMI and ≤180% of AMI for properties located in high-cost areas | <120% of AMI | Modified AGI ≤160% of AMI |

| Purchase Price Restriction | N/A | N/A | ≤110% of area median purchase price for full tax credit amount |

| Housing Counselling Required | Yes | Not required | Not required |

Tax Incentives to Support Homeownership:

“American Dream Down Payment Act”: Introduced in February by Reps. Gregory Meeks (D-NY), Joyce Beatty (D-OH), and Al Green (D-TX), the American Dream Down Payment Act would establish qualified down payment savings programs to open tax-advantaged accounts (similar to 529 accounts for educational expenses) to save for a down payment, including closing costs, for the purchase of a principal residence. There is no “first-time homebuyer” requirement for the use of the funds in the account, and the maximum account balance would be $102,080 subject to annual increase based on inflation.

Building Home Equity Among Underserved Borrowers:

In an effort to enable first-generation homeowners to build home equity more rapidly, Sen. Mark Warner (D-VA) has also proposed subsidized 20-year mortgages for first-generation homebuyers. Using a one-time federal subsidy to lower the interest rate, the monthly payments on such a mortgage would be comparable in gross terms to 30-year mortgages for the same property.

More details about these proposals and efforts to increase the housing supply are expected to emerge as Congressional negotiations over infrastructure continue this Summer and Fall.

Statement: Nomination of Julia Gordon to Serve as FHA Commissioner

WASHINGTON — Lindsey Johnson, President of U.S. Mortgage Insurers (USMI), issued the following statement on the White House’s nomination of Julia Gordon to serve as Assistant Secretary for Housing, Federal Housing Commissioner, Department of Housing and Urban Development (HUD):

“USMI applauds the nomination of Julia Gordon to serve as Federal Housing Commissioner to lead the Federal Housing Administration (FHA). Gordon has broad experience in the housing finance system, specializing in supporting affordable homeownership and consumer protection policies for underserved markets. Her previous work, including nearly six years leading the National Community Stabilization trust (NCST), public service as manager of the single-family policy team at the Federal Housing Finance Agency (FHFA), and four years as senior policy counsel at the Center for Responsible Lending (CRL), will allow her to efficiently address the important issues facing the housing industry. We look forward to working closely with Gordon in seeking to promote a complementary, collaborative, and consistent housing finance system that enables sustainable homeownership for American families while also protecting taxpayers.”

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

Podcast: President Lindsey Johnson on “Radian On Air”

USMI President Lindsey Johnson appeared on “Radian On Air” podcast with Radian President of Mortgage and USMI Chairman Derek Brummer. On the episode titled, “National Homeownership Month: Expanding Minority Homeownership,” they discussed the importance of homeownership, barriers for first-time homebuyers, solutions to address low housing supply, and the role of private MI in promoting homeownership.

Listen here.

Blog: Key Takeaways from National Homeownership Market Survey

On June 22, USMI released the results of its 2021 National Homeownership Market Survey. ClearPath Strategies fielded the national survey among 1,000 U.S. adults in the general population from April 13-21. Quotas were set to ensure a cross sample of age, gender, race, region, and education as well as homeowners, first-time homebuyers, and prospective homebuyers. The purpose was to understand the perceptions around homeownership, the mortgage process, and the challenges people face when trying to purchase a home.

This blog is the first in a series that will explore the findings from this comprehensive survey around the housing and mortgage markets in the United States. We kick off the series with the seven key takeaways from the national survey. The complete findings from USMI’s national survey are available here.

- Owning a home matters. More than 7 in 10 respondents see owning a home as important for stability and financial security. However, as we dig into the other key findings, economic and access gaps lead to challenges to buying a home.

- Lack of affordable housing and low supply of housing ranked among the top homebuying challenges. In fact, nearly 7 in 10 respondents ranked the lack of affordable housing as the number one housing challenge and nearly 6 in 10 stated that low housing supply is another top issue. This is contextualized by the current historically low housing supply, which is most acute in the “starter home” segment of the market.

