News Filter: Blog

Blog: Do the math – Buying a home now is possible

With record low housing supply and high inflation contributing to skyrocketing home prices, the barriers to owning a home may seem insurmountable. But buying a home in a sustainable, affordable way is possible with low down payment mortgage options. First-time and low- to medium-income homebuyers can qualify for mortgage financing without emptying their bank accounts and can keep some cash on hand for home improvements or a rainy-day fund.

Conventional home loans backed by private mortgage insurance (MI) have been available for borrowers for decades and helped nearly 2 million homebuyers in the past year purchase or refinance a mortgage. Private MI is a temporary cost that allows for a down payment as small as 3% of the purchase price. While some borrowers wait until they save 20% for a down payment, the added years of saving can translate to higher interest rates, more expensive home prices and lost home equity.

“Renters who are on the hunt to buy should do the math and consider what is best for them, because often they will find that purchasing with a low down payment mortgage provides buyers with an ability to access the market sooner, and ends up being a significant advantage for them,” said Lindsey Johnson, president of U.S. Mortgage Insurers (USMI).

In today’s market, it could take a family earning the national median income up to 21 years to save 20%, according to calculations by USMI.

If you are one of these renters looking to buy your first home but don’t have 20% down, don’t worry: you are not alone. According to the National Association of REALTORS® (NAR), the typical down payment in 2021 was 7% for first-time homebuyers and 17% for repeat homebuyers.

How can buying now save you money later?

Consider you want to purchase a $375,000 home, the median sales price for a single-family home in 2021, according to NAR. A 5% down payment is $18,750 versus $75,000 for 20% down. With a 740 credit score at today’s MI rates, your monthly MI payment would be about $157, which is included in your monthly mortgage payment until the MI can be canceled, usually after five years once you reach 20% equity in the home.

Due to robust home price appreciation (HPA) that came in at 17.5% for 2021, today’s $375,000 home will likely cost more in the years ahead. This will also have an impact on the necessary down payment and length of time required to save for it. There are other variables in the equation too, such as interest rates. As interest rates rise, so too can the cost of mortgage financing.

Not all low down payment mortgages are the same. Importantly, government-backed loans insured by the Federal Housing Administration (FHA) require at least a 3.5% down payment, an upfront charge that must be paid at closing or added to your loan balance, and the monthly insurance is permanent for the life of the loan.

There are many online mortgage calculators that can help. Check out lowdownpaymentfacts.org to learn more.

Blog: Mortgage Insurance Levels the Playing Field

Blog: Celebrating Women’s History Month – Q&A with Prominent Housing Leaders

Blog: Q&A with Faith Schwartz of Housing Finance Strategies

Blog: Q&A with Paula C. Maggio of MGIC

Blog: Q&A with Debra Still of Pulte Financial Services

Blog: Q&A with Meghan C. Bartholomew of Radian

Blog: Where Housing Legislation Stands in an Election Year

By Brendan Kihn, Senior Government Relations Director of USMI

As the country kicks off primary elections in the mere matter of weeks, policymakers and advocacy groups are already sizing up what can and cannot be accomplished before voters go to the polls on November 8 for the 2022 midterm election. Just over a year ago, the Democrats gained control of the White House, Senate, and House of Representatives – their first trifecta since January 2011 – and Democrats were hopeful that the party could advance a long list of policy priorities related to taxation, healthcare, and housing investments. Following the enactment of the American Rescue Plan Act, which included $10 billion in homeowners assistance and $22 billion in emergency rental assistance, and the Infrastructure Investment and Jobs Act (the “Bipartisan Infrastructure Deal”), Democrats turned their attention to the Build Back Better Act (BBB), which includes more than $150 billion in housing investments.

Status Update on the “Build Back Better” Agenda

Policymakers are acutely aware of the affordability challenges facing homebuyers and there is especially bipartisan support for increasing housing supply. BBB, both the specific bill and the Biden Administration’s general policy theme, represents a broad collection of policy objectives and programs which includes initiatives to promote access to homeownership, fair housing, and affordable rental opportunities. BBB’s historic investment in housing includes:

- $65 billion to preserve and rebuild public housing

- $26 billion to create and preserve affordable and accessible housing

- $24 billion for new Housing Choice Vouchers to support families struggling to afford their rent

- $10 billion in down payment assistance for first-time, first-generation homebuyers

