WASHINGTON — U.S. Mortgage Insurers (USMI), the association representing the nation’s leading private mortgage insurance (MI) companies, released annual volume data showing that the private MI industry helped more than 800,000 borrowers secure mortgage financing in 2025. Approximately 92% of these mortgages were new purchases.

“Homeownership has long been a bedrock of the American Dream and, for generations, private MI has served as a tool for millions of American families to affordably and sustainably achieve this milestone,” said Seth Appleton, President of USMI. “This latest data further demonstrates the foundational role private MI plays in making homeownership attainable for first-time homebuyers and working families across the country.”

Over the past nearly 70 years, the private MI industry has enabled nearly 41 million people to access affordable and sustainable low down payment mortgages. In 2025, nearly 65% of those who used private MI to purchase a home without a large cash down payment were first-time homebuyers. The average loan amount for mortgages backed by private MI was roughly $375,000, according to data from Fannie Mae and Freddie Mac (the GSEs).

A USMI report found that, on average, it could take 26 years for a household earning the national median income to save a 20% down payment plus closing costs at the median national sales price. Rather than waiting a quarter century to achieve homeownership, private MI allows homebuyers to get off the sidelines with as little as a 3% down payment and begin building generational wealth and equity years, or even decades, sooner. By using private MI and accessing homeownership with smaller down payments, American homebuyers collectively saved more than $250 billion in down payment costs since 2020, including more than $35.3 billion in 2025 alone.

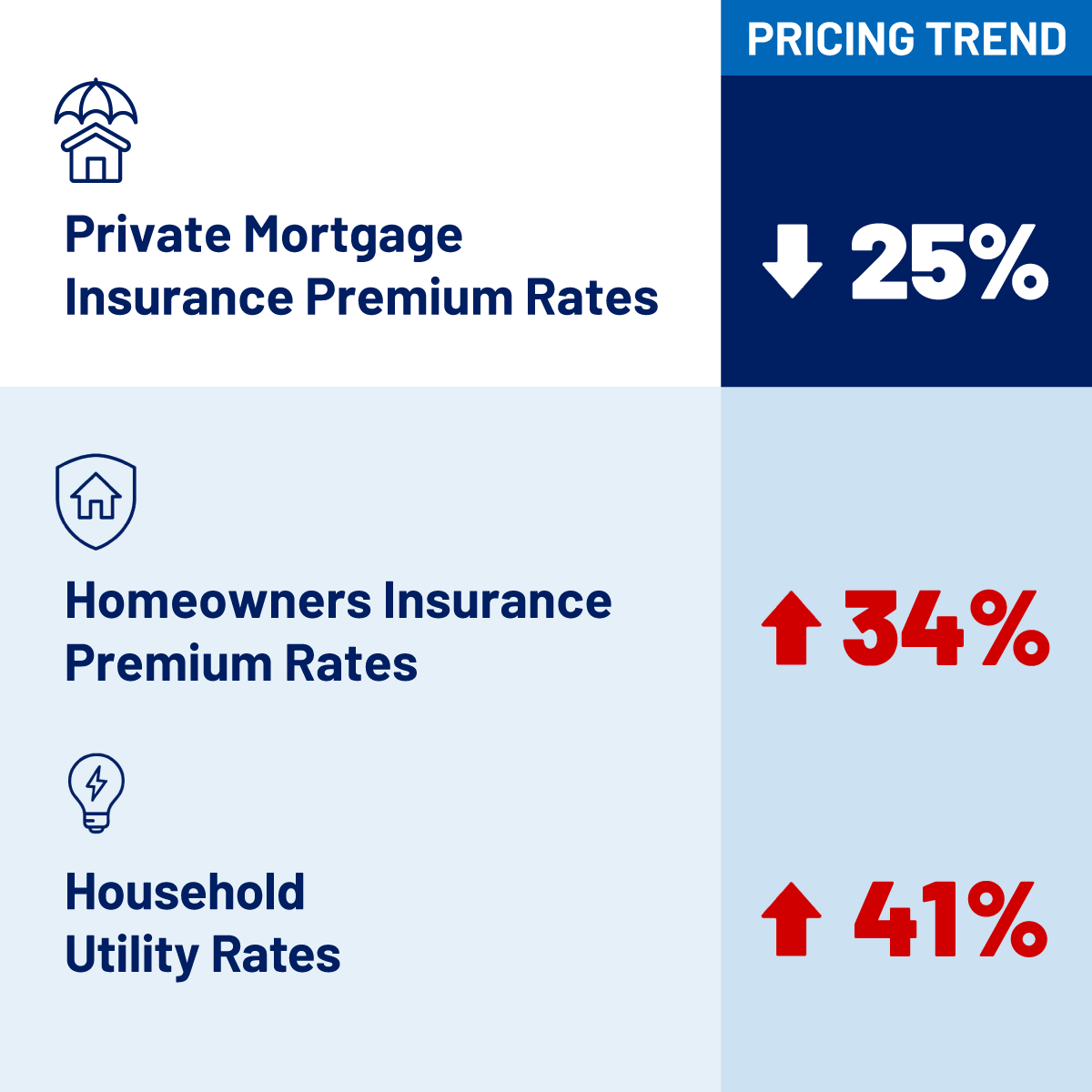

Importantly, private MI premium rates, as measured by publicly available in-force portfolio yield data, have declined in recent years due to the 2017 Trump tax cuts and enhanced risk-based pricing, in stark contrast to other costs associated with homeownership such as homeowners insurance premium rates and household utility rates. And, thanks to the Working Families Tax Cuts signed into law by President Trump last summer, qualified homeowners will once again be able to deduct premiums paid to private MI companies and government agencies on their federal income taxes and receive targeted tax relief.

“The deduction was claimed more than 44 million times between 2007 and 2021, when qualified American families were able to deduct MI premiums from their federal taxes. For 2021, the average deduction was more than $2,300,” said Appleton. “Beginning next tax season, millions of hard-working American homeowners will once again receive meaningful relief as federal tax policy promotes sustainable homeownership across the country.”

By design, private MI serves as the first layer of private capital protecting the housing finance system against default risk, protecting more than $1.6 trillion in mortgages and shielding the GSEs, lenders, and taxpayers from mortgage credit risk. The private MI industry’s strength and resiliency has been reinforced by safeguards and enhancements, including updated Private Mortgage Insurer Eligibility Requirements (PMIERs), which set robust, granular requirements for insuring loans acquired by the GSEs.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to affordable and sustainable housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.