Press Release: Comments on FHFA’s Single-Family Credit Risk Transfer Request for Input

For Immediate Release

October 11, 2016

Media Contact: Dan Knight

(202) 777-3547

USMI Submits Comments on FHFA’s Single-Family Credit Risk Transfer Request for Input

Mortgage insurers outline industry’s role in shifting greater risk away from taxpayers in an equitable way for all lenders while expanding access to homeownership

WASHINGTON — U.S. Mortgage Insurers (USMI) submitted comments to the Federal Housing Finance Agency (FHFA) today regarding its Single-Family Credit Risk Transfer (CRT) Request for Input (RFI) and steps to further shield the government sponsored enterprises (GSEs), Fannie Mae and Freddie Mac, as well as American taxpayers, from losses from mortgage-related risks. In its comments, USMI highlights the distinct advantages of front-end CRT done through expanded use of mortgage insurance (MI) that can address existing shortcomings in the GSEs’ credit risk transfer transactions and that can offer substantial benefits for taxpayers, lenders of all sizes, and borrowers.

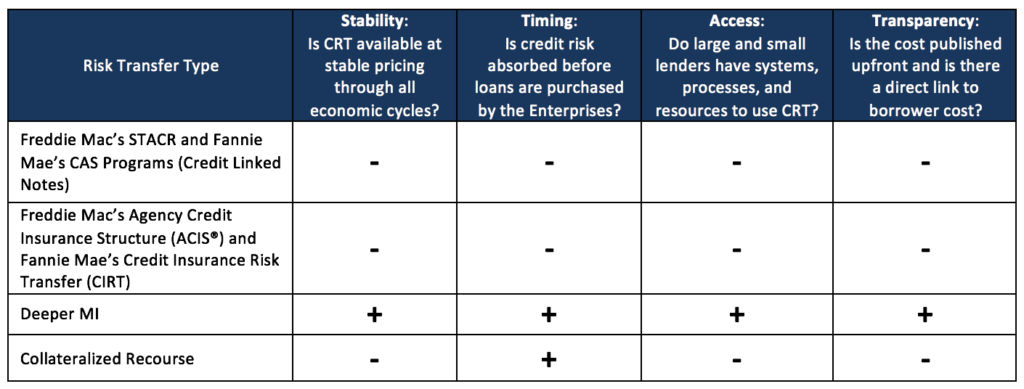

USMI notes in its comments that “increasing the proportion of front-end CRT in the Enterprises’ CRT strategy will advance four key objectives of a well-functioning housing finance system by ensuring that: (1) a substantial of private capital loss protection is available in bad times as well as good; (2) such private capital absorbs and deepens protection against first losses before the government and taxpayer; (3) all sizes and types of financial institutions have equitable access to CRT; and (4) CRT costs are transparent, thereby enhancing borrower access to affordable mortgage credit.”

“By design, and as evidenced by the more than $50 billion in claims our industry paid during and since the financial crisis, mortgage insurance provides significant first-loss risk protection for the government and taxpayers against losses on low-down payment loans,” said Lindsey Johnson, President and Executive Director of USMI. “As the government explores ways to further reduce mortgage-related risk while also ensuring that Americans continue to have access to affordable home financing, experience shows that mortgage insurance is the answer, particularly when you consider mortgage insurance protection is at work before the risk even reaches the GSEs’ balance sheets.”

While USMI commends FHFA in its comment letter for establishing principles and risks to evaluate front-end CRT structures, which will enable the GSEs and other market participants to analyze the virtues and shortcomings of each form of CRT using an analytical framework, it urges that “the RFI principles should apply to both existing and proposed CRT activities.”

Among other questions, the RFI inquired about benefits of front-end CRT for small lenders. USMI explains in its letter that “small lenders derive optimal benefits from CRT programs that are familiar, have minimal implementation costs, and are based on lender selection among several market participants. Accordingly, MI works very well for small lenders (and deeper-cover MI similarly would work very well for small lenders) because it is already part of their current credit origination processes, is available with transparent pricing, and is available to lenders of all sizes. On the other hand, small lenders have no access to and derive no direct benefits from back-end forms of CRT.”

“In addition to the specific goal of shifting more risk from Fannie Mae and Freddie Mac, and unlike back-end CRT, mortgage insurance plays a direct role in helping families who have good credit but can’t afford large down payments to qualify for a mortgage. For nearly sixty years, mortgage insurers have been leaders in helping millions of Americans, particularly first-time homebuyers, purchase homes in an affordable way,” Johnson said.

Johnson added, “MI is one of the best forms of time-tested credit risk protection for our nation’s mortgage finance system. Mortgage insurers have taken steps to enhance both their claims paying ability—by increased capital and operational standards—and their claims paying process through updated Master Policy Agreements. MI is private capital directly tied to housing. Unlike some other forms of CRT structures, MI is dedicated to a housing finance system in good and bad economic times. By using more MI to provide deeper front-end risk sharing on loans the GSEs guaranty, the GSEs and taxpayers will be at a much more remote risk of losses. Promoting greater front-end risk sharing with MI is a way to help build a strong, stable housing finance system, provide prudent access to affordable mortgage credit, protect taxpayers, and help facilitate the homeownership aspirations for Americans for years to come. ”

USMI’s full comments to FHFA can be found here. A fact sheet on USMI’s comments can be found here.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.