- Housing insecurity during the pandemic was also a significant concern for Americans, particularly among minorities. Sixty-six percent of all respondents ranked housing insecurity, including concerns about the ability to make mortgage and rental payments, as the second highest housing challenge. A further dive into the survey findings underscores these economic concerns are particularly acute among minorities. African Americans and Hispanics said that falling behind on rent or mortgage payments was their number one concern. Twice the number of African American respondents (20 percent) and more than one-half times the number of Hispanic respondents (16 percent) reported this concern compared to white respondents (10 percent).

- The inability to save for a down payment and imperfect credit history also ranked among the biggest challenges to buying a home. African American (74 percent) and Hispanic (66 percent) respondents reported that in addition to the lack of affordable homes or lack of supply on the market, the inability to save for a down payment (39 percent of all minorities) and imperfect credit history (37 percent of all minorities) are the biggest challenges they face when it comes to buying a home. Of all adults surveyed, 60 percent view “credit score” as having the most impact on the cost of a mortgage, while 81 percent said they understand the factors that impact one’s credit score and 79 percent view credit scores as being fair.

- Socioeconomic disparities – such as lower income, lack of intergenerational wealth, limited savings, and the percentage of monthly income dedicated to housing costs – only add to the challenges to buying a home. These factors can lead to lower credit scores and higher overall debt loads to manage, which all can contribute to greater challenges to achieving homeownership. African American and Hispanic respondents rank these issues as more significant challenges compared to white respondents.

- Many Americans still do not realize that low down payment mortgages are widely available. Up to 45 percent of all respondents mistakenly believe that you need a down payment of 20 percent or more to qualify for a mortgage. Thirty percent of all adults surveyed indicate that they are not familiar with down payment requirements. In truth, homebuyers can qualify with a down payment as low as 3 percent with private mortgage insurance, and as low as 3.5 percent with a loan backed by the Federal Housing Administration (FHA).

- While down payments continue to be a significant challenge, mortgage insurance (MI) is seen as leveling the playing field and respondents express strong support for access to mortgages with MI in both the conventional and government-backed markets. Seventy-three percent of all respondents view mortgage insurance as needed and positive to accessing homeownership. MI provides access to home financing for those who might not otherwise be able to purchase a home due to limited funds for a down payment. Nearly 70 percent of respondents cited that it was important to have access to loans through the conventional market backed by private MI and government-backed loans through the FHA.

Newsletter: June 2021

June marks the official start of summer and National Homeownership Month. This week, USMI released its 2021 National Homeownership Market Survey, which examined perceptions around homeownership, the mortgage process, and the challenges people face when trying to purchase a home. USMI also released its annual MI in Your State report in early June, which found borrowers were able to access home financing three times sooner in 2020 because of private mortgage insurance (MI). We dig further into these reports and more below.

USMI’s 2021 National Homeownership Market Survey

Black Homeownership Collaborative Launches in Ohio

USMI’s MI in Your State Report

Supreme Court Decision: Collins v. Yellen

Federal Agencies Extend Foreclosure Moratoria

MI Premium Tax Deductibility Proposal in Congress

Credit Risk Retention Rule

HUD Confirmations and Nominations

What We’re Listening To: “Radian On Air” Podcast

What We’re Watching: New American Funding Panel on Down Payment Assistance & Increasing Black Homeownership

What We’re Reading: Redwood Trust’s Employee Home Access Program

USMI’s 2021 National Homeownership Market Survey. On June 22, USMI released its 2021 National Homeownership Market Survey. This new research, fielded by ClearPath Strategies to 1,000 adults in the U.S., found that nearly 7 in 10 (69 percent) ranked lack of affordable housing and nearly 6 in 10 (57 percent) ranked low housing supply among the biggest homebuying challenges. The survey also specifically looked at these responses by race to better understand minorities’ perceptions and challenges around homeownership, housing affordability, and the mortgage process. It also revealed that many people continue to not understand the down payment requirements to purchase a home. Housing insecurity (66 percent) was also among the top concerns from respondents. Socioeconomic disparities – such as lower income, lack of intergenerational wealth, limited savings, and the percentage of monthly income dedicated to housing costs – were reported to make these challenges more acute, particularly among minorities.