- $500 million for a wealth-building home loan program

- $250 million increase in allocation to Federal Home Loan Bank Affordable Housing Programs (AHP)

- $100 million to increase access to small-dollar mortgages

The U.S. House of Representatives passed BBB on November 19 with a 220-113 vote only for the bill to hit a major roadblock in the Senate exactly one month later. On December 19, Sen. Joe Manchin (D-WV) announced that “[d]espite my best efforts, I cannot explain the sweeping Build Back Better Act in West Virginia and I cannot vote to move forward on this mammoth piece of legislation.” The Democrats’ razor thin majority in the Senate (50 plus Vice President Harris) creates a tenuous “working majority,” whereby a single defection or absence can make or break a piece legislation. In this case, it is crystal clear that BBB as passed by the House is dead.

2022 began with a certain degree of legislative soul searching among Democrats to strategize avenues to pass elements of BBB that can either: (1) garner bipartisan support and pass via regular order with a 60-vote threshold in the Senate; or (2) enjoy support from the entire Democratic caucus for passage via reconciliation. Democrats will face internal and external pressure to pass something in an effort to show voters that they can govern and deliver for the American people who handed them the levers of power in the 2020 election. Housing advocates remain adamant that housing investments should be included in any legislative packages that seek to advance the Biden Administration’s BBB agenda. And, while critics are concerned that BBB will “dramatically reshape our society,” there is an equally strong sentiment among others that such a “reshape” is exactly what is necessary to invest in the American people and expand economic opportunities, including access to affordable homeownership.

Expanding Access to Mortgage Finance

USMI, as articled in its “2022 Policy Priorities for Access, Affordability & Sustainability in the U.S. Housing Finance System,” has consistently supported legislative and regulatory reforms to remove barriers to homeownership and promote an equitable and sustainable housing finance system. As policymakers seek to advance equity in the housing finance system and address significant affordability issues, they must thread the needle of expanding access to homeownership without further driving up housing costs in a very tight market. The country is experiencing an alarming shortage of homes, most notably in the “starter home” segment of the market, with only 1.8 months of supply for existing homes at the end of 2021, according to the National Association of Home Builders (NAHB). This has been one of the primary drivers of strong home price appreciation which came in at 17.5 percent for 2021, according to the Federal Housing Finance Agency’s (FHFA) House Price Index (HPI). While home price appreciation is a boon for existing homeowners who rapidly build up equity that can be tapped for other financial goals, increasing house prices represent a real hurdle for families looking to attain homeownership.

Survey and reports, including USMI’s 2021 National Homeownership Market Survey, routinely identify saving for a down payment as one of the primary challenges that families face when it comes to purchasing. Recent year’s home price appreciation demonstrates the critical need to ensure continued robust access to low down payment mortgages, where borrowers can put as little as 3 percent down with private mortgage insurance (MI) and 3.5 percent down with government-backed insurance. However, for those who are unable to cobble together the funds for a 3 or 3.5 percent down payment, non-profit organizations and governmental entities throughout the country operate thousands of down payment assistance (DPA) programs designed to help these homebuyers. Policymakers have honed in on DPA as a tool to expand homeownership and legislative proposals, most notably House Finance Services Committee (HFSC) Chairwoman Waters’ (D-CA) Downpayment Toward Equity Act (H.R. 4495 / S. 2920). These proposals understand the need to focus these programs to those who need assistance most, targeting first-time, first-generation homebuyers. BBB included $10 billion for such a program and housing advocates had called for that number to be increased to $100 billion. In the wake of BBB stalling in the Senate, policymakers in the House are exploring upcoming legislative vehicles to appropriate funds for targeted DPA.

Housing Tax Provisions

Mortgage Insurance Premium Tax Deduction

At the end of 2021, various temporary tax provisions commonly referred to as “tax extenders” expired, including the deduction for MI premiums. Borrowers who are unable to put down 20 percent for their homes typically finance the purchase transaction with loans that have either private MI of government-backed MI through the Federal Housing Administration (FHA), U.S. Department of Veterans Affairs (VA), or U.S. Department of Agriculture (USDA), and these premiums have been tax deductible for many homeowners since 2007. This deduction has been extremely beneficial for first-time, younger, and minority homebuyers who often rely on low down payment mortgages to purchase homes due to limited access to funds or intergenerational wealth for large down payments.