Black Homeownership Collaborative. In collaboration with more than 100 organizations and individuals involved in the Black Homeownership Collaborative, USMI supports policies that promote equity and work to increase homeownership rates among Black Americans. On June 18, the Collaborative unveiled a solutions-based initiative to close the Black homeownership gap. The Collaborative’s seven-point plan includes homeownership counseling, targeted down payment assistance, housing production, credit and lending reforms, civil and consumer rights enforcement, advancing homeownership sustainability, and marketing and outreach. The goal is to create 3 million net new Black homeowners by 2030. Read more at 3by30.org.

USMI’s MI in Your State Report. On June 2, USMI released its annual MI in Your State report on the role of private MI in all 50 states and the District of Columbia. The report found that home loans backed by private MI increased 53 percent in 2020, with more than 2 million borrowers securing mortgage financing — a record year for the industry’s 65-year-history. The report also found that saving for a 20 percent down payment could take potential homebuyers 21 years — three times longer than it could take to save 5 percent down. Texas, California, Florida, Illinois, and Michigan were the top five states for mortgage financing with private MI. Fact sheets for all 50 states, plus the District of Columbia, are available here.

Supreme Court Decision: Collins v. Yellen. On June 23, the Supreme Court released its opinion for Collins v. Yellen, giving the U.S. President greater control over the Federal Housing Finance Agency (FHFA) and the future of the government-sponsored enterprises (GSEs), Fannie Mae and Freddie Mac. The Court held that “[t]he Recovery Act’s restriction on the President’s power to remove the FHFA Director, 12 USC 4512(b)(2), is unconstitutional.” This provides President Biden with the authority and opportunity to nominate a new FHFA Director who will be in better alignment with the Biden Administration’s policy positions and priorities. The Court also held that GSE shareholders’ statutory claim must be dismissed since the FHFA’s actions regarding the Net Worth Sweep did not exceed its “powers or functions” as a conservator. This is undoubtedly a significant determination for the future of the leadership of FHFA, as well as the future of the GSEs. USMI continues to promote a housing finance system that is backed by private capital, and also promotes sensible reforms to the GSEs that include utility-like regulation of the GSEs.

Following the Court’s opinion, President Biden appointed Sandra Thompson, formerly the Deputy Director of the Division of Housing Mission and Goals, as the Acting Director of the FHFA. Prior to joining the FHFA in 2013, Acting Director Thompson spent more than 23 years at the Federal Deposit Insurance Corporation (FDIC), most recently as the Director of the Division of Risk Management Supervision. Her experience in financial supervision, consumer protection, and outreach will continue to benefit the FHFA and housing finance system. USMI looks forward to continued engagement with Acting Director Thompson and her FHFA colleagues to promote a robust conventional mortgage market and access to affordable mortgage credit.

Federal Agencies Extend Foreclosure Moratoria. On June 24, the White House announced a number of actions to protect renters and homeowners still experiencing financial hardships due to the COVID-19 pandemic. The Administration indicated that the U.S. Department of Housing and Urban Development (HUD), U.S. Department of Veterans Affairs (VA), and U.S. Department of Agriculture (USDA) are extending their foreclosure moratoria for one month, until July 31, 2021, and that homeowners with mortgages insured or guaranteed by the agencies may enter into COVID-related forbearance through September 30, 2021. FHFA followed with a statement that the GSEs are extending their foreclosure moratoria on single family foreclosures and real estate owned (REO) evictions through July 31, 2021. Homeowners with GSE-backed single family mortgages continue to be eligible for COVID-related forbearance.

Credit Risk Retention Rule. On June 11, USMI joined with several other housing and finance organizations on a comment letter to banking and housing regulators. The letter provided observations and recommendations with respect to the review of certain provisions of the 2014 Credit Risk Retention Rule that was jointly issued by the Office of the Comptroller of the Currency, the Board of Governors of the Federal Reserve System, the FDIC, the Securities and Exchange Commission, the FHFA, and HUD. Following careful analysis of the changes issued by the Consumer Financial Protection Bureau (CFPB) in its final Qualified Mortgage (QM) rule, the organizations expressed strong support for the continued alignment of the Qualified Residential Mortgage (QRM) and QM frameworks.

HUD Confirmations and Nominations. This month, Adrianne Todman was confirmed as HUD’s Deputy Secretary, Damon Smith was nominated to serve as the agency’s General Counsel and Julia Gordon was nominated to serve as the commissioner of the Federal Housing Administration (FHA). Smith previously served as the acting general counsel for HUD in 2014. Gordon had managed the single-family policy team at the FHFA from 2011 to 2012, and more recently, was a member of the FHFA and HUD agency review team for the Biden administration. USMI looks forward to working with HUD leadership and the FHA team on policies to best serve borrowers and responsibly facilitate access to homeownership.

What We’re Listening To: “Radian On Air” Podcast. Lindsey Johnson sat down with Radian President of Mortgage and current USMI Chairman Derek Brummer for the company’s latest podcast episode of “Radian On Air” titled, “National Homeownership Month: Expanding Minority Homeownership.” They discussed the importance of homeownership, barriers for first-time homebuyers, solutions to address low housing supply, and the role of private MI in promoting homeownership. Listen to the full episode here.

What We’re Watching: New American Funding Panel on Down Payment Assistance & Increasing Black Homeownership. On May 20, Lindsey Johnson joined Freddie Mac’s Sam Noel, and Stockton Williams, Executive Director of National Council of State Housing Agencies, in a virtual discussion hosted by New American Funding for its New American Dream initiative. Panelists discussed the pressing problem of bridging the down payment gap, how potential homebuyers can overcome that obstacle, and how to increase and sustain Black homeownership.

What We’re Reading: Redwood Trust’s Employee Home Access Program. In case you missed it, Redwood Trust announced its Employee Home Access Program (“the Redwood Benefit”), an MI benefits program for its workforce that supports employees seeking a path to homeownership. Through the program, Redwood is reimbursing all MI costs to help its employees put down roots in areas of their choosing. Citing limited access to affordable housing supply and challenges to access affordable housing, Redwood CEO, Chris Abate encouraged other corporate leaders to offer MI support for their employees: “If as a corporate leader you’re focused on environmental, social and governance objectives, I urge you to consider this benefit for your employees, too.”

Blog: 2021 National Homeownership Market Survey

ClearPath Strategies fielded USMI’s 2021 National Homeownership Market Survey of 1,000 adults in the U.S. It was commissioned online April 13-21. Quotas were set to ensure a cross sample of age, gender, race, region, and education as well as homeowners, first-time homebuyers, and prospective homebuyers. The purpose was to understand the perceptions around homeownership, the mortgage process, and the challenges people face when trying to purchase a home.

The survey finds that 7 in 10 say lack of affordable housing is the biggest homebuying challenge in the United States, while many do not understand down payment requirements. Housing insecurity (66 percent) and low supply (57 percent) closely followed. Socioeconomic disparities – such as lower income, lack of intergenerational wealth, limited savings, and the percentage of monthly income dedicated to housing costs – were reported to make these challenges more acute.

“This survey underscores the need to address the nation’s undersupply of housing, and specifically affordable housing, because too many people are being left out of the market or face significant barriers to get into the housing market,” said Lindsey Johnson, President of USMI. “Our survey shows that low- to moderate-income households and underserved communities struggle to become homeowners due to several major factors including low housing supply, lack of affordable housing, and personal economic factors such as imperfect credit score or the inability to afford a 20 percent down payment.”