In December 2021, Reps. Ron Kind (D-WI) and Vern Buchanan (R-FL) introduced H.R. 6109 and earlier this month Sens. Maggie Hassan (D-NH) and Roy Blunt (R-MO) introduced S. 3590 to permanently extend the tax deduction for MI premiums and expand taxpayer eligibility by increasing the income threshold. This bipartisan, bicameral legislation would ensure that millions of homeowners continue to benefit from this tax deduction, which in 2019 amounted to an average deduction of more than $2,000.

State and Local Tax Deduction

One housing-related tax provision that has been extremely important to senators from high-cost states (which often happen to be Democratic states) is addressing the $10,000 limit on state and local tax (SALT) deductions through tax year 2025 imposed by the Tax Cuts and Jobs Act of 2017. In fact, changes to the SALT deduction are so high on the priority list for some members of Congress that they have declared “No SALT, no deal” with regard to supporting a BBB-like package. The House-passed version of BBB raised the SALT deduction cap from $10,000 to $80,000 for tax years 2021 through 2030 but, due to no chance of passage in the Senate, the cap remains unchanged. Outside of the BBB legislative process, lawmakers on both sides of the aisle have introduced standalone bills to address, in various manners, the current SALT cap, including:

- SALT Deductibility Act (R. 613 / S. 85) – repeals the temporary cap for tax years 2021 through 2025.

- SALT Fairness Act (R. 202) – repeals the temporary cap for tax years 2021 through 2025.

- SALT Deduction Fairness Act (804) – increases the cap to $20,000 for joint filers for tax years 2021 through 2025.

- SALT Fairness for Working Families Act (R. 2439) – increases the cap to $15,000 for individual filers and $30,000 for joint filers for tax years 2021 through 2025.

As Democrats look for legislative vehicles to address SALT, including upcoming spending bills and smaller packages that advance targeted portions of BBB, there is a growing sense that modifications should be tailored to help middle class Americans and not amount to a giveaway to millionaires and billionaires.

******

The pressure is on for Democrats to deliver on the Build Back Better agenda that was a pillar of the 2020 Biden campaign. One month in Washington, DC is a long time and eight months can seem like an eternity, but all eyes will be on the White House and congressional Democrats’ internal negotiations to determine what housing policies, if anything, can be passed before voters head to the polls in November.

Blog: Addressing the Increasing Costs of Homeownership

Buying a home is the largest single investment most Americans will make, but during the last few years, that dream has become increasingly unreachable for a significant portion of the population as the housing market experiences strong home price appreciation (HPA) and historically low levels of supply. A recent Wall Street Journal article reported on this rising home price trend, outlining how mortgage payments can become unaffordable as a result. According to the Federal Reserve Bank of Atlanta, the median American household would need 32.1 percent of its income to cover mortgage payments on a median-priced home – the most since November 2008, when the same outlays would require 34.2 percent of income. Moreover, the Federal Housing Finance Agency’s (FHFA) 2021 Q3 House Price Index (HPI®) report indicates that house prices were up 4.2 percent compared to the second quarter of 2021, but the real surprise comes when you look over the one year period during which home prices climbed 18.5 percent.

With this in mind, it is no surprise that an increasing number of consumers (64 percent) believe it is a bad time for buying a home, according to Fannie Mae’s latest Home Purchase Sentiment Index (HPSI®). This is a dramatic change from a year ago when that rate stood at only 35 percent, a change driven by consumers’ sentiments that home prices (plurality at 45 percent) and mortgage rates (majority at 58 percent) will increase over the next 12 months.

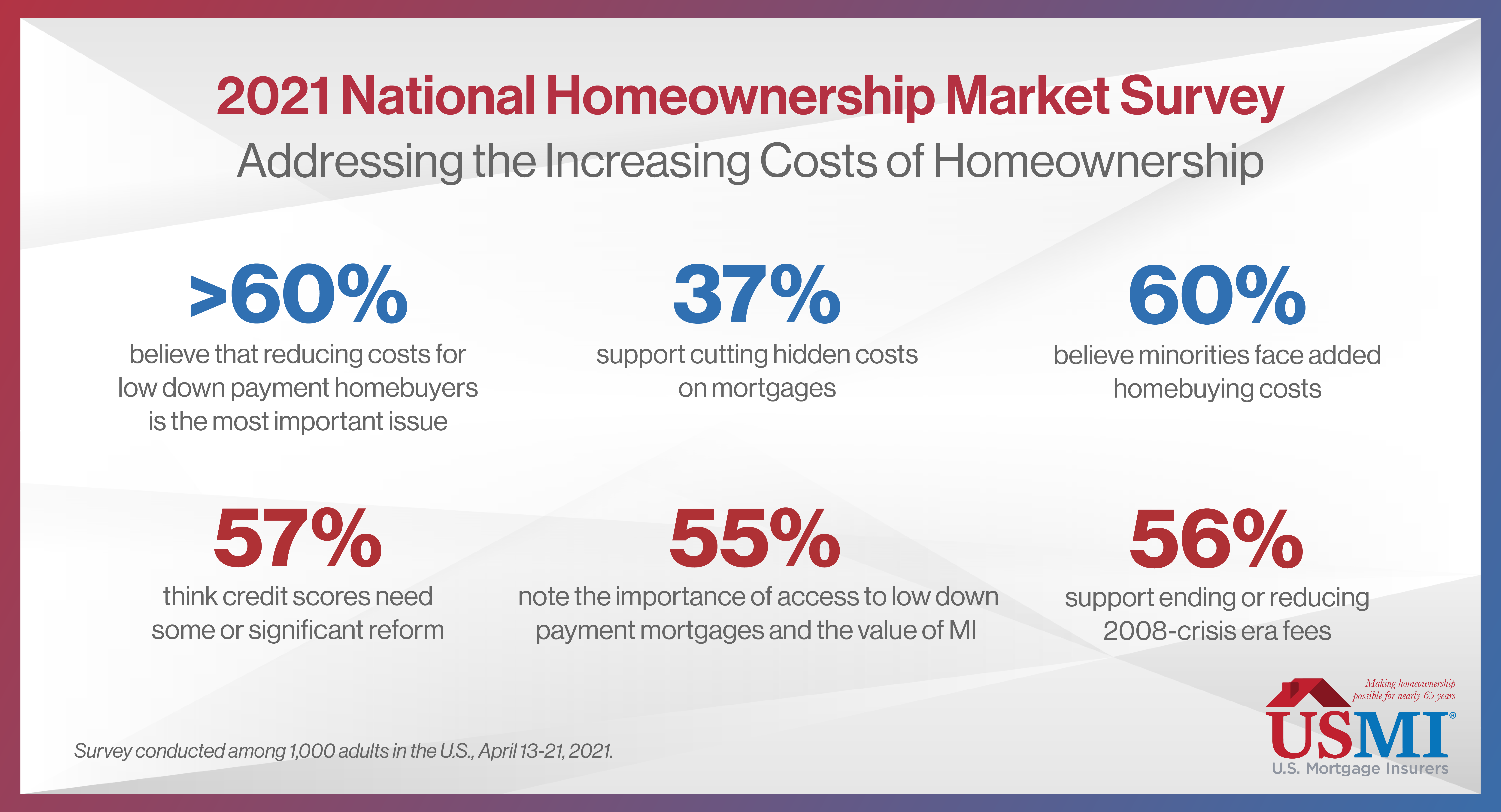

This entire situation only serves to push the goal of owning a home further out of reach for many prospective first-time, minority, and low- to moderate-income (LMI) homebuyers. In addition, there are other fees and charges that potential homebuyers could incur, increasing the cost of homeownership for creditworthy borrowers throughout the country. In fact, USMI’s 2021 National Homeownership Market Survey, which polled 1,000 adults in the U.S., found that 60 percent of respondents believe minorities face added homebuying costs because they tend to have lower credit and higher debt.

Moreover, when asked about the priorities and reforms the housing finance industry should focus on, over 60 percent of respondents believe that reducing costs for low down payment homebuyers is the most important item for the home buying process, and 37 percent support cutting hidden costs on mortgages. Other issues respondents conveyed include:

- Nearly 70 percent of respondents ranked the lack of affordable housing as the number one housing challenge and almost 60 percent stated that low housing supply is another top issue.

- 61 percent of respondents want to eliminate added costs for low down payment homebuyers and 56 percent of respondents specifically support ending Loan-Level Price Adjustments (LLPAs), 2008-crisis era fees that disproportionately affect minority and first-time homebuyers.

- 55 percent of respondents noted the importance of access to low down payment mortgages and the value of mortgage insurance (MI) to help borrowers qualify for mortgage financing.

- 57 percent think credit scores need some or significant reform, driven by respondents’ view that credit score is the underwriting element that most impacts mortgage costs.

Many of the “hidden costs” that borrowers reference when purchasing a mortgage are not really “hidden,” but instead are costs that they may not have anticipated incurring as part of closing the loan. Last week, Fannie Mae released a report titled, “Barriers to Entry: Closing Costs for First-Time and Low-Income Homebuyers,” which finds “[i]n a sample of approximately 1.1 million conventional home purchase loans acquired by Fannie Mae in 2020, median closing costs as a percent of home purchase price were 13 [percent] higher for low-income first-time homebuyers than for all homebuyers, and 19 [percent] higher than for non-low-income repeat homebuyers.” The report also finds that “Black and white Hispanic low-income first-time homebuyers on average paid higher closing costs relative to purchase price than their white non-Hispanic or Asian counterparts […] For some low-income first-time homebuyers, closing costs can be particularly onerous.” Fannie Mae found that some of these “homebuyers had closing costs equal to or exceeding their down payment.”

The FHFA released an Equitable Housing Finance Plans Request for Input (RFI) in September 2021, and the government sponsored enterprises (GSEs), Fannie Mae and Freddie Mac, are required to submit Equitable Housing Finance Plans to FHFA by December 31, 2021. The plans will be in effect on January 1, 2022. USMI submitted its comment to the RFI in October. Given the private MI industry is one of the only forms of private capital available through market cycles and whose core business is focused on helping people without large down payments achieve affordable and sustainable homeownership, private MIs share the FHFA and GSEs’ view that the two pillars of good mortgage lending are sustainability and affordability. The goal should be a strong housing finance system that ensures equitable access to all mortgage-ready borrowers. USMI strongly supports efforts to remove barriers to homeownership and increase access and affordability, including for historically underserved households, while instilling sustainability for these same borrowers. The MI industry welcomes the opportunity to work with the FHFA, the GSEs, and other housing finance stakeholders to advance these goals.

Blog: Viviendas para los hispanos: Cómo el crecimiento de la población hispana ayuda a impulsar el mercado de la propiedad

El número de hogares hispanos ha crecido por seis años consecutivos, incluso durante la pandemia del COVID-19. Aumentar de manera sostenible el acceso a la propiedad de vivienda a través de políticas como los préstamos para un pago inicial bajo, puede ayudar a cerrar la brecha de la propiedad de vivienda.

El 15 de septiembre marca el inicio del Mes de la Herencia Hispana y es una oportunidad para reconocer las significativas contribuciones y la influencia de los hispanos-americanos a la historia, cultura y logros de los Estados Unidos. También es un momento para reflexionar acerca del mercado de propiedades de viviendas para los hispanos en América. En particular, durante los últimos años, la población hispana ha sido un componente clave para el crecimiento de la propiedad de vivienda en los EE.UU., y se proyecta a ser el grupo demográfico que liderará este segmento de la industria por las siguientes cuatro décadas.

De acuerdo con el reporte de 2020 de la Oficina de Censo de EE.UU., durante los siguientes 40 años los hispanos serán los principales contribuidores al crecimiento de la población estadounidense, representando un 68 por ciento hasta el 2060. El Urban Institute también proyecta que de 2020 a 2040, la mayoría de los nuevos propietarios de viviendas netos serán hispanos, estimando que, de 6,9 millones de nuevos hogares, 70 por ciento serán hispanos. Estas cifras hablan de la importancia de este grupo demográfico a nuestra nación y el impacto que tendrán en el mercado de hipotecas y de propiedades de viviendas durante las siguientes décadas.

El crecimiento de la población hispana también es una razón importante para concentrarse en las barreras que existen para que grupos minoritarios puedan acceder a las viviendas. Retos como barreras económicas y la oferta de viviendas asequibles mantienen el acceso a la propiedad fuera del alcance de muchos de estos potenciales propietarios. La brecha de ingresos entre hispanos y blancos no-hispanos sigue siendo pronunciada, con hogares blancos no-hispanos recibiendo un ingreso medio de hasta 26 por ciento por encima de los hogares hispanos. En 2019, el ingreso medio de un hogar hispano fue de $56.113 (Oficina de Censo de EE.UU.). Además, de acuerdo con el reporte “El Estado de la Propiedad de Viviendas para Hispanos 2020”, de la Asociación Nacional de Profesionales Hispanos de Bienes Raíces (NAHREP por sus siglas en inglés), los hispanos tienden a tener una relación de deuda-ingresos (DTI por sus siglas en inglés) más altos y puntajes de crédito más bajos, y dada la juventud de la comunidad hispana, compradores primerizos impulsan las ganancias en la propiedad de viviendas de hispanos. En 2019, el 56 por ciento de propietarios hispanos indicaron que estaban viviendo en el primer hogar que habían tenido, según reportó la encuesta de “Viviendas Americanas de 2019” de la Oficina de Censo de EE.UU. Por lo tanto, los compradores hispanos son un grupo demográfico importante, quienes son atendidos por productos hipotecarios de pago inicial bajo, los cuales benefician a compradores primerizos y de ingresos moderados, principalmente ayudando a cerrar la brecha del pago inicial.

La encuesta del “Mercado de Propiedad de Viviendas Nacional 2021” de USMI, la cual encuestó a 1.000 adultos en los EE.UU., incluyendo una muestra de hispanos, encontró que el 67 por ciento de hispanos considera que ser propietario de un hogar es algo “muy importante”. Además, la encuesta arrojó que 53 por ciento de hispanos reportó haber experimentado problemas de vivienda durante la pandemia del COVID-19, siendo las principales preocupaciones: desalojos y retrasos en el pago de rentas o hipotecas.

Entre los obstáculos que los hispanos enfrentan, 66 por ciento indicó que la escasez de hogares asequibles es el principal problema relacionado a la vivienda. Adicionalmente, el 20 por ciento señaló que uno de los mayores problemas al comprar una casa es la imposibilidad de costear un pago inicial del 20 por ciento, dado que costos mensuales de vivienda consumen una gran parte de los ingresos hispanos; cerca del 60 por ciento indicó que gastan más del 30 por ciento de sus ingresos en vivienda. Finalmente, 65 por ciento de hispanos sugirió que existe un prejuicio socioeconómico en el proceso de compra de viviendas, con la encuesta señalando que niveles bajos de ingreso, falta de riqueza intergeneracional para pagos de iniciales y dificultades en el sistema de puntaje de créditos, están entre las barreras más significativas para incrementar los niveles de propiedad de vivienda entre grupos minoritarios en los EE.UU.

Sin embargo, aunque estas barreras fueron mencionadas, el 90 por ciento de los hispanos también señaló que se sintieron tratados de manera justa durante el proceso de hipoteca. No obstante, mitos y desinformación persisten alrededor de este grupo demográfico. Por una relación de casi 3 a 1 comparado con los encuestados blancos, los hispanos creen que el proceso de aprobación de hipotecas no es asequible e indicaron que no comprenden a plenitud los requisitos para el pago de iniciales. De hecho, el 45 por ciento cree erróneamente que se requiere un pago inicial de 20 por ciento o más cuando en realidad los seguros de hipotecas privados (PMI por sus siglas en inglés) permiten a los compradores adquirir viviendas con pagos de iniciales tan bajos como el 3 por ciento.

Estas cifras y proyecciones dejan claro que, a medida que la población hispana crece rápidamente y tiene un impacto importante sobre el mercado inmobiliario, los responsables de la formulación de políticas no deben perder de vista tanto retos del mercado a corto plazo, como la escasez significativa de viviendas asequibles para compra o renta, como también problemas sistémicos de largo plazo que incrementan innecesariamente los costos o crean barreras para minorías y compradores de menor ingreso. Aun así, a pesar de haber sido particularmente impactados por la pandemia del COVID-19, hispanos-americanos son el único grupo demográfico que ha incrementado su tasa de propiedad de vivienda por seis años consecutivos (incluyendo el 2020) de acuerdo con NAHREP. Retirar las barreras que enfrentan las minorías para acceder a viviendas permitirá que incluso más hogares hispanos gocen de los beneficios de ser propietarios durante las siguientes décadas.

Los seguros de hipotecas privados (PMI) aumentan las posibilidades de compra de viviendas para minorías y hogares de bajos ingresos, al permitirles obtener préstamos de manera asequible y sostenible, ayudándoles así a alcanzar una estabilidad inmobiliaria y generar riqueza, logrando el Sueño Americano. En 2020, casi el 60 por ciento de los prestatarios atendidos por seguros de hipotecas privados eran compradores primerizos y más del 40 por ciento eran prestatarios con ingresos por debajo de los $75.000 anuales. De hecho, la encuesta de USMI encontró que los consumidores ven a este sector privado como una pieza importante dentro del rompecabezas del mercado de propiedad de viviendas, nivelando el campo de juego al ayudar a compradores de bajos y moderados ingresos y primerizos a acceder la financiación de viviendas.

En la medida que celebramos el Mes de la Herencia Hispana, manifestamos nuestro compromiso con el apoyo de políticas sólidas y prudentes que ayuden a expandir la propiedad de viviendas.

Blog: Affordability and Supply Among Top Homebuying Challenges

The lack of affordable housing continues to be a focal point for the mortgage finance community as low- to-moderate income (LMI) and first-time homebuyers continue to report challenges in buying starter homes. In fact, today, the Federal Housing Finance Agency (FHFA) released its Home Price Index and reported that home prices were up 1.7 percent in May, and up an astonishing 18 percent year over year. This significant home price appreciation is largely driven by the lack of housing supply in today’s market and is impacting borrowers’ access to homeownership across the country. Therefore, it is no surprise this topic has become an elevated policy concern, as the “underbuilt” gap has dramatically increased over the last decade, and between 2018 and 2020, the housing stock deficit increased by more than 50 percent according to a recent Freddie Mac report.

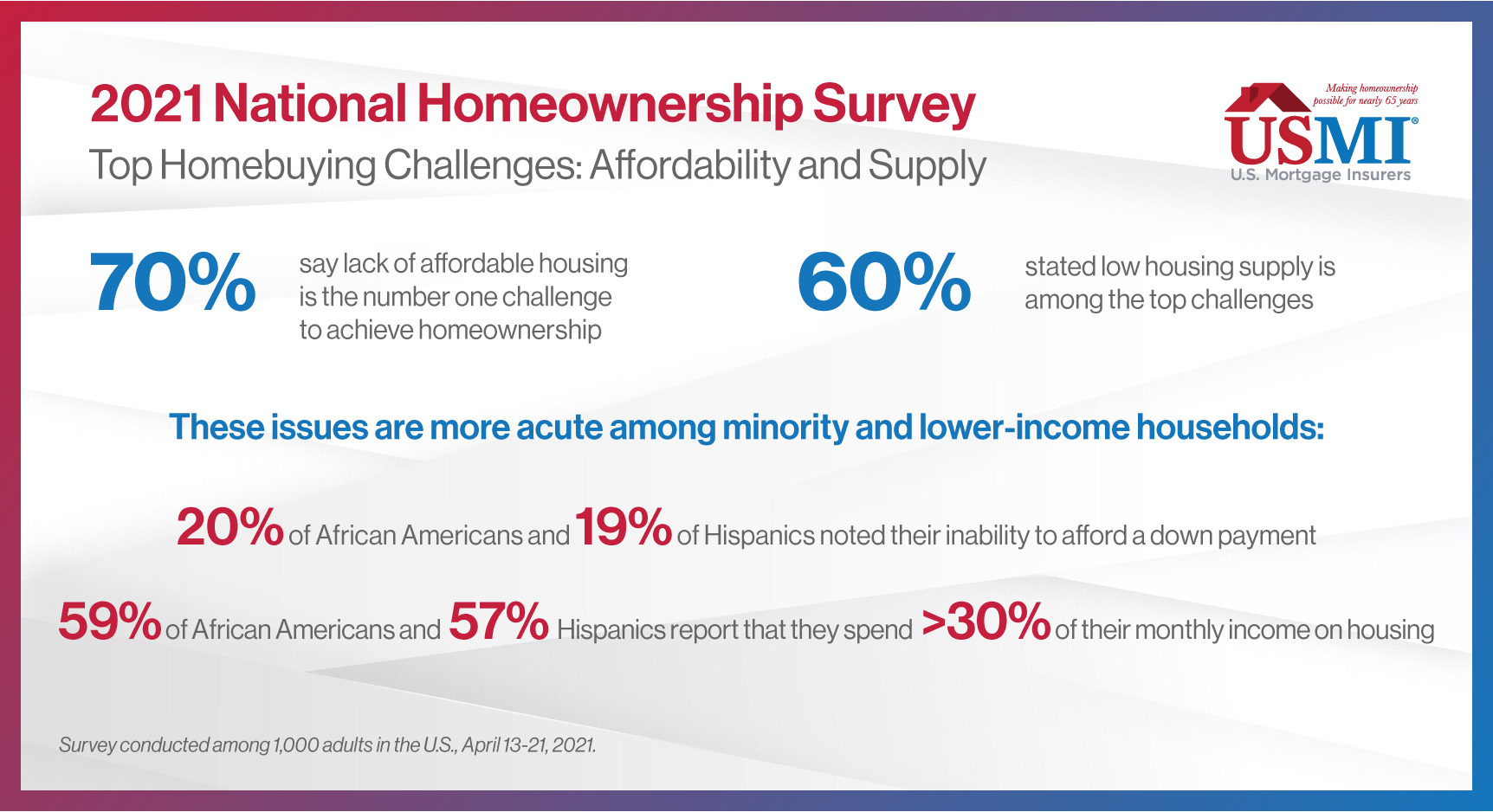

The National Association of REALTORS® (NAR) recently released a report that highlights the dire housing supply situation our nation currently faces. “The state of America’s housing stock […] is dire, with a chronic shortage of affordable and available homes [needed to support] the nation’s population,” and adds that “[a] severe lack of new construction and prolonged underinvestment [have led] to an acute shortage of available housing […] to the detriment of the health of the public and the economy.” In addition to finding an underbuilt gap of 5.5 to 6.8 million housing units since 2001, the report notes that unbuilt single-family homes account for 2 million of those units. This shortage of available and affordable homes, coupled with a robust demand, is fueling the rise of housing prices for potential homebuyers, putting the goal of homeownership further out of reach. NAR’s Chief Economist Lawrence Yun stated in the report, “[t]here is a strong desire for homeownership across this country, but the lack of supply is preventing too many Americans from achieving that dream.” In late June, USMI released its 2021 National Homeownership Market Survey, fielded by ClearPath Strategies among 1,000 U.S. adults in the general population, which found that Americans understand the importance of owning a home: more than 7 in 10 respondents see this as important for stability and financial security.

USMI, in representing a sector of the industry that is dedicated to facilitating affordable low down payment lending and promoting sustainable homeownership, explored this topic in our recent survey, which found that lack of affordable housing and low supply of housing ranked among the top homebuying challenges. In fact, nearly 7 in 10 respondents ranked the lack of affordable housing as the number one housing challenge and nearly 6 in 10 stated that low housing supply is another top issue. These issues were more acute among minority and lower income homebuyers as 20 percent of African American and 19 percent of Hispanic respondents note their inability to afford a down payment. Further, more than half of African Americans (59 percent) and Hispanics (57 percent) reported spending over 30 percent of their monthly income on housing, the threshold for a household to be considered “housing-cost burdened.” The complete findings from USMI’s national survey are available here.

These challenges are front and center of the nation’s housing agencies, FHFA and the Federal Housing Administration (FHA). Last month, President Biden appointed Sandra L. Thompson as FHFA’s Acting Director, having previously served as the Deputy Director of the Division of Housing Mission and Goals since 2013. In her accepting remarks, Thompson stated that “[t]here is a widespread lack of affordable housing and access to credit, especially in communities of color,” adding that “[i]t is FHFA’s duty through our regulated entities to ensure that all Americans have equal access to safe, decent, and affordable housing.” President Biden also recently nominated Julia Gordon to be the Assistant Secretary for Housing and FHA Commissioner.

USMI continues to urge policymakers and the housing finance industry to focus on addressing this historic shortage of affordable homes to help balance housing prices and ensure access to homeownership. In a letter directed to the Department of Housing and Urban Development (HUD) Secretary Marcia Fudge, USMI urged HUD to avoid policies that would stoke more demand in the marketplace without addressing the supply issues, as not doing so will only worsen the affordability challenges. And while addressing supply and the shortage of affordable homes is imperative, policymakers must also not lose sight of addressing the issues that unnecessarily increase costs or create barriers for minority and lower income homebuyers. Importantly, expanding homeownership opportunities for these borrowers does not have to be at the expense of reforms made over the last decade that have strengthened the system to reduce risk, protect borrowers, and avoid another housing market collapse.

We appreciate that policymakers recognize the role of low down payment mortgage options in facilitating homeownership. USMI’s survey found that consumers view mortgage insurance (MI) as an important piece of the homeownership puzzle, specifically because MI levels the playing field by helping LMI and first-time buyers access home financing. In fact, 73 percent of all respondents view MI as needed and positive to obtaining homeownership, and nearly 70 percent of respondents citing that it is important to have access to these low down payment loans through both the conventional market backed by private MI and government-backed loans through FHA.