USMI members continue to help millions of borrowers bridge the down payment gap. USMI supports sensible regulatory and legislative reforms to further address barriers to homeownership and promote an equitable and sustainable housing finance system backed by private capital. In collaboration with more than 100 organizations and individuals involved in the Black Homeownership Collaborative, USMI also supports policies that promote equity and work to increase homeownership rates among Black Americans.

Full survey results can be found here. Press release on the survey can be found here.

Press Release: National Survey Confirms Low Housing Supply and Lack of Affordable Housing Among Biggest Homebuying Challenges for Minorities and Americans Overall

2021 National Homeownership Market Survey Also Finds Most Americans Don’t Understand Availability of Low Down Payment Mortgage Options

WASHINGTON — U.S. Mortgage Insurers (USMI) today released its 2021 National Homeownership Market Survey that finds nearly 7 in 10 (69 percent) ranked lack of affordable housing and nearly 6 in 10 (57 percent) ranked low housing supply among the biggest homebuying challenges in the United States. The survey also revealed that many people continue to not understand the down payment requirements to purchase a home. Housing insecurity (66 percent) was also among the top concerns from respondents. Socioeconomic disparities – such as lower income, lack of intergenerational wealth, limited savings, and the percentage of monthly income dedicated to housing costs – were reported to make these challenges more acute. The survey also specifically looked at these responses by race to better understand minorities’ perceptions and challenges to homeownership.

“This survey underscores the need to address the nation’s undersupply of housing, and specifically affordable housing, because too many people are being left out of the market or face significant barriers to get into the housing market,” said Lindsey Johnson, President of USMI. “Our survey shows that low- to moderate-income households and underserved communities struggle to become homeowners due to several major factors including low housing supply, lack of affordable housing, and personal economic factors such as imperfect credit score or the inability to afford a 20 percent down payment.”

USMI’s survey found that when broken down by race these economic factors are even more pronounced. Seventy-four percent of African American and 65 percent of Hispanic respondents reported that in addition to the lack of affordable homes or low supply, the inability to save for a down payment (39 percent of all minorities) and imperfect credit history (37 percent of all minorities) are the biggest challenges they face when it comes to buying a home.

Housing insecurity during the pandemic was also a significant concern among survey respondents, particularly for minorities. The number one concern among African American and Hispanic respondents was falling behind on rent or mortgage payments. In fact, twice the number of African American respondents (20 percent) and more than one and half times the number of Hispanic respondents (16 percent) reported this concern compared to white respondents (10 percent).

“The survey also shows that more education is needed around the mortgage finance process, particularly to ensure more buyers understand that low down payment mortgage options are widely available,” said Johnson.

USMI’s survey found that up to 45 percent of all respondents mistakenly believe that you need a down payment of 20 percent or more to qualify for a home purchase. Another 30 percent indicated that they do not know about down payment requirements. In truth, you can qualify with a down payment as low as 3 percent. The survey also asked respondents about the role of mortgage insurance. According to survey respondents, the top reasons for MI are it “levels the playing field” and “increases lower-income families’ access to homeownership.” A majority of respondents also said it was important to have access to low down payment loans through both the conventional and government-backed markets, such as the Federal Housing Administration (FHA).

USMI members support sensible regulatory and legislative reforms to remove barriers to homeownership, and they promote an equitable and sustainable housing finance system backed by private capital. In collaboration with more than 100 organizations and individuals involved in the Black Homeownership Collaborative, USMI also supports policies that promote equity and work to increase homeownership rates among Black Americans.

ClearPath Strategies fielded USMI’s 2021 National Homeownership Market Survey of 1,000 adults in the U.S. It was commissioned online April 13-21. Quotas were set to ensure a cross sample of age, gender, race, region, and education as well as homeowners, first-time homebuyers, and prospective homebuyers. The purpose was to understand the perceptions around homeownership, the mortgage process, and the challenges people face when trying to purchase a home.

The complete findings from USMI’s national survey are available here.